China’s bear market woes run deeper than Trump tariffs

Trade war a sideshow to bigger concerns about tight credit and poor data

Don Weinland in Mumbai and Roger Blitz in London

Blame for the sell-off of China’s stock market has been levelled at the Sino-US trade war but Beijing’s problems have been evident for some time and run much deeper.

Long before US president Donald Trump imposed billions of dollars in tariffs against China, a steady drip of credit tightening and middling Chinese economic data underpinned the selling, with the tariff rhetoric just amplifying the gloom.

China’s key stock market index, the Shanghai Composite, has now tumbled into bear market territory for the first time in more than two years, falling another 1.1 per cent on Wednesday.

The last major sell-off at the start of 2016 was driven by a clutch of bad economic indicators. This time analysts say a multitude of concerns for China — from a mounting trade war with the US and failing overseas projects, to tighter credit and a pullback from institutional investors — has spurred the abrupt cooling of investor sentiment for shares.

“The A-share [domestic Chinese stocks] market began underperforming before the announcement of tariffs,” said Ting Gao, head of UBS China equity strategy. “The materials, industrial and property sectors are down a lot — they [investors] are pricing in a fairly deep growth problem.”

Concerns about tightening monetary policy over the past year and more restrictive banking regulation have fuelled fears about tight credit and lower growth — worries seemingly confirmed by a wave of bond defaults seen in China this year.

“What’s different today is that you are seeing a different regulatory environment,” said Nicholas Chui, senior investment manager at Aberdeen Standard Investments. “Things are tighter than ever and the days of easy monetary policy are over.”

Banks have been forced to recognise many off-balance-sheet assets. This has led to a tightening of liquidity in shadow lending channelled through asset management companies.

In China’s bluntest response to the fall in stocks so far, the People’s Bank of China announced on Sunday it would cut the reserve requirement ratio (RRR) for a number of banks, deploying about $100bn into the economy. The measure was directed at cushioning the impact of the US tariffs and allaying investors concerned about credit tightening.

“The policy is to support a stable market. The RRR cut showed this, and from a monetary policy perspective, there are a lot of tools for the PBoC to employ,” said Frank Tsui, a fund manager at the Hong Kong-based Value Partners.

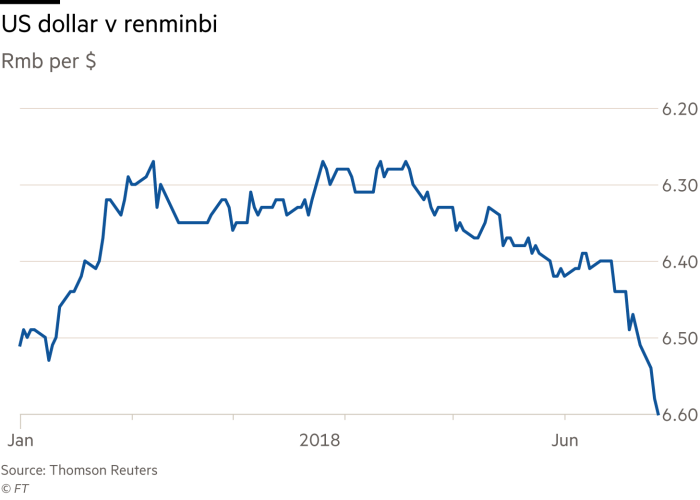

But the RRR cut has been complicated by a drop in China’s renminbi. Its fall this week of 1.5 per cent against the dollar, which takes it to its lowest level in six months, has investors wondering whether the PBoC may be using the exchange rate as a trade war tool.

“Aside from retaliating with like-for-like tariffs, Chinese policymakers could well be intentionally weakening their currency as another form of retaliation — a weaker CNY would help Chinese exports and hurt US imports,” said Bilal Hafeez, forex strategist at Nomura.

But he and other analysts know there would be a hefty price to pay — in turning investors away from Chinese markets, and encouraging capital flight.

That would inflict more harm on the Chinese economy than the US economy, said Geoff Yu of UBS Wealth Management — not to mention China’s trading partners. “So devaluing the CNY would likely invite criticism from other countries,” he said.

In any case, Mr Yu added, the US could easily raise import tariffs further to offset the effects of a weaker renminbi.

Renewed investor anxiety over China comes at a time when its companies were hoping to capitalise on growing market attention. Global index funds began pouring money into Chinese stocks many months before China’s inclusion in the MSCI Emerging Markets index.

Index provider MSCI added a list of 234 China-listed stocks to its flagship EM index in late May, a moment viewed as a key development for China’s opening up to global investors.

But the MSCI hype has largely petered out, analysts said.

“There was lots of anticipation that big index funds would be buying into the market in the run-up to inclusion,” said Arthur Kwong, head Asia-pacific equities at BNP Paribas Asset Management. “Now you don’t have these big buyers.”

Mr Kwong said no single factor had pushed the Shanghai Composite into bear-market territory. Instead, diverse factors led to the poor performance. Even problems with the country’s overseas infrastructure boom, called the Belt and Road Initiative, has generated increasingly negative sentiment on domestic stocks, he said.

Traders now have to decide whether the China’s domestic share market is oversold. A widening discount of A-shares to equivalent stocks traded in Hong Kong suggests that China’s predominantly retail market has over sold.

“There is not a lot of long-term money [in China] — it’s short-term reactive,” said Stuart Rae, chief investment officer Asia-Pacific value equities, AllianceBernstein. “You should not react to the short-term news. Earnings growth has not changed much yet valuations have got cheaper.”

Additional reporting by Jasper Moiseiwitsch in Hong Kong

0 comments:

Publicar un comentario