Bond markets signal early end to Fed rate rises

While the central bank hails strength of US economy, traders are not so sure

Joe Rennison in New York

Fed chair Jay Powell

Bond traders are anticipating that an end to the Federal Reserve’s cycle of monetary policy tightening could come as early as next year, facing down policymakers that expect to raise interest rates for longer.

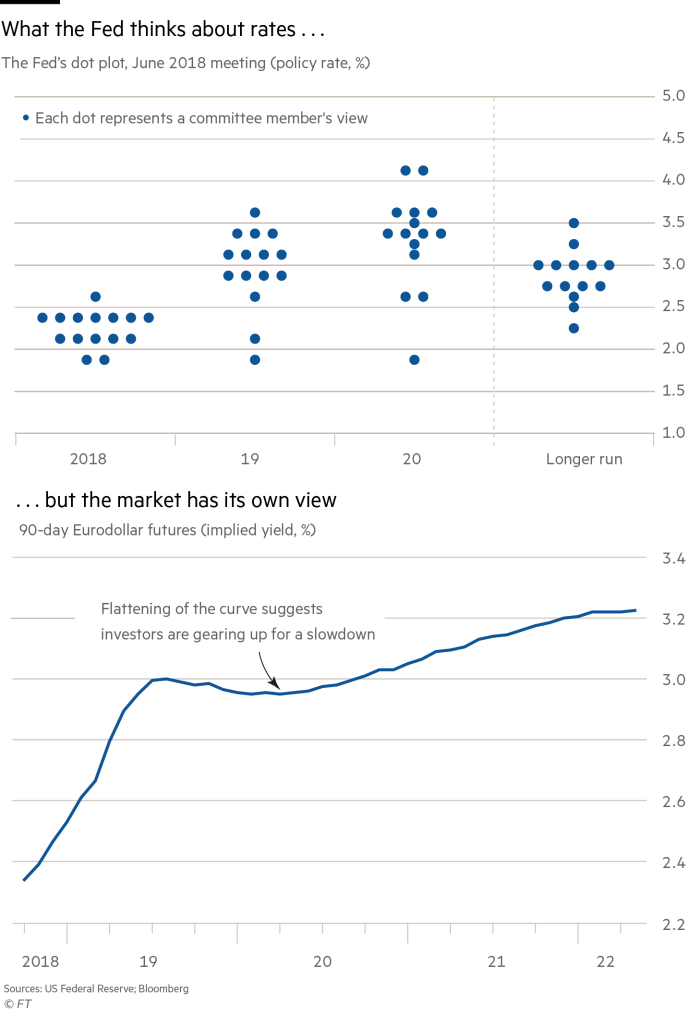

While the Fed expects to raise rates into next year and potentially the year after — a point that could be reiterated by chair Jay Powell when he gives testimony this week to Congress — current prices in US interest rate markets suggest that the central bank will stop its hiking cycle sooner.

According to the median prediction by policymakers, the Fed policy rate will rise to 3.375 per cent in 2020. In contrast, eurodollar futures suggest rates may plateau in 2019.

The differences come as investors are factoring in the risk of a slowdown in the economy despite strong corporate earnings growth and positive economic data, .

“The markets are telling us that there is a pretty high risk of economic slowdown or recession at the end of 2019,” said Guy LeBas, chief fixed-income strategist at Janney Capital Management.

The yield on futures expiring in December 2019 stood at 2.97 per cent on Friday, and on futures expiring in March 2020 it was an almost identical 2.975 per cent. The yield falls to 2.96 per cent for December 2020 eurodollar futures.

“The market is saying that the Fed is wrong,” said John Brady, managing director at RJ O’Brien.

This is only the fifth time since 1989 that there has been an inversion in the eurodollar futures yield curve, where longer-term rates are below shorter-dated rates. Each time it has been followed by the Fed pausing its policy tightening.

The Fed has been stressing the strength of the economy in its recent communications but trade concerns have amplified fears that companies may begin to slow capital expenditure, while some analysts say that the boost from tax reform will begin to erode in 2019 as year-over-year growth comparisons will be set at a higher bar.

A second market measure of interest rate expectations, fed funds futures, which are less heavily traded than eurodollar futures, is showing a similar plateau in 2019, although it is not inverted.

The pattern can also be seen in the difference between two and 10-year Treasury yields, with the 10-year struggling to sustain levels above 3 per cent. When shorter-dated yields rise above longer-dated yields it is seen by many investors as a sign of a coming recession. The spread on Friday between the two Treasury benchmarks stood at just 24 basis points, the lowest level since 2007.

A majority of Fed policymakers expect two more rate rises this year. With further moves early next year, that would put the Fed close to its median estimate of the neutral interest rate, at which monetary policy neither stimulates nor cools the economy. Policymakers are intensely debating whether to push beyond that level or call a halt there.

Complicating deliberations is the Fed’s balance sheet, which some officials think may be artificially flattening the yield curve and making it a less useful indicator than in previous economic cycles.

The size of the balance sheet is still holding down long-term rates, they suggest, but the programme to reduce its holdings, which began in October of last year, may be contributing to an upward drift in short-term rates as investors struggle to digest the increase in supply.

Additional reporting by Sam Fleming

0 comments:

Publicar un comentario