Stronger dollar poses challenge for Wall Street blue-chips

Currency strength seen hurting foreign revenues for multinational companies

Nicole Bullock in New York and Chloe Cornish in London

As the political crisis in Italy has deepened, the euro fell below $1.15

Market turmoil in Europe led by Italy’s escalating political crisis is set to extend the US dollar’s rise, raising questions on Wall Street of a hit to foreign profits for blue-chip multinational companies.

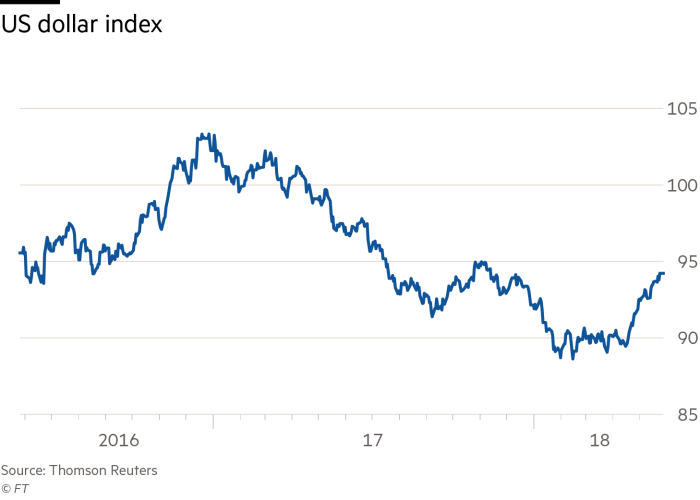

The dollar has gained more than 7 per cent against the euro since the single currency peaked at $1.25 in early February. As the political crisis in Italy has deepened this week, the euro fell below $1.15 — its lowest level since July 2017.

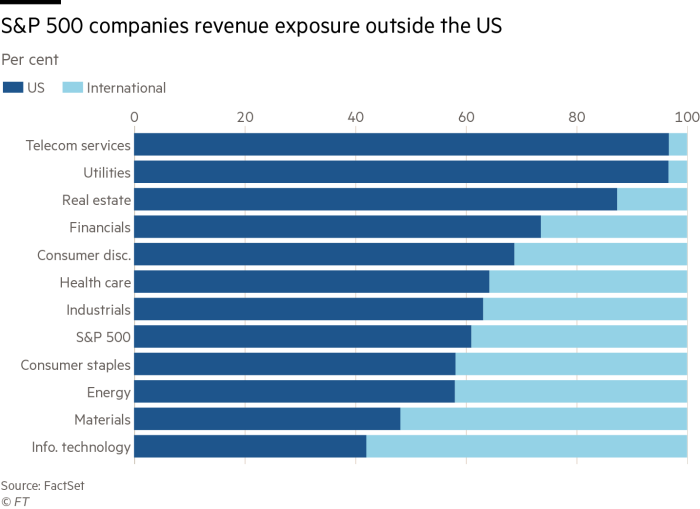

Many of the leading lights in the S&P 500 rely on foreign-based revenues and thus face an unfavourable conversion when the dollar strengthens. It is not a perfect science — companies do not uniformly disclose their reliance on foreign revenues, and they can and do hedge their currency exposure — but few are likely to escape unscathed if the rising dollar trend continues.

Still, since mid-April, the dollar has steadily climbed against a basket of other major currencies, which include the euro, buoyed by signs of a stronger economy that has added more than 5 per cent to its value.

“A rising US dollar translates into a negative currency headwind for many of the companies in the S&P 500,” said Martin Jarzebowski, vice-president and portfolio manager at Federated Investors.

The dollar’s recent turn also coincides with the first-quarter reporting season by US companies. A surge in US corporate profit growth in the wake of tax cuts, estimated at about 25 per cent year on year by Factset, has failed to drive the S&P 500 back to its record peak set in late January.

This reflects a sense among some investors that earnings may have peaked for the cycle, with such apprehension reinforced should the dollar gain further altitude.

David Donabedian, chief investment officer of CIBC Atlantic Trust, said: “I do not look at this 4-5 per cent rise in the dollar as a big game changer in earnings.” Still, he added that the rebound in the currency “is supportive of the idea that after the third quarter you get a deceleration of earnings”.

Some industries and sectors are more sensitive to shifts in the dollar than others. Tech companies as a group, for example, derive more than half of their revenue outside the US. Consumer staples groups also have significant overseas exposure, while telecoms companies, utilities and the real estate sector are largely domestic.

“Regional banks, homebuilders — there is a whole group of industries that really do not have a lot of exposure outside the 50 states,” said Mr Donabedian. “But this is not a big enough move [in the dollar] to be playing that — not as of yet.”

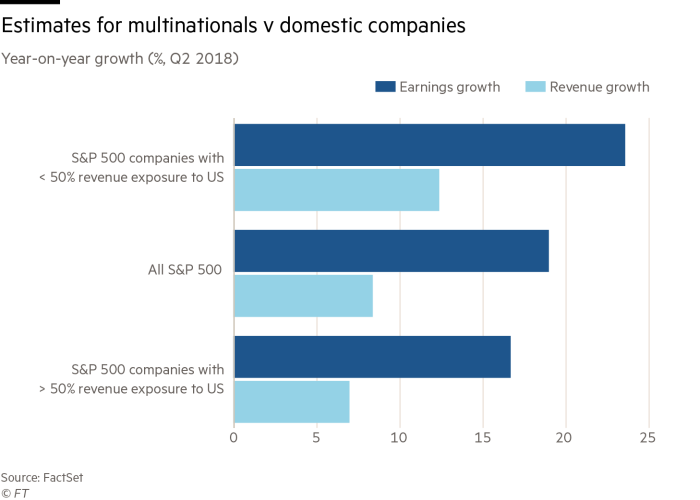

FactSet data also show that Wall Street analysts forecast companies that make more than half of their revenue outside the US reporting greater revenue and earnings increases for the second quarter compared with those that are more domestically focused and the overall S&P 500.

Market moves also reflect that exposure to economies outside the US remains in favour.

The S&P 500 US Revenue Exposure index, which measures the performance of companies in the index with higher than average revenue exposure to the US, is down for the year, whereas an index that measures companies with a higher than average revenue exposure outside the US is up nearly 3 per cent. Over time, however, the latter’s performance has been driven more by bullish or bearish sentiment about China than the moves of the dollar.

The dollar’s recent ascent helps to explain why the shares of small companies, which tend to generate most of their revenue at home, have outperformed the S&P 500. The domestic focus also insulates small-caps to the trade tensions that have emerged this year and makes them a bigger beneficiary of cuts in the corporate tax rate and a stronger economy.

According to David Lefkowitz, senior equity strategist at UBS Global Wealth Management, the back of the envelope calculation indicates that a 10 per cent change in the dollar spurs a 2 per cent shift in S&P 500 earnings.

Mr Lefkowitz said the dollar “would have to rise another 10 per cent before that tailwind [to S&P 500 earnings] would go away. The move is pretty small in the scheme of things”.

Meanwhile, the strengthening dollar and weakening pound provides a boost to international stocks in London, where the FTSE 100 index hit an all-time high earlier this month.

“North America accounts for roughly 20 per cent of [FTSE all share] revenues,” said James Illsley, a UK equity portfolio manager at JPMorgan Asset Management, adding that approximately 40 per cent of UK-listed dividends are declared in dollars: “Think about big oil stocks, HSBC . . . You can receive [these dividends] in sterling as a UK investor, so dollar strength will obviously help”.

Mike Fox, head of sustainable investments at Royal London, said growth differentials — currently in favour of the US over the UK and Europe — tend to be a short-term driver of key foreign exchange rates . . . “It’s very useful for GlaxoSmithKline, AstraZeneca, BP”.

0 comments:

Publicar un comentario