Fed’s dilemma grows more acute after EM and Europe turmoil

Bank of India governor pleads for US central bank to relax tightening plans

Joe Rennison and Robin Wigglesworth

© AP

The US Federal Reserve is often buffeted by fierce cross-currents but investors caution that balancing the strong domestic economy and rising turbulence in emerging markets — and now Europe — will require a particularly adept hand at the tiller this year.

Although Argentina and Turkey have been the focus for their own idiosyncratic reasons, Urjit Patel, India’s central bank governor, argued that emerging markets are suffering a broader bout of “upheaval” caused by the “double whammy” of the Fed’s balance sheet shrinkage and the US Treasury’s borrowing binge.

“Given the rapid rise in the size of the US deficit, the Fed must respond by slowing plans to shrink its balance sheet,” Mr Patel wrote in the FT on Monday. “If it does not, Treasuries will absorb such a large share of dollar liquidity that a crisis in the rest of the dollar bond markets is inevitable.”

At the same time, Italy’s political crisis may have abated with the formation of a new government but the anti-establishment, populist and Eurosceptic parties that will now control Italy are hardly beloved of investors. Longer term concerns over the durability of the common currency remain, something that sent US Treasury yields tumbling early last week.

On the other hand, analysts note that the US economy continues to expand at a robust clip, exemplified by unemployment numbers and manufacturing data released on Friday. That double dose of strong data prompted traders to lift Treasury yields back up higher again to end the week — and it improved the odds of the Fed staying on its path of monetary tightening this year.

“I think it steadies the Fed’s hand. I do think that three increases this year are there, and the chance of four is back on the table,” said Jim Paulsen, chief investment strategist at the Leuthold Group. “The market message is that the Fed should continue to tighten. I would think the Fed sees that message, too.”

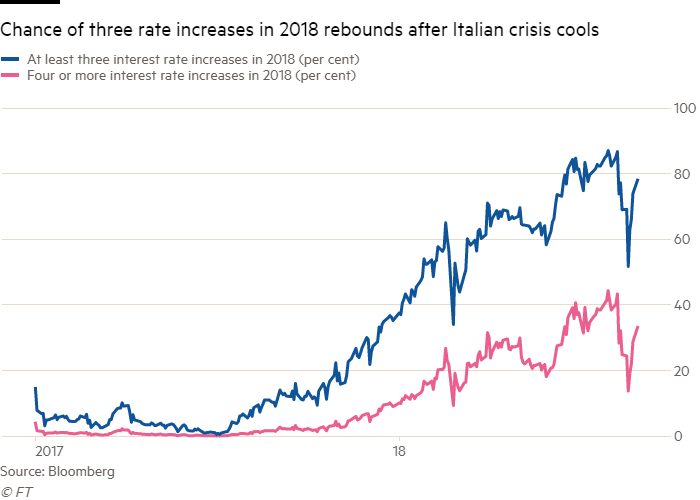

The tug of the cross-currents is well-illustrated by the oscillations in the Fed funds market. The odds on three more interest rate increases this year, on top of the first rise announced in March — as implied by Fed funds futures — had risen to a high of nearly 40 per cent by May 22, plummeted to a low of 13 per cent on May 29 and rose back to 30 per cent on Monday.

The implied probability of the Fed only raising interest rates once more this year, after the March increase, jumped from 13 per cent on May 22 to nearly 40 per cent at the peak of the Italian turmoil but has since slid back to under 20 per cent.The Treasury market has also see-sawed with the 10-year Treasury yield bouncing back from a low of 2.76 per cent on May 29 to 2.92 per cent on Monday.

The Fed itself has indicated that it plans to raise interest rates twice more this year. And many investors and analysts reckon that the US central bank will not be pushed off course by stresses in Europe and the developing world — something that Lael Brainard, one of the Federal Reserve’s governors, hinted in a speech last week.

“An environment with a strengthening dollar, rising energy prices and the possibility of rising rates raises the risks of capital flow reversals in some emerging markets that have seen increased borrowing from abroad. Although stresses have been contained to a few vulnerable countries so far, the risk of a broader pullback bears watching,” she noted.

However, “continued gradual increases” in interest rates remained “appropriate”, Ms Brainard said, given the economic stimulus that the $1.5tn of tax cuts and a $300bn increase in federal spending would entail.

Indeed, given the robust US economic outlook, some analysts even caution that it runs the risk of overheating. The 10-year “breakeven” rate, a market measure of investors’ inflation expectations, remains above the Fed’s target 2 per cent at 2.07 per cent, despite recent declines, and inflation is expected to continue to accelerate into the summer.

“The Federal Reserve has to focus on stable growth in their own economy,” said David Kelly at JPMorgan Asset Management. “They cannot be overly worried about what is going on in other markets.”

Even investors that remain sceptical of inflation accelerating forcefully doubt that US policymakers will be pushed off course. “The Fed monitors these situations but the US has a pretty good growth story,” said Dan Ivascyn, global chief investment officer at Pimco.

Nonetheless, political stress was easier for markets to ignore when central banks were accommodative, and cracks could emerge or widen as the Fed continues to ratchet back its monetary stimulus, according to Aaron Kohli, a strategist at BMO Capital Markets. “The Fed is exerting stress — not just in the US but globally — as it tightens conditions,” he said.

This is what worries Mr Patel of the Reserve Bank of India. He argued that the current pace of Fed balance sheet shrinkage could be slowed to avoid the otherwise “inevitable” fallout from boomeranging back on the US economy.

“Such a move would help smooth the impact on emerging markets and limit effects on global growth through the supply chains that span both developed and emerging economies.

Otherwise, the possibility will increase of a ‘sudden stop’ for the global economic recovery,” he wrote. “That might hurt the US economy as well. Circumstances have changed. So should Fed policy.”

0 comments:

Publicar un comentario