Emerging markets face a dollar double whammy

The Fed must adjust its balance sheet shrinkage to limit the effects of less liquidity

Urjit Patel

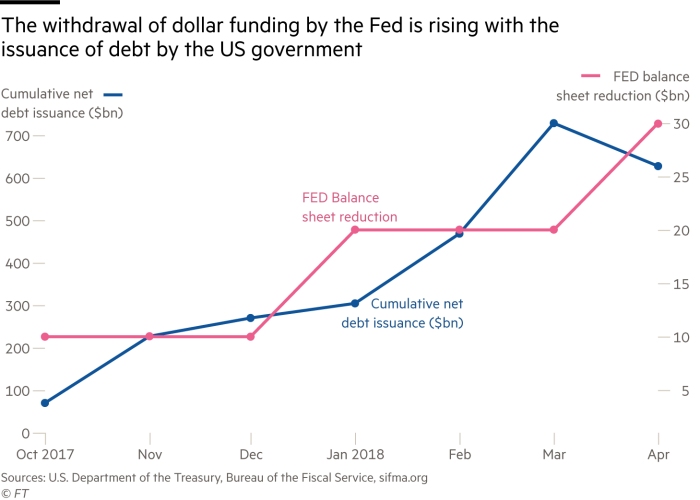

Over the next few years, the government’s net issuance of debt will stabilise, whereas the Fed’s balance-sheet reduction will keep rising © AP

Dollar funding of emerging market economies has been in turmoil for months now. Unlike previous turbulence, this episode cannot be attributed to the US Federal Reserve’s moves on interest rates, which have been rising steadily since December 2016 in a calibrated manner.

The upheaval stems from the coincidence of two significant events: the Fed’s long-awaited moves to trim its balance sheet and a substantial increase in issuing US Treasuries to pay for tax cuts. Given the rapid rise in the size of the US deficit, the Fed must respond by slowing plans to shrink its balance sheet. If it does not, Treasuries will absorb such a large share of dollar liquidity that a crisis in the rest of the dollar bond markets is inevitable.

Consider the scale of both events. Starting in October 2017, the Fed began reducing reinvestment of the coupons it receives from debt securities holdings. That shrinkage will peak at $50bn a month by October and total $1tn by December 2019. Meanwhile, the US fiscal deficit is projected to be $804bn in 2018 and $981bn in 2019, implying net issuance by the US government of $1.169tn and $1.171tn, respectively, in the two years.

So, the withdrawal of dollar funding by the Fed, as it reduces its reinvestment of income received, is proceeding at roughly the same pace as that of net issuance of debt by the US government. Over the next few years, the government’s net issuance will stabilise, albeit at a high level, whereas the Fed’s balance-sheet reduction will keep rising.

This unintended coincidence has proved to be a “double whammy” for global markets. Dollar funding has evaporated, notably from sovereign debt markets. Emerging markets have witnessed a sharp reversal of foreign capital flows over the past six weeks, often exceeding $5bn a week. As a result, emerging market bonds and currencies have fallen in value.

When the Fed announced the normalisation of its balance sheet, the full extent and details of the Trump tax cuts were not known. Both scale and timing of the US fiscal deficit have been a surprise to markets.

The US central bank has shown admirable sagacity in its rate increases since they were first telegraphed in statements of the Federal Open Market Committee in 2012. Indeed, its flexible approach has played a pivotal role in maintaining global financial stability.

The Fed was reasonably consistent in its forward guidance on the first rate rise. Nevertheless, it extended the period for exceptionally low levels from “at least through late 2014” in 2012 to “well past the time that the unemployment rate declines below 6.5 per cent” in December 2013.

Forward guidance was updated from March to October 2014, and in March 2015, to reflect the sensitivity in timing the first rise in the Fed funds rate to match inflation outcomes. In sum, the Fed carefully adjusted the pace to evolving macroeconomic conditions. Global spillovers did not manifest themselves until October of last year. But they have been playing out vividly since the Fed started shrinking its balance sheet. This is because the Fed has not adjusted to, or even explicitly recognised, the previously unexpected rise in US government debt issuance. It must now do so.

The good news is that there is an option available to the Fed that does not require it to change the overall policy direction. It can simply recalibrate its normalisation plan, adjusting for the impact of the deficit. A rough rule of thumb would be to reduce the pace of its balance-sheet contraction by enough to damp significantly, if not fully offset, the shortage of dollar liquidity caused by higher US government borrowing.

Such a move would help smooth the impact on emerging markets and limit effects on global growth through the supply chains that span both developed and emerging economies.

Otherwise, the possibility will increase of a “sudden stop” for the global economic recovery.

That might hurt the US economy as well. Circumstances have changed. So should Fed policy. It would still reach the same destination, but with less turmoil along the way.

The writer is the governor of the Reserve Bank of India

0 comments:

Publicar un comentario