Brazilian Markets Plummet As Elections Approach

by: Ian Bezek

- Brazilian markets dropped as much as 9% Thursday, capping a 33% decline since January.

- The trucking strike is over, but the consequences have just begun.

I- t's too early to buy Brazil on the whole, but there may be a couple of stocks worth taking a look at as prices tumble.

- The trucking strike is over, but the consequences have just begun.

I- t's too early to buy Brazil on the whole, but there may be a couple of stocks worth taking a look at as prices tumble.

- This idea was discussed in more depth with members of my private investing community, Ian's Insider Corner.

2018 is shaping up to be an exciting year for emerging markets. Lately, we're getting a fresh panic every couple of weeks, with Brazil taking the mantle now that Argentina and Turkey have calmed down for the moment. Brazilian stocks, which were sprinting to multi-year highs as recently as January, have skidded since then. In fact, the country, as measured by the iShares MSCI Brazil Capped ETF (EWZ) is down by almost a third in just a few months - highlighted with an impressive 5% dump (as of this writing) on Thursday:

Long-time readers probably remember that I'm fundamentally bearish on Brazil as an economy on a longer time horizon. The country has massive entrenched problems, including but not limited to an unaffordable pension scheme, unbelievable levels of corruption, off-the-charts income inequality, and a populace that tends to vote for politicians that don't uphold investor-friendly values.

I've long used the Heritage Foundation's Index of Economic Freedom as a quick shortcut for getting a look at whether a country is investable for the long-term or should merely be used for shorter-term trades. Countries that don't embrace free market principles are unlikely to deliver promising environments for capital formation and the protection of outside shareholders in the long run.

As such, in the part of the world I follow most closely, Latin America, we can see a pretty clear differentiation between the countries that treat foreign investors well and the ones that tend to give investors more trouble. The 2018 Heritage rankings for LatAm shake out as follows (countries with US-listed ADRs only):

- Chile - #20

- Colombia - #42

- Peru - #43

- Mexico - #63

- Argentina - #144

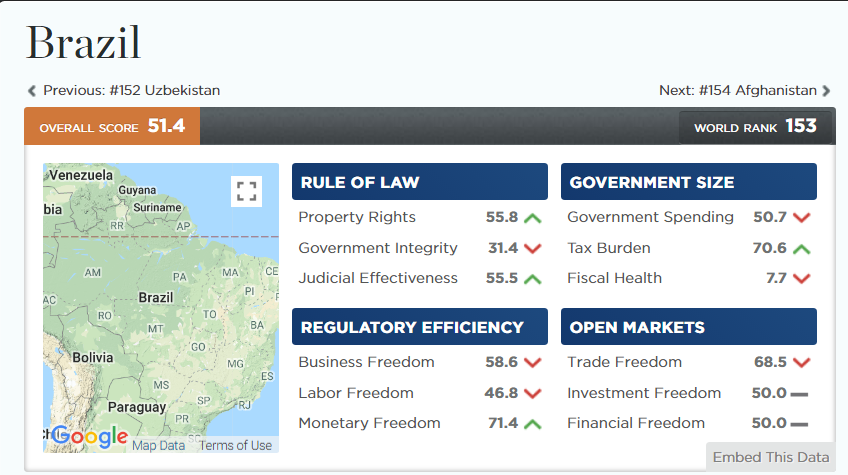

- Brazil - #153

Incredibly, Brazil, even with a "pro-markets" government in the form of Michel Temer, is ranked at #153 in the world, sandwiched between Afghanistan and Uzbekistan in the rankings.

Heritage's breakdown of Brazil's situation fails to inspire:

Its fiscal health score is particularly alarming, since even traditionally profligate spending countries like Greece (70), Italy (68), and Japan (49) score reasonably well on this metric. Brazil's combination of massive debt and near 10% of GDP budget deficits lately has the country in a league of its own.

Not surprisingly, the gigantic fiscal shortfall has led to a fresh plunge for the Brazilian Real:

That's a 20% devaluation for the year, as Brazil tries to keep pace with its neighbor Argentina in the race for 2018's worst-performing currency. Things came to a head on Thursday with Brazil's central bank intervening aggressively in the swaps market to try to prop up the value of its currency. Despite that, the Real proceeded downward, hitting fresh 2-year lows. It's also approaching new all-time lows.

Why Is Brazil Tanking?

The most obvious cause is the ongoing unrest regarding rising fuel prices. The country was paralyzed recently by a 10-day long fuel strike. Brazil is uniquely reliant on road transportation, and thus the trucking strike brought the country's logistics to a standstill, with food shortages and other major problems arising.

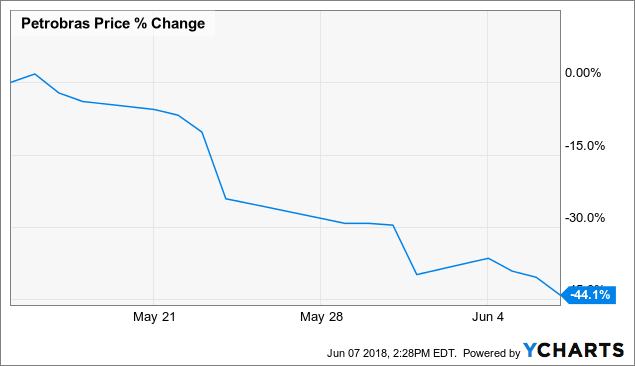

Finally, given the societal chaos, the government felt compelled to cave in. It rolled back fuel price hikes and the head of Brazilian state-run oil company Petrobras (PBR) was forced to resign. Petrobras has lost almost half its value since May 15th - pretty amazing for a company that had a greater than $100 billion market cap at that point:

PBR data by YCharts

PBR data by YCharts

Even with the fuel strike over, things have hardly gone back to normal. As The Guardian noted, the event raised questions about the stability of Brazilian democracy. Strikers were calling for a military coup to resolve the situation. Now that the incident has passed (at least for the time being), the public is questioning whether nationally important companies should be allowed to try to make profits - as the Guardian article put it:

Brazilians argue over when and how state-controlled oil company Petrobras should set fuel prices - the cause of the strike - and whether it should make money for its shareholders or swallow losses for the benefit of the nation.

As a foreign investor, this should scare you. If a country's electorate views the so-called national good as more important than the property rights of private businesses, expect your capital to get plundered sooner or later. A political system that allows property rights to be violated in that manner will almost certainly see it happen sooner or later as long as voters have a populist streak.

That brings us to the other matter - the upcoming presidential election this fall. Foreign investors have long been hyping up the Brazilian story since the current Temer government is pro-markets, and there had been hope that the next government would continue in that vein.

This, however, is not going to happen. Current president Temer is profoundly unpopular, often polling at single-digit approval ratings. Arguably the country's most popular politician would be former socialist president Lula da Silva. It appears he will be unable to run this time, however, due to corruption charges.

That leaves the frontrunner as populist right-wing firebrand Jair Bolsonaro. Originally seen by outsiders as a Trump-like figure with little chance of winning, Bolsonaro has benefited greatly from the collapsing support for the current government, and the corruption scandals on the left-wing side of the spectrum. And while his views on policing and the military may seem extreme, foreigners hoped that Bolsonaro's right-wing tendencies would extend to business matters as well.

With the fuel strikes, however, Bolsonaro stuck to his populist leanings, supporting the strikers, rather than embattled Petrobras. This has sent foreign investors into a panic, since his stance suggests that Bolsonaro will not be a reliable defender of investor interests. With the second place candidate in the upcoming election also holding anti-market views, that puts Brazilian stocks and its currency into a high-risk political position. There's a reason I avoid countries like Brazil and Argentina for much more than short-term catalyst-driven trades.

What Happens Next?

Like in Argentina last month, we'll have to see what sort of maneuvers Brazil's Central Bank can come up with to try to prop up the currency. In Argentina, two massive interest rate hikes didn't do the trick, but a third one, plus a hard floor for the Peso and a request for IMF assistance, has staunched the bleeding for now. Brazil's Central Bank loves currency swaps, and is pushing that lever hard again now, despite it seeing limited effectiveness during the 2015 currency meltdown there.

Brazil has a more difficult position than Argentina in the short-term. Temer is a lame duck president and his successor is unlikely to care about catering to foreign investors. That's a stark contrast to Argentina, where President Macri's coalition did well in the mid-term elections last year, and thus he retains a reasonable amount of political capital. And unlike Temer, Macri isn't embroiled in corruption schemes or stuck with a rock-bottom approval rating.

Also, Brazil's voters simply don't seem willing to support the sort of austerity that Argentina has reluctantly accepted. A recent poll found that more than 85% of Brazilians supported the fuel strikes, but far fewer would support the higher taxes necessary to fund lower fuel prices that the truckers demanded. Given Brazil's dismal fiscal position already, higher budget deficits are the last thing the country needs.

All this adds up to me being uninterested in investing in Brazil at this time on a country-wide basis. EWZ, the country ETF, is still way up from the 2015-16 lows despite the economy barely making it out of recession and quite possibly heading back into another one next year.

Data: Tradingeconomics.com. Yes, Brazilian stocks did move up almost 150% off the lows, thanks to GDP growth briefly topping 1% before decelerating again.

The political situation is hardly fixed - sure, it was a positive that Rousseff was kicked out of the presidency, but there's little indication that the next elected president will be all that much better. And the country's fiscal situation is dreadful.

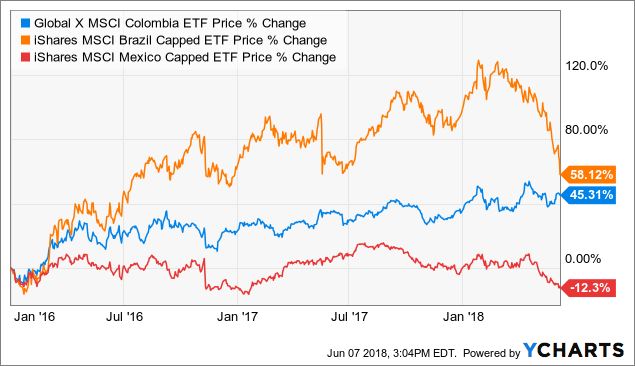

With both Colombia and Mexico at reasonable valuations, there's no reason to walk into the political minefield that is Brazil with its equity market still up so much from recent levels. Colombia's next president will be a devoted right-winger, and Mexico's, while a leftist, will have little control of the legislature and thus won't be able to create the same sort of havoc that is likely to occur in Brazil:

GXG data by YCharts

GXG data by YCharts

I do think there are some reasonable values in a couple of Brazilian companies, and a few more that are meaningfully exposed to the country though headquartered elsewhere. I've recently recommended Despegar.com (DESP) and Corporacion America Airport (CAAP), both Latin American businesses headquartered elsewhere that derive a significant amount of revenues from Brazil - and both have gotten beat up in 2018. And I bought one Brazilian company that should be relatively less affected by the current mess - see Ian's Insider Corner for more on that.

In general though, there's no reason to get too aggressive trying to buy the Brazilian drop just yet.

The stock market ran up way too far there despite a lack of much tangible economic or political progress. Just as we saw in Argentina earlier this year, misplaced optimism is now giving way to a more grim and realistic appraisal of the situation. Combined with a one-way upward trade in the US Dollar as of late, emerging markets are coming under fire more generally, and there's no rush to buy the falling knives just yet.

0 comments:

Publicar un comentario