Thoughts On The Fed Statement And Wednesday's Late Selloff

by: The Heisenberg

- What did you take away from the May Fed statement? If the answer is "nothing," well then think a little harder.

- This wasn't a complete non-event and I've got your full guide right here.

- Importantly, there's a discussion herein about the Powell "put" and how today's curve dynamics play into that discussion.

- This wasn't a complete non-event and I've got your full guide right here.

- Importantly, there's a discussion herein about the Powell "put" and how today's curve dynamics play into that discussion.

- If you were looking for something definitive from the May Fed statement, you didn't get it on Wednesday and that's probably just as well.

I'm not sure there was much utility in tipping their hand any further ahead of a fully priced June hike and amid an ongoing dollar (UUP) rally that's fueled in large part by rising rates and the assumption that as price pressures continue to build in a late-cycle environment, the Fed will be inclined to lean aggressively against inflation especially considering the possibility that fiscal stimulus will increase the odds of overheating.

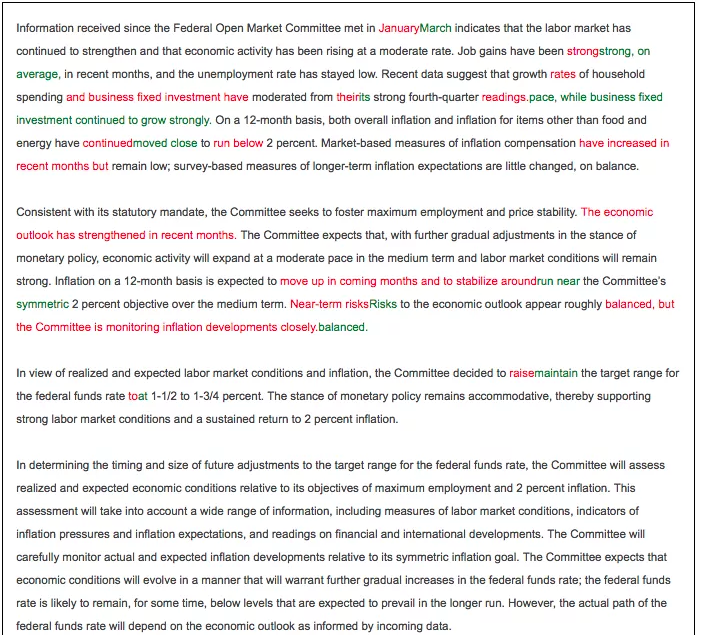

There was no avoiding a tweak to the inflation language in the statement. The Fed's preferred gauge is back to target and last week's above-consensus ECI print is further evidence to support the contention that wage pressures are building. But while the inflation outlook was upgraded, the growth outlook was more muted and the language around inflation was perhaps less inspiring (read: less hawkish) than markets were anticipating. Here's the red line:

(Heisenberg)

(Heisenberg)

As usual, interpretations varied with regard to the post-Fed market reaction, but the initial move lower in the dollar, the knee-jerk bid for bonds (TLT), and the quick spike in equities (SPY) and gold (GLD) all tipped a dovish interpretation, if not by humans, then at least by algos. Those reactions were ultimately faded and/or completely reversed. Stocks were ugly into the close:

(Heisenberg)

(Heisenberg)

Here's Bloomberg's Vincent Cignarella with the "algos" explanation:

Investors initial reaction to the FOMC statement was to buy up stocks, bonds and sell the dollar, based partly on what algos read as a Fed that was dovish on growth while maintaining its view on inflation. The omission of a reference in the March statement suggesting that the economic outlook had “strengthened in recent months” was taken as Fed second-guessing economic growth prospects. A closer examination by human eyes has revealed quite the opposite, the Fed is confident it's on the right path, prepared to hike two more times in 2018 and potentially one more time. The statement was indeed the "hawkish hold" markets were looking for.

And look, I'm not big on the whole "once the algos figured it out, things reversed course" meme.

There were plenty of reasons why human beings might have taken the statement as dovish compared to expectations.

As I wrote in the traditional daily wrapover on my site, the tweaks to the statement could plausibly be interpreted as dovish by humans and machines alike and more than a few folks agree.

“This doesn’t seem like an overtly hawkish shift in language overall,” and “it wasn’t as hawkish as markets had expected” Wells Fargo’s Erik Nelson noted.

“[The Fed] did little to forewarn that a rate hike was imminent in June and while PCE may run hotter than 2% this year, policymakers appear to be trying to tamp down expectations that such a run would warrant a materially faster pace of rate hikes,” CIBC said, chiming in.

“They also said — and I think what the market is reacting to — that market-based measures of inflation expectations remain low”, SocGen’s (OTCPK:SCGLY) Subadra Rajappa told Bloomberg in an interview, adding that “part of our expectation was that if the Fed were going to guide the market to expect a total of four hikes this year, we might start getting a hint of that in the May statement, I didn’t see it in the statement."

There's another possible read. If you look at the red line, the reference to the economic outlook having "strengthened in recent months" was omitted, and if you really wanted to, you could make an argument that while the inflation outlook was not as hawkish as some were anticipating, it still amounted to an admission that we're moving in the direction of a sustained rise to target, and when taken with the slightly less enthusiastic read on growth, there's a stagflation narrative in there somewhere. I think that's a stretch, but it's worth noting.

A more straightforward read comes from Goldman (NYSE:GS), whose Jan Hatzius simply notes the obvious, which is that the "downgrade" to the growth outlook wasn't really a "downgrade" (as such) and the inflation outlook is firming. Here are some excerpts from Goldman's post-Fed take:

The key change in the post-meeting statement was the recognition that headline and core inflation have “moved close to 2 percent,” an upgrade that was widely expected but important nonetheless. We left our subjective odds of a June hike unchanged at 90%.

In addition to the upgrade to the statement, another significant change has taken place since the March meeting: most participants who have recently been on the dovish end have made comments hinting at a shift toward the center. The stronger degree of consensus on the FOMC behind continued gradual hikes adds to our confidence that the FOMC will hike three more times in 2018, for a total of four hikes this year. We also expect four hikes in 2019.

One interesting thing to note: the 5s30s bull steepened, bouncing off a multi-year tight below 32bp on Tuesday and steepening by more than 2bp in the 10 minutes following the Fed statement.

That brings me neatly to a discussion about whether steepeners of one kind or another are a real tail risk for the market. Last week, I talked a bit about the prospects for vicious steepening later on down the road in the event a downturn forces the Fed to cut rates, undermining the dollar against a fiscal backdrop that will, by that time, have deteriorated meaningfully. At that point, there would be very real questions as to who would sponsor the U.S. long end.

Well, last Friday, Deutsche Bank's (NYSE:DB) Aleksandar Kocic was out with his latest note and in it, he suggests that for the time being, "the long end is getting stabilized [and] the tail risk is shifting from bear steepeners to bull steepeners." As noted above, bull steepening is exactly what we got on Wednesday following the Fed.

In his latest note, Kocic lists the myriad factors that support the U.S. long end. I've been over those before (specifically, in the steepening post linked above), but the idea is as follows (and I'm quoting myself here, from a post published last weekend):

Last week’s selloff through 3% on 10s notwithstanding, the long end could continue to find sponsorship for a variety of reasons including, most obviously, a safe haven bid associated with acute risk-off episodes but also the assumption of a stable currency thanks in no small part to the Fed and expectations that Fed hikes (and the accompanying USD strength) will ultimately serve to cap inflation expectations.

The idea here is that as the Fed continues to hike, risk assets will get more nervous and although "everything wants to selloff" (to quote Kocic) in an environment where central banks are pulling back from markets, equities are perhaps the least desirable asset to hold simply because that's where volatility has manifested itself in 2018.

Meanwhile, volatility has been pushed away from rates. The relative stability of long end bonds only makes them more appealing, thus ensuring they remain bid, especially at times when risk-off is the dominant market mode. The problem there is that the more well-anchored long rates are, the more ineffective Fed hikes appear and that, in turn, prompts the FOMC to continue to hike, destabilizing equities further. Here's Kocic:

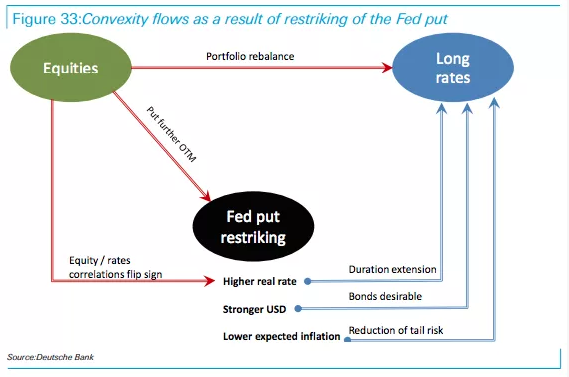

Restriking of the Fed put is a withdrawal of convexity from equities. It is effectively a removal of a put spread from the market. However, in the environment where everything is bound to sell off (a market mode that is a mirror image of QE), volatility is one of the key decision variables. More volatile equities are less desirable than less volatile duration. In that environment, convexity withdrawal creates a reinforcing loop where more turbulence in risk assets tends to cause stability in fixed income. The figure shows the convexity flows across the two markets.

This continues until equities sell off enough to meaningfully tighten financial conditions, at which point the market begins to reprice the Fed path or, more simply, take some of the additional hikes out. That represents the restriking of the Fed "put" and it would entail bull steepening - like what we saw on Wednesday.

Clearly, we're not anywhere near the type of equities selloff we would need for this to occur and indeed, June hike odds stuck at ~95% following the May statement.

Ultimately, the Fed "fireworks" (as it were) will come next month, but in the meantime, look for evidence that stocks are attempting to make their way down to a level that would force a repricing of the Fed path.

If you start to see that, you'll know the Powell "put" is in play.

0 comments:

Publicar un comentario