Ray Dalio And The 'Pretty Stupid' Cash Holders

by: The Heisenberg

- On January 23, Ray Dalio told CNBC that people holding cash are going to end up feeling "pretty stupid".

- Three weeks later, those cash holders were the only investors with positive real YTD returns.

- Fast forward three months and the very same policies Dalio cited as the likely catalysts for a "blowoff" top in equities are making cash even more attractive.

- Herein lies an irony of ironies.

- Three weeks later, those cash holders were the only investors with positive real YTD returns.

- Fast forward three months and the very same policies Dalio cited as the likely catalysts for a "blowoff" top in equities are making cash even more attractive.

- Herein lies an irony of ironies.

If you're holding cash, you're going to feel pretty stupid.

That, verbatim, is what Ray Dalio said in Davos on January 23 in an interview with CNBC.

Let me say upfront that my point here isn't to lampoon Ray Dalio. Obviously, there's a sense in which most of the investing community is always going to be "pretty stupid" if the benchmark for "smart" is Ray Dalio. I think everyone should aim high (as it were), but Jim Grant's critique notwithstanding, investors who decide to benchmark their careers against Ray Dalio are likely to come up just as short as aspiring basketball players that benchmark themselves against Kobe Bryant.

That said, everyone makes mistakes and even outside of actual, quantifiable "bad calls", everyone makes errant comments that look misguided in retrospect. The quote excerpted here at the outset is at the very least an example of the latter, if not the former.

Dalio's rationale behind the "pretty stupid" cash call was simple. It was predicated on the assumption that the "Goldilocks" environment of still-subdued inflation and synchronous global growth would continue in the near- and medium-term, and between late cycle stimulus in the U.S. and buybacks, markets were headed for the fabled "blowoff" top (if you watch the interview, he actually uses the term "blowoff").

Well, not to put too fine a point on it, but that call could scarcely have been more poorly timed.

The market peaked 72 hours later and that inflation Dalio said "isn't a problem" became a "problem" a week later when the above-consensus average hourly earnings print that accompanied the January jobs report exacerbated the ongoing bond rout on the way to catalyzing the mayhem that unfolded on Friday, February 2, spilled over into the following Monday, and culminated that Thursday in the second 1,000 point down day for the Dow in the space of a week.

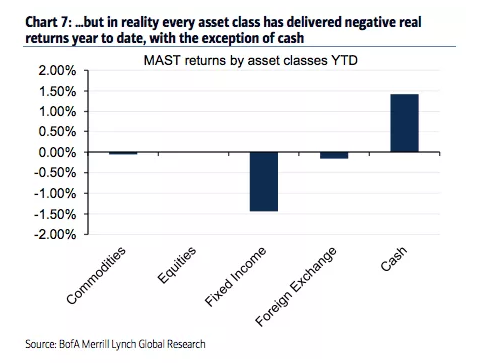

Through February 12, Ray's "pretty stupid" people were the only ones with positive real YTD returns:

(BofAML)

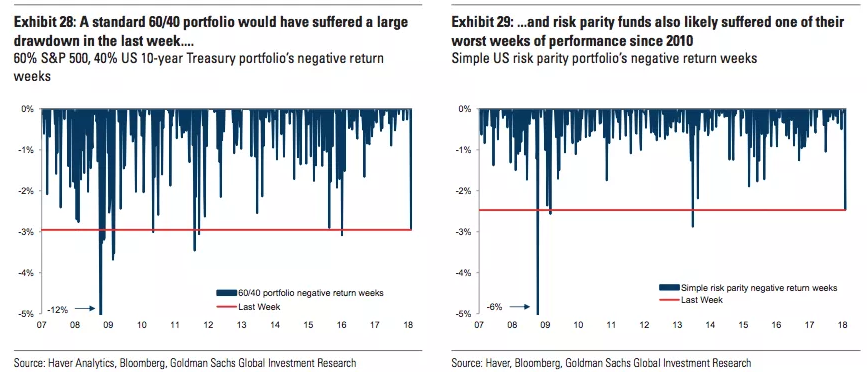

The reason I bring this up is because it has implications for the debate about what the "pain threshold" is for 10Y yields (TLT). That discussion was front and center this week as yields on 10s touched 3% for the first time in four years, a "milestone" (if that's what you want to call it) that left everyone asking the same questions they were asking in February when the bond rout finally spilled over into stocks, leading to one of the worst weeks for balanced portfolios and risk parity (and when you think risk parity, think about Dalio's Bridgewater, although I don't profess to know how he performed during that week) in years:

(Goldman)

That's what's colloquially known as "diversification desperation" and it occurs when the stock-bond return correlation flips sustainably positive, or, more simply, when bonds and stocks selloff together.

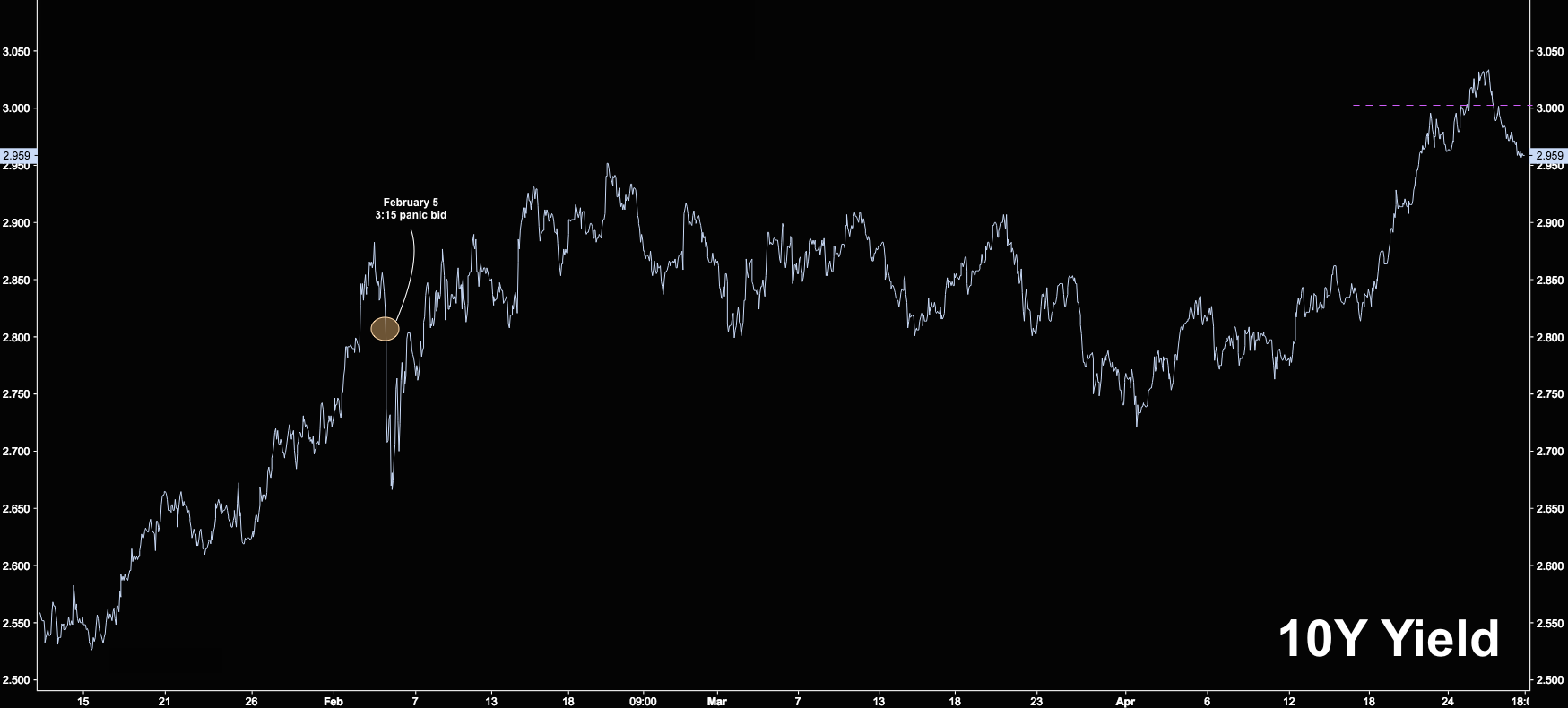

There's a vociferous debate going on right now about what level on 10Y yields is the tipping point beyond which stocks get hit. Again, this discussion has popped up again because this week, we eclipsed the February highs:

(Heisenberg)

I'm not going to get into the weeds with regard to where the "danger zone" for stocks is vis-à-vis 10Y yields. Rather, what I want to point out here is that while there are a number of factors that will ultimately support the long end (i.e., entice buyers and cap yields), it's possible that the safe-haven appeal of 10Y Treasurys in an equity rout may be diminished by the increasingly attractive proposition of simply holding cash.

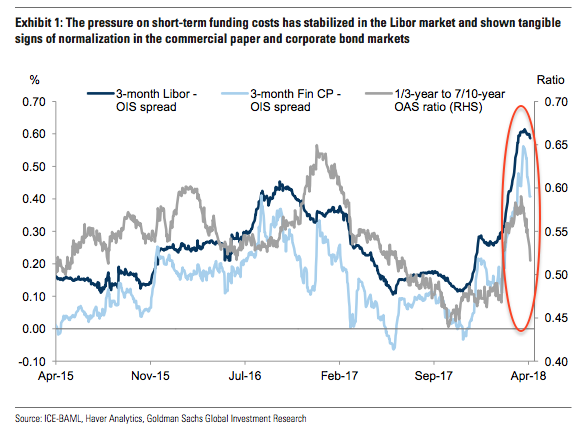

What Dalio seems to have missed (and actually, I doubt he "missed it" as much as he just didn't think this was particularly relevant for most investors), is that the very same factors he cited as the catalysts for the "blowoff" phase of the equity rally contributed to a short-term funding shock that looked like this in Q1:

(Heisenberg)

I talked about that at length on several occasions this month and last, but as Goldman notes, there's now a general consensus about what drove what you see in that chart. To wit, from a note out earlier this week:

A broad consensus has emerged among market participants that three key drivers fueled the first quarter funding pressure:

Each of these factors contributed to some degree to what we think will prove a temporary supply/demand imbalance in the corporate bond and money markets.

- The change to the tax treatment of foreign earnings from US companies;

- Changes to the Base Erosion and Anti-Abuse tax (i.e., BEAT);

- The surge in T-bill issuance.

All of that is related to the tax bill and to the spending bill. In other words, it's all related to the same fiscal stimulus that Dalio (and many others) suggested would help spark the mythical "blowoff" top in U.S. stocks (SPY).

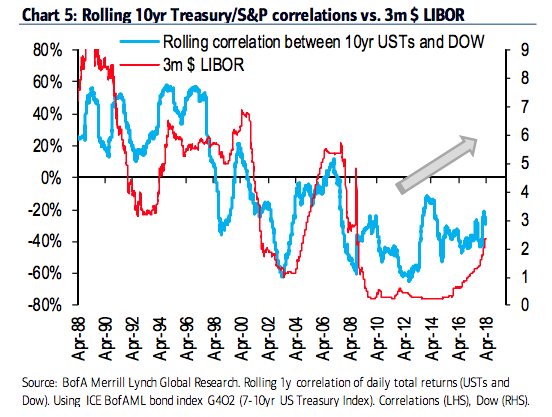

Well, as BofAML writes in a new note, the correlation between 10Y Treasury returns and U.S. stock returns tracks the evolution of 3m LIBOR. Consider this:

The typical haven characteristic of Treasury debt is being hindered by the appealing rates of return on cash in the US. Historically during periods of market turbulence, money would flow from risky assets (such as stocks) into US Treasury bonds. But with $ Libor at 2.36%, support for Treasury debt is diminishing (consider that 5yr Treasury yields are 2.84%). In other words, the rise of “cash” as an asset class is altering the traditional allocation decisions of multi-asset investors in times of market stress.

Chart 5 highlights this point. We show the rolling 1yr correlation between total returns on 10yr Treasury bonds and the total returns on stocks (daily returns). We overlay this with the evolution of 3m $LIBOR.

The implication there, in case it isn't obvious, is that haven demand for U.S. Treasurys will diminish as the attractiveness of cash as an alternative rises, and the result will be that the stock-bond return correlation will be more prone to being positive, thus exacerbating the above-mentioned "diversification desperation" and imperiling the very assumption that underpins risk parity and balanced portfolios.

Again, the irony there is that it's the distortions from the tax changes and the spending bill that are in part behind this dynamic, and if I had to extrapolate further (which I don't, but I will anyway), what I would also venture to suggest is that the late-cycle fiscal stimulus will probably force the Fed to get more aggressive than they otherwise would have, thus driving short-end rates higher still and making cash even more attractive relative to long-term bonds which will continue to selloff as inflation pressures mount.

So while the jury is certainly still out on whether the folks holding cash will indeed feel "pretty stupid" as Dalio explicitly predicted back in January, one thing's for sure: they're not feeling "pretty stupid" as of right now.

0 comments:

Publicar un comentario