It's Official: 'Buy-The-Dip' Has Failed

by: The Heisenberg

- The Pavlovian mentality has officially been undermined in 2018 according to one model of a "buy-the-dip" strategy.

- The implications of this are profound, but most immediately it suggests a return to the low volatility regime that made 2017 one of the calmest years on record is unlikely.

- Here is a comprehensive look back at how "buy-the-dip" went from a derisive meme to viable strategy.

- And here is how and why it failed this year, visualized and quantified.

- The implications of this are profound, but most immediately it suggests a return to the low volatility regime that made 2017 one of the calmest years on record is unlikely.

- Here is a comprehensive look back at how "buy-the-dip" went from a derisive meme to viable strategy.

- And here is how and why it failed this year, visualized and quantified.

One of my favorite subjects to write about when it comes to markets is how "buy the dip" went from a derisive meme aimed at maligning purportedly uninformed retail investors for their propensity to view any decline in equity prices as an "opportunity", to a viable strategy underwritten somewhat explicitly by monetary authorities.

Whenever I have this discussion with people either online or, on the increasingly rare occasions when I find myself in contact with actual human beings operating in what used to be humanity's natural habitat (i.e., in the real world as opposed to in the digital void), I always have to preface it by saying that I do not subscribe to wild conspiracy theories about central banks and stocks. I am certain this plea will be summarily ignored by at least some readers, but I implore you to spare me your theories about Fed officials trading futures from their basements or Kuroda moonlighting as an FX trader and buying any dips in USD/JPY when markets are in turmoil.

There are of course times when some manner of intervention is necessary/desirable and yes, overt intervention in markets by authorities is obviously a real thing. But the whole "plunge protection team" narrative has taken on an absurd life of its own over the past decade or so, and I think it's important that people retain some perspective. Yes, markets are sometimes manipulated both by authorities and by bad actors who are not authorities. Sometimes, instances of the latter can indeed be called "conspiracies." But every seemingly inexplicable tick or errant print isn't evidence of "manipulation" or a "conspiracy."

Sometimes, things just happen - that's what a "fat finger" is and you should get used to that, because thanks to modern market structure, dominated as it is by algos, it's going to happen more and more often. Innovations in market structure have also raised questions about liquidity provision, and if critics are correct to say that liquidity will be increasingly prone to evaporating when we need it most, seemingly anomalous events (read: flash crashes and flash "smashes", as it were) are almost certain to occur with increasing rapidity. Those are just the facts of life in modern markets, and while it's always possible to couch everything in conspiratorial terms (the HFT lobby is, in some ways, its own conspiracy), I think it's critical that people keep some perspective.

Allow me one quick caveat to those points. In China, there is a literal plunge protection team. It's called "the national team" and it does indeed step in to support markets at key junctures in order to, among other things, keep stocks stable around important political events. That's not a secret, nor is it a conspiracy. Everyone knows it and there's no real effort on the part of Beijing to hide it.

So having said all of that, there has of course been an ongoing, coordinated effort by developed market central banks to inflate the prices of risk assets since the crisis. As I never tire of reminding you, that is the furthest thing from a conspiracy imaginable. It's how QE works and for anyone who was unfamiliar with the mechanics, it was explained very explicitly in a 2010 Op-Ed in the Washington Post by Ben Bernanke called "What The Fed Did And Why." That Op-Ed contains this passage:

This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.

If central banks driving stock prices higher and deliberately suppressing corporate borrowing costs is a "conspiracy theory", well then Ben Bernanke is a "conspiracy theorist". And if, to take the other side of the argument, this was supposed to be some kind of a closely-held secret that only central bankers knew about, well then Ben Bernanke is the worst co-conspirator in the world. I don't know about you, but I don't want to be in a "conspiracy" with a guy who writes an Op-Ed for the Washington Post called "What We Did And Why."

The point is, "yes" there has been an ongoing effort on the part of central banks to inflate stock prices (SPY) and catalyze a global hunt for yield that ends up driving everyone down the quality ladder with the effect of leaving everything priced to perfection in fixed income. But "no", that is not a conspiracy. Again, it's literally how accommodative policy works.

Ok, so what was implicit in Bernanke's Op-Ed and in pretty much anything else you want to read on this subject is that at a certain point, this whole endeavor runs on autopilot. The whole idea here is to create a self-sustaining recovery and foster self-feeding loops. You don't want to have to cut rates and/or buy assets in perpetuity, because eventually, you'll end up like the BoJ - cornering entire markets and finding yourself at risk of owning the entire free float of publicly traded companies. Or you'll end up like the ECB - creating a situation where € junk bonds trade inside of U.S. Treasurys (TLT).

Part of the problem - and I've been over this a thousand times if I've been over it once - is that central banks overestimated the efficiency of the transmission mechanism between asset price inflation and the real economy and underestimated the efficiency of the transmission mechanism between accommodative policies and financial assets. In other words, they assumed the "trickle down" from asset price inflation would work faster than it did and they seemed to have thought the market's propensity to frontrun $20 trillion in liquidity would be less enthusiastic than it turned out to be, a rather odd assumption to make given that rational people are always going to frontrun a perpetual bid from a determined, price insensitive buyer. Especially one that's armed with a printing press.

Again, the frontrunning of accommodation is to a certain extent desirable as it represents the autopilot effect which is the point of this whole post. The problem is that if asset price inflation takes too long to trickle down (i.e., takes too long to translate into the type of real-economy outcomes central banks are ostensibly chasing), then the risk is that bubbles inflate as the effects of accommodation become disproportionately concentrated in asset prices. The ultimate irony inherent in that setup is that a bursting of those bubbles could end up being the source of the next downturn and if that downturn shows up before central banks have had a chance to replenish their countercyclical ammo, well then it's not clear how they will respond.

In the U.S. experience, the Fed has "succeeded" (and I use the scare quotes there because there are dangers inherent in this success) in creating a reflexive relationship with markets via a two-way communication loop that effectively gives markets a say in the future course of normalization. This is the relationship described by Deutsche Bank's Aleksandar Kocic in a seminal 2015 note on the "removal of the fourth wall." Here are the key quotes from that note (referencing the September 2015 Fed meeting, which came amid the chaotic fallout from the devaluation of the yuan a month prior):

Going into the FOMC meeting, we had to face multiple nested contingencies, from Fed reaction function, to ambiguous signals given by the economic models which largely underwent structural breaks post-2008 and eroded market's already low confidence regarding economic forecasts. The Fed decision showed that when everything fails, common sense remains the best guide. And common sense prevailed.

This changes everything. Power relations have been revealed; nothing will ever be the same. In that sense, despite seeming status quo, the FOMC was a true Event in the sense of being an encounter which retroactively creates its own causes.

What we now have is another data point which outlines the contours of the Fed reaction function. Fed's communication strategy, it is becoming clear, is an equivalent of what in theater context is referred to as Removing the fourth wall whereby the actors address the audience to disrupt the stage illusion - they can no longer have the illusion of being unseen. An unalterable spectator becomes an alterable observer who is able to alter. The eyes are no longer on the finish, but on the course - what audience is watching is not necessarily an inevitable self-contained narrative. The market is now observing itself from another angle as an observer of the observer of the observers.

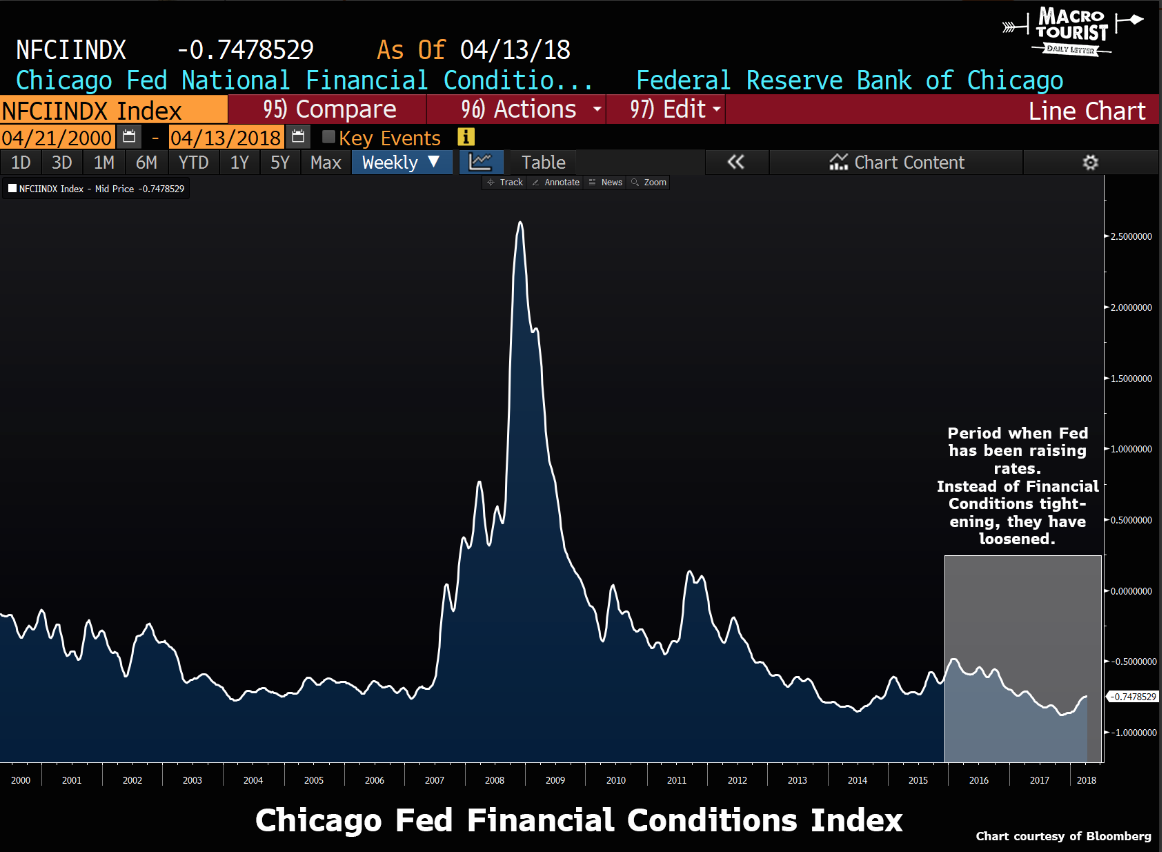

That framework has proven to be exceptionally instructive in thinking about the market's reaction to the Fed hiking cycle and it helps to explain how financial conditions managed to get looser as the Fed tightened:

(Bloomberg, with annotations from Kevin Muir)

Without getting too much further down the rabbit hole here (too late!), the point is that after a certain amount of time, the reflexive nature of the relationship between the Fed and markets created a series of self-feeding dynamics that optimized around themselves, culminating in a volatility seller's paradise and transforming "buy-the-dip" from a derisive meme applied to retail investors into what became not just a viable strategy, but in fact a nearly infallible law.

Allow me to quote myself on this:

The increasing rapidity with which intermittent volatility flareups collapse has been a defining feature of markets over the past couple of years and this dynamic has become especially prevalent since Brexit.

Part and parcel of that dynamic is the idea that the central bank put has become self-sustaining – it runs on autopilot. Why wait on dovish forward guidance (or any other signal from the monetary gods) to buy the dip when you know with absolute certainty that in the unlikely event a drawdown proves to be some semblance of sustainable, policymakers will calm markets? If you know it’s coming, well then you should buy the dip now. This becomes a recursive exercise as everyone tries to frontrun everyone else and before you know it, dips and volatility spikes are mean reverting at a record pace as the prevailing dynamic optimizes around itself.

In short, the two-way communication loop between policymakers and markets became a self-fulfilling prophecy over the past couple of years. Markets became so conditioned to policymaker intervention and dovish forward guidance at the first sign of trouble that no one saw any utility in waiting around for it anymore.

And here's how BofAML puts it in a note dated April 10:

A key factor that created 100yr+ records in terms of low equity volatility last year was the moral hazard injected by central banks teaching investors that buying equity-dips (or selling equity volatility spikes) was "free-money". This led to complacency among investors that risk was not real, resulting as we argued in our 2018 outlook, in an unsustainable "low volatility bubble".

Well, you might have noticed that things aren't "mean reverting" as quickly as they used to.

That is, while markets recovered from the February correction, things got tumultuous again, as trade war bombast collided with domestic political turmoil and Syria concerns to destabilize markets anew. So far, the "Powell put" is missing in action and probably will remain so up to and until equities decline enough to squeeze financial conditions materially, forcing the market to take some hikes out of the curve, thus restriking the Fed put for Powell.

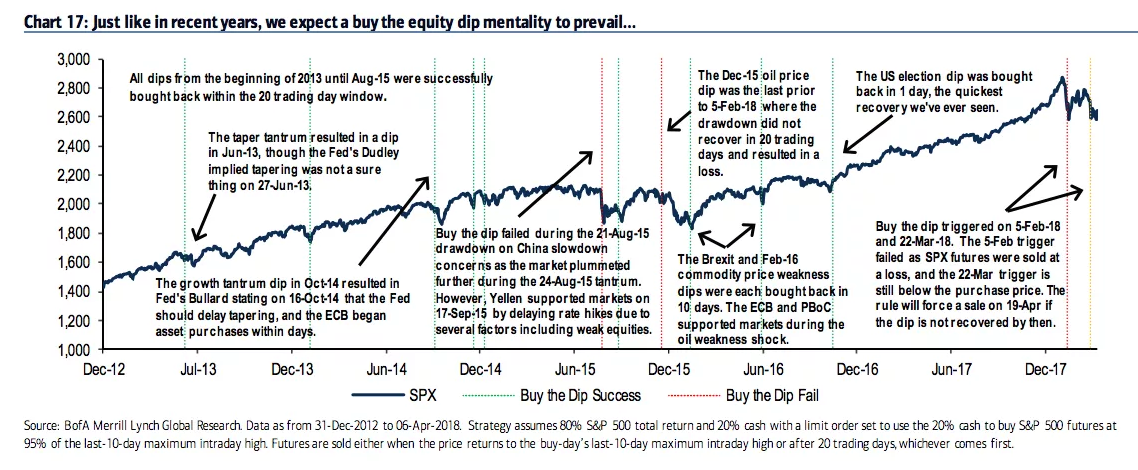

Ok, well in the meantime, BofAML is out suggesting that "buy-the-dip is failing." In the same note mentioned above, the bank is out reassessing a trading strategy based on all of the dynamics described above. Here's how it worked:

In 2017, we showed how a simple trading strategy of holding cash and buying any 5% dip in S&P futures until either the market retraced or 20 trading days passed outperformed the S&P on a risk-adjusted basis consistently since 2014. This was in contrast to 2011-2013 when this simple strategy failed to outperform, and demonstrated a change in market dynamics towards faster shock recoveries and shallower dips.

See what I mean when I said, above, that "buy-the-dip" has literally been transformed from a derisive market meme applied to retail investors to a viable, indeed seemingly infallible, strategy?

Ok, well guess what? That strategy has faltered this year. Here's BofAML's annotated chart:

(BofAML)

Over there on the right-hand side, you can see that "buy-the-dip" (as defined above) has seemingly stopped working. Do you want more details? Ok, that's fine. BofAML has them for you along with some more fun visuals. To wit:

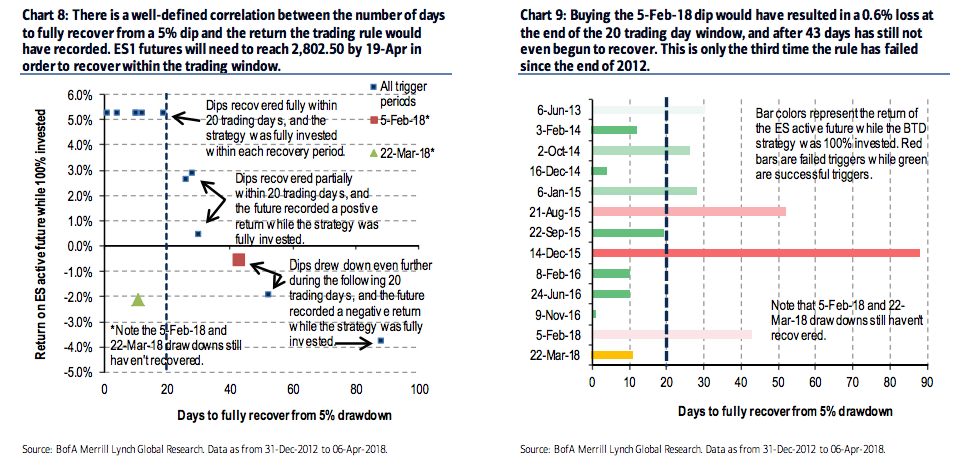

The 5-Feb-2018 trigger seems most similar to the 21-Aug-2015 shock (China slowdown scare), which lost 1.93% upon liquidation at the end of the 20 trading day window and ultimately took 52 days to fully recover (Chart 8 and Chart 9). Looking at the recent 5-Feb shock, we are 43 days in and the market is down an additional 1.63%. However, in comparison, after 43 days into the Aug-15 shock the S&P had actually recovered about 2%. While in ‘15 Chair Yellen supported markets by announcing a delay of rate hikes due to concerns about China and equity weakness, today few expect Chair Powell to step in to support stocks. Our trading rule triggered for a second time in 2018 on 22-Mar, and as of 6-Apr we are 13 days into the 20 day investment window. At current prices, the trade has lost 2.13%. In order for the dip to fully recover within the window, S&P E-mini futures (ES1) would need to cross 2,802.50 by 19-Apr, over 7% above 6-Apr’s closing level of 2,605.75.

Note the bit about Yellen in there. That "support for markets" in 2015 that BofAML mentions is what Kocic was referencing in the 2015 noted cited above.

So, according to BofAML's model of one "buy-the-dip" strategy, the spell appears to be broken and one thing that should be readily apparent from everything said above is that once the market starts to believe the game is up, the psychology that underpins the self-feeding nature of this dynamic goes into reverse. Here is BofAML one more time, explaining what I just said in the context of a potential return to the low volatility regime:

Importantly, even if US equities do end up recovering to set new highs in 2018, perhaps on the back of a strong earnings season, simply breaking the trend of rapid recoveries (and the Pavlov BTD mentality), should prevent a return to the 2017 bubble lows in volatility.

There you go. So while all of this needn't necessarily mean that U.S. equities can't make new highs, what it does mean is that betting on rapid "mean reversion" on any volatility spike isn't likely to work out as well as it did in the past. Indeed, a return to the conditions that made last year one of the calmest on record by all manner of measures simply isn't likely.

0 comments:

Publicar un comentario