Italy’s new rulers could shake the euro

If it were to crash out of the single currency and default, the damage would be huge

Martin Wolf

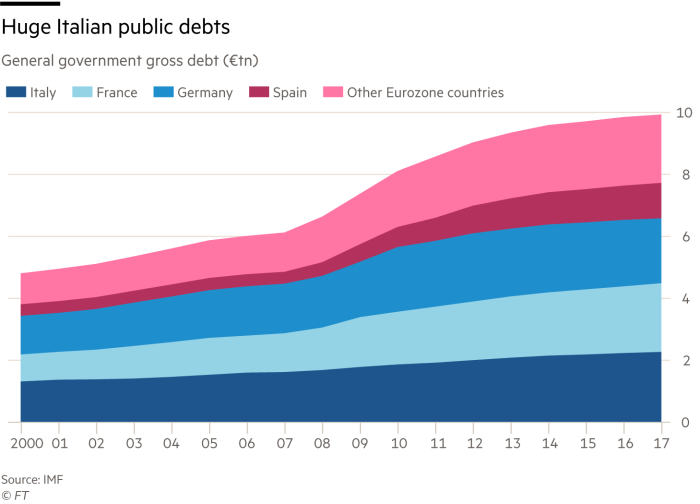

Italy is not Greece. But not all the differences are encouraging. Its economy is 10-times bigger. Its €2.3tn public debt is seven-times bigger; it is the largest in the eurozone and fourth largest in the world. Italy is too big too fail and may be too big to save. The question is whether its new government will trigger such a crisis and, if so, what might follow?

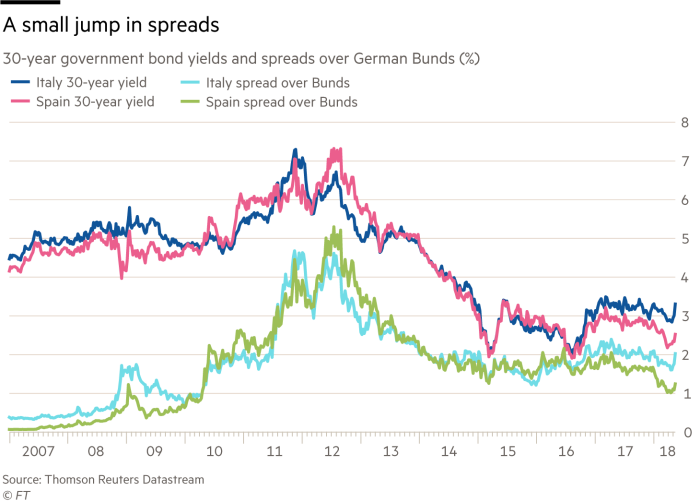

So far markets are only slightly nervous. On Monday, yields on 30-year Italian government bonds were just 220 basis points above German levels, with yields of 3.4 per cent. This is far below peak spreads of 467 basis points and peak yields of 7.7 per cent in 2011. Alas, it could get far worse. (See charts.)

According to the European Council on Foreign Relations, in no member state of the EU, bar Greece, did the sense of “cohesion” of individuals with the EU fall more sharply between 2007 and 2017 than in Italy. By the latter year, its ranking on this criterion had tumbled to 23rd of 28 members.

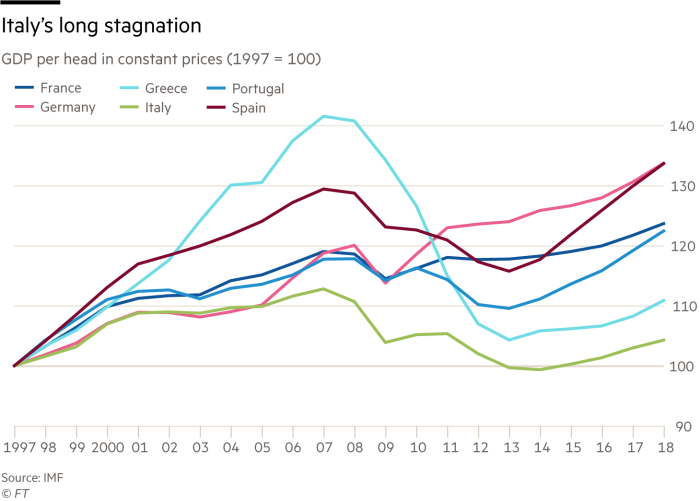

This is not just due to the economic crisis. Between 1997, when the eurozone was launched, and 2017, Italy’s real gross domestic product per head rose 3 per cent — a worse performance than that of Greece. Italians also feel they have been abandoned to cope with their migration crisis largely on their own.

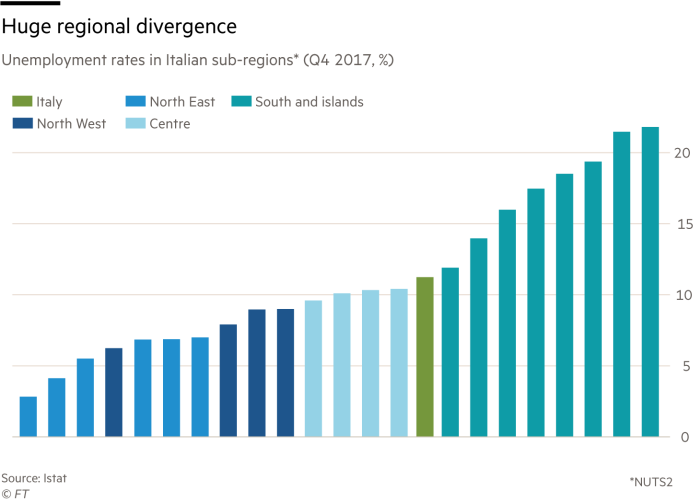

Many Italians, in brief, feel semi-detached from the EU. They are also contemptuous of their establishment. This is why an intellectually incoherent government of leftwing and rightwing populists have gained power, the former stronger in the south, the latter stronger in the north — a division explained by sharp regional economic divergences.

This mess is the fault of both Italy and the EU. The latter has failed to achieve target inflation or generate adequate demand. This has made it difficult to achieve necessary post-crisis adjustments in competitiveness. Germany’s refusal to recognise that these are problems has made things far worse. But Italians also failed to understand the necessity of radical economic and institutional reform if Italy is to thrive, especially in a currency union with Germany.

It may be too late. The spiral of populism is: unhappy voters; irresponsible promises, bad outcomes; even unhappier voters; still more irresponsible promises; and worse outcomes. The story is not over. It may have just begun.

The Five Star Movement and the League’s common programme contains enough to spark conflict with the EU and the eurozone: higher spending, lower taxes and assaults on eurozone fiscal and monetary rules. Bruno Le Maire, French finance minister, has already sounded the alarm. Matteo Salvini, hardline leader of the League, responded briskly that: “I didn’t ask for votes . . . to continue on a path of poverty, precariousness and immigration: Italians first!”

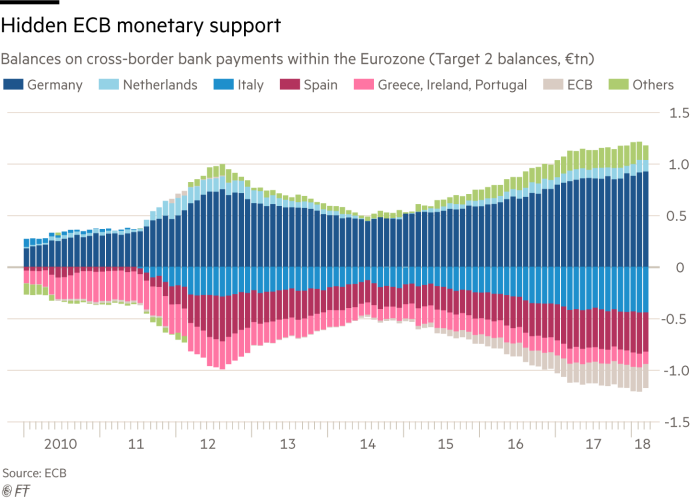

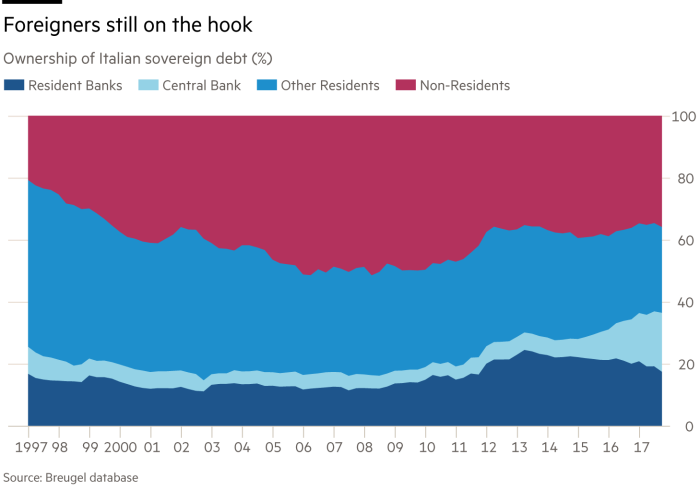

The complacent assumption is that creditors will rule. If the new government were to break the rules, the European Central Bank could not help it. In a clash, financial instability would bring the Italians to heel. But this is only true if the Italians are unwilling to employ the doomsday weapon of default. Non-residents owned €686bn of Italian government bonds (36 per cent) at the end of 2017. Moreover, in March 2018, the Italian central bank owed partners — the Bundesbank, above all — a further €443bn in the “Target 2” system. Today, debtor and creditor positions inside the European System of Central Banks surpass their scale during the crisis of 2012.

If Italy were to crash out and default, the damage could be huge. Yet even this ignores the wider economic, not to mention political, impact. It will be harder to bully Italy than Greece, largely because Italexit is obviously a far more dangerous proposition than Grexit.

So what might happen? One possibility is that Giuseppe Conte, the proposed prime minister, will lead a conventional government. Alternatively, the government will back down at the first whiff of gunpowder. But it is also possible that it will persist with its policies, triggering a run on Italian debt and Italian banks. Without ECB support, that could force limitations on the transferability of bank money outside the country or on its conversion into cash. Italy would effectively fall out of the eurozone.

This would be a monstrous crisis. Would the government then back down? Again, probably so. But the damage to confidence might take years to reverse. The Italian economy would lose its limited forward momentum and go into reverse. The flight of capital, people and businesses could be devastating. Given all this, another election might see the emergence of a still more radical government or, at worst, the unity of Italy might come into question.

Would such a long-running Italian crisis be contained in this one country? Again, possibly so.

Yet, in a serious crisis, other countries might be affected. Note that Spain too has increasing debts within the ECB’s Target 2 system. The pressure on the eurozone could become substantial: reform or perish.

In 1991, I argued of monetary union: “The effort to bind states together may lead, instead, to a huge increase in frictions among them. If so, the event would meet the classical definition of tragedy: hubris (arrogance), ate (folly); nemesis (destruction).”

Many Italians do blame Europe for their plight. That may be unfair, but it is inevitable, since so many of the decisions that now affect them are made in Europe. The attempt to break out of the straitjacket, for which they have now voted, seems sure to fail. But that will not resolve the crisis. It could even make it worse in the long run. Until Italy regains prosperity, its politics and its place in Europe will stay fragile. Anything can happen.

0 comments:

Publicar un comentario