Black Swan? The 'Vicious Steepener' Risk

by: The Heisenberg

- Everyone wants to talk about the relentless flattening of the U.S. curve.

- What very few people seem to realize is the extent to which the current dynamic may be setting the stage for a dramatic steepening episode down the road.

- If you're looking for an underappreciated risk, here's one for the ages.

- What very few people seem to realize is the extent to which the current dynamic may be setting the stage for a dramatic steepening episode down the road.

- If you're looking for an underappreciated risk, here's one for the ages.

There's been a ton of chatter lately about relentless flattening in the curve and what it might or might not portend for the U.S. economy.

Although the 2s10s steepened for three straight sessions to close the week, that was off a decade low of just ~41 bps on Wednesday.

(Heisenberg)

This has become a veritable obsession for pundits, even as analysts have variously attempted to take a more nuanced approach by trying to discern whether a flat or inverted curve necessarily means what it used to or otherwise has the same predictive power it may have had in past cycles.

Here's what one analyst I spoke to over the weekend had to say:

I think in general this whole discussion about curve inversion as a predictor of recession is incorrect. I mean, there was some connection in the past, but causation has changed. The connection no longer holds. Even in 2007, the curve inverted for different reasons; it didn't know about the recession, otherwise we would have avoided it.

Whatever the case, there likely won't be much in the way of respite from the flattening in the near term. In other words, the transitory bout of steepening we saw on Thursday and Friday is likely to be just that - transitory. Here's Bloomberg's Brian Chappatta, from his week ahead preview (usually out on Sundays, always free, and always worth a read, by the way):

The U.S. will issue a combined $96 billion of two-, five- and seven-year notes this week, the largest slate of fixed-rate coupon sales since 2014, according to BMO Capital Markets. After a stretch dominated by Federal Reserve speakers, the offerings are likely to refocus traders on the prospect of ever-larger auctions to cover swelling budget gaps.

That outlook will be hammered home next week, when the Treasury releases its latest financing estimates for the current and upcoming quarters. With trillion-dollar deficits just around the corner, the department’s forecasts could very well be market-moving.

And this is where this discussion gets interesting if you step back and think ahead. I've talked a lot over the past six or so months about the dangers inherent in piling fiscal stimulus atop a late cycle economy (see here and here, for instance). There's likely to be a sugar high for economic activity, but that comes at a cost; literally, in the sense that the current round of expansionary fiscal policy is deficit-funded.

As you're probably aware, the latest CBO forecasts show the deficit hitting $1 trillion two years earlier than previously expected as a result of the tax cuts and extra spending measures.

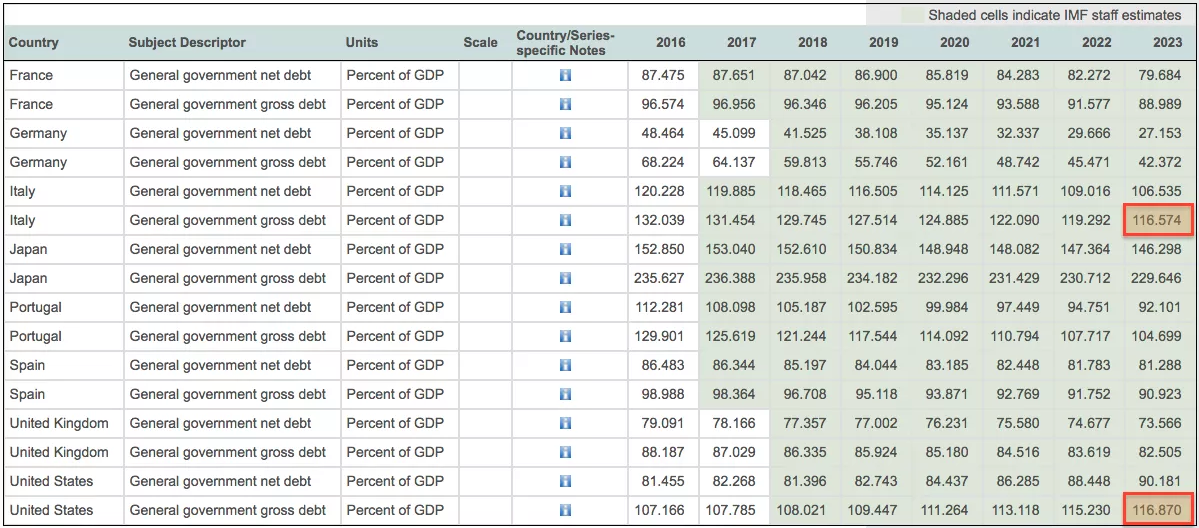

The tax cuts and the spending are likely to juice the economy in the near term, but it's doubtful they will pay for themselves via growth effects over the longer haul. According to the IMF, the U.S. fiscal position will be worse than that of Italy, Mozambique and Burundi by 2023:

Needless to say, the stimulus risks stoking inflation and thereby forcing the Fed to hike more aggressively than they otherwise might. Here's an excerpt from a new piece by Brookings:

The U.S. economy remains in robust shape, with growth in GDP, industrial production, and investment holding up well. In tandem with strong consumer confidence and employment growth, wage and inflationary pressures have picked up slightly, although less than would be typical at this stage of the cycle. The U.S. is engaged in a perilous macroeconomic experiment, with the injection of a significant fiscal stimulus even as the economy appears to be operating at or above its potential.

The Fed is likely to lean hard against potential inflationary pressures as this stimulus plays out. Export growth has been buoyed by a weak dollar and strong external demand, but the U.S. trade deficit has still risen over the past year.

As the Fed hikes to ward off inflation pressures, those hikes will of course drive short-end rates higher, thereby supporting the dollar and underpinning demand for the long-end (between favorable rate differentials and the safe haven appeal of U.S. debt, Treasurys will be an attractive asset even as the fiscal outlook for America worsens and even as the administration's trade doctrine amounts to a weak dollar policy by proxy). This dynamic will lead to more flattening in the near to medium term.

But this presents a palpable (and likely underappreciated) set of concerns. The buildup in duration and the perpetuation of the bond trade more generally creates an ever larger tail risk.

What you have to ask yourself is where the bid for the long end is going to come from when the U.S. finally does enter a recession against a backdrop where America's fiscal position has ventured into uncharted territory and the dollar suddenly loses support from a Fed that will be forced to cut rates to counter the downturn. Here's Deutsche Bank's Aleksandar Kocic, from a note out Friday:

In contrast, in the current cycle, the main driver of the flattening trend is essentially the strong USD – as long as the currency remains stable, the sponsorship for the US long end is likely to be uncontested. This becomes problematic when the USD begins to weaken significantly and that can come on the back of either higher inflation or possible recession or a general weakening of the economy. Fed hikes in this case act as a stabilizer – rate hikes are both supportive for currency and potentially prevent higher inflation.

Nevertheless, persistence of the current trend is a cause of buildup of tail risk. As we are expecting a continuing fiscal easing and deficit spending in the future in the environment of economic expansion, when the recession kicks in, Fed would have to cut rates. The logical question is: who will sponsor the long end of the US curve in an economy with potentially weaker currency? Long yields would likely fail to rally or could even sell off in an easing cycle. The persistence of Fed hikes and curve flattening could become an incubator for vicious steepeners in the future.

See what I mean? The current environment is conducive to the continual sponsorship of the U.S. long end as Fed hikes are supportive of the dollar even against the deteriorating fiscal outlook. Those same hikes serve as a check on inflation. This could encourage crowded positioning (i.e., the buildup of tail risk) which in turn raises the stakes further in the event the economy finally falters, forcing the Fed to cut rates, thereby allowing inflation to materialize and potentially undercutting the currency against a backdrop where the fiscal picture is the worst it's ever been.

In that scenario, the bid for the long end of the U.S. curve may evaporate completely, leading to dramatic steepening and opening the door for a supercharged version of the spike in cross-asset volatility we saw in early February during the brief inflation scare that accompanied the above-consensus AHE print in the January jobs report.

0 comments:

Publicar un comentario