"My best regards to dollar bears": Bulls cheer buck’s resurgence

Bets against the dollar feel the heat, with more gains now expected

Katie Martin

The dollar is back, and those who had always kept the faith in the currency are running a victory lap. With bells on.

The dollar index, which tracks its value against a basket of other major currencies, is now up by 2.4 per cent from the middle of this month to reach its highest point since early January. The euro, meanwhile, continues to sink in the wake of the latest European Central Bank press conference, which delivered a note of caution, albeit measured caution, over the region’s economic soft patch.

“My best regards to all dollar bears,” writes Ulrich Leuchtmann, currencies analyst at Commerzbank. (A saucer of milk for Table 12 please, thanks.)

He continues:

The amount of ridicule, malice and criticism my colleagues and I had to face over the past months, was overwhelming! Our view that the dollar depreciation in December and January was fundamentally unfounded, that the market would not be able to ignore the dollar-positive arguments forever and that therefore we would see a recovery of the US currency was rejected by many: by readers, by clients, by colleagues.

I have to admit that in view of a wall of dollar bears I too had my doubts sometimes — as I am happy to admit. Perhaps everything really was going to be different this time round? Perhaps I had overlooked important arguments or mistakenly dismissed them as circumstantial? Perhaps the whole approach of our FX analysis was incorrect after all?

So it makes me particularly happy to see that the development of the markets is now proving us right.

Yep, we got that last bit. But he’s not done…

All these fabricated, sometimes absurd arguments that were used at the start of the year to extrapolate and justify dollar weakness have collapsed (a) because they are devoid of content and (b) because the development of the exchange rates can no longer disguise the fact this fact. As a result the dollar recovery is a self-perpetuating process. In a way it could be claimed that the dollar weakness was a speculative bubble that is currently bursting.

A Fed that is on track for several more interest-rate rises this year (compare and contrast with the ECB) and robust US inflation both mean that the buck can keep climbing from here, he said, quite aside from the rise in US bond yields, which he considers to be a distraction.

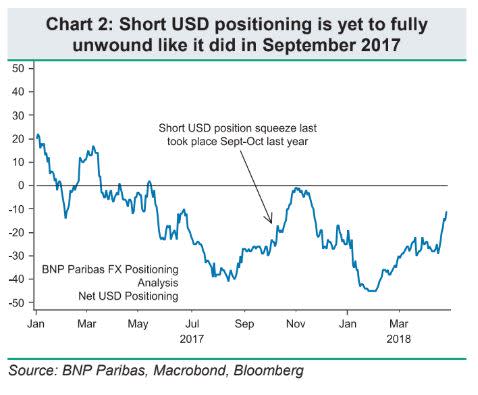

Michael Sneyd at BNP Paribas, meanwhile, argues that fickle traders have abruptly latched back on to signals from the US bond markets as a driver for the buck. “US rates didn’t matter for the dollar, now they do,” he said, adding that bets against the currencies are now folding under unbearable pressure.

We do not see events over the weeks ahead triggering a return to the weaker dollar theme, unless the FOMC delivers a dovish surprise on 2 May, which we consider unlikely, or April’s non-farm payrolls disappoint sharply (again, we do not expect this). Rather, we view that a catalyst for a euro or yen recovery would need to come from Europe or Japan in the coming weeks, which also appears unlikely.

ING sympathises with those who are caught on the wrong side of this, saying it “had thought the end point to the Fed policy cycle was nearly priced, but instead short rates are still moving and making dollar hedging costs very expensive.”

“It has been a tough week for those short dollars,” the bank adds.

HSBC’s David Bloom says he expects the euro to sink to $1.15.

Cyclical drivers are becoming dominant again, pointing to dollar strength as the Fed tightens and others hesitate.

0 comments:

Publicar un comentario