The economic damage from a trade war

Economists are taught trade wars are almost always damaging. The question for investors is: how damaging?

Gavyn Davies

A worker operates a furnace at a steel plant in Anhui province, China © Reuters

President Donald Trump’s threatened escalation of trade tariffs has moved to the centre of investor concerns. So far, the levies announced on steel and aluminium imports affect sectors so small that they will have almost no macro effect on US inflation, growth or employment. However, they could represent the thin edge of a very large wedge.

The focus now shifts to the Article 301 investigation into China’s practices in technology transfer and intellectual property. The White House is likely to take action on that soon. With hawks like Peter Navarro and Wilbur Ross in the ascendancy, and modifying influences fading after Gary Cohn’s resignation as chief economic adviser, the president may soon follow his instincts and announce tariffs on imports from China.

Although Navarro and Ross see tariffs as a means of forcing Beijing to abandon unfair distortionary practices, they could just as easily result in retaliatory trade controls, and even a global trade war.

That may seem improbable, but hostile rhetoric is building, and such an outcome can no longer be ignored.

This week, I will discuss the analytics of trade tariffs, and their macroeconomic impact on the country that imposes them. Next week, I will turn to the global effects of a full-scale trade war.

The bottom line: a global trade war, though still unlikely, would administer a negative shock to world GDP of perhaps 1-3 percentage points in the next few years. Although investors might see this as a manageable hit to growth, there is a downside to the distribution that could turn out to be much worse.

Economists are taught early on that trade wars are always damaging. Memories of the Smoot-Hawley Act in 1930 loom large. But what are the mechanisms involved?

When tariffs are imposed, the increase in the costs of cross-border trade obviously reduces global imports and exports, relative to output. This is what drives the welfare gains and losses in the longer term.

On this, there are some centuries-old results from international trade theory (see the leading textbook by Paul Krugman et al). In these partial equilibrium trade models, almost no one disputes that the decline in trade flows will reduce the scope for the law of comparative advantage to work, and for technology to flow easily across borders.

The reduction in these gains will hurt productivity and damage global welfare.

However, if a large country imposes a steel tariff, that might force Chinese producers to absorb part of the losses by cutting their prices to maintain a foothold in the American market.

In turn, the US might improve its terms of trade, and even see an overall welfare gain as the price of its steel imports declines. This favourable net outcome for the US is generally thought unlikely. Furthermore, smaller countries cannot achieve such offsetting gains, because they have to accept the global price. Their welfare is therefore unambiguously decreased.

Further cases that may justify tariffs are the protection of infant industries, and the correction of market distortions (eg export subsidies) imposed by other governments. However, most economists think it is better to attack these distortions head on, rather than indirectly through “offsetting” import tariffs.

Moving into macro-economics, many variables can change in response to tariffs, including the exchange rate, inflation, monetary policy and unemployment. This becomes much more complicated.

In old-fashioned Keynesian models (with fixed prices and exchange rates), a tariff is viewed as an expenditure-switching intervention, not necessarily an expenditure-reducing one.

US tariffs on steel imports could cause an increase in domestic production as foreign products are priced out of the American market. As a gross over-simplification, expenditure is, in the first instance, switched from China to the US, leaving global steel production unchanged. Mr Trump seems to believe all this.

But the effects on aggregate demand are complex. When the US imposes its tariff, China at first loses net income. In the US, steel producers might gain from greater output, but consumers, both households and other companies, lose. The government gains from tariff revenues, though these are probably distributed across the economy.

The initial effects on aggregate demand therefore depend on how all these gains and losses are translated into expenditure. Such redistributions are similar to the effects of an oil price increase that shifts income away from consumers and towards producers. If the losers cut demand immediately, while the winners spend their gains more slowly, global demand and output will fall in the short term. But none of this is obvious without much more empirical work.

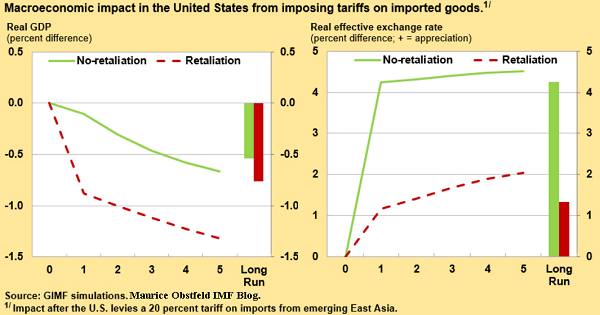

In his classic 1960s work, Robert Mundell argued that, in a world of flexible exchange rates, a new US import tariff will tend to improve the country’s trade balance, which will increase the dollar’s real exchange rate. This real exchange rate rise dominates the effect on the American economy, producing an overall decline in US output and employment, despite the (smaller) gains from the tariff’s expenditure-switching effect.

This remains the standard result. Maurice Obstfeld, the International Monetary Fund’s chief economist, wrote in 2016 that a 20 per cent US tariff on imports from East Asia, would (without retaliation) raise the dollar by 5 per cent, and cut US output by 0.6 per cent over five years.

In these models, Mr Trump’s trade agenda could back-fire on the US economy. Furthermore, all these results would be worse if we allow for temporary effects of tariffs on global supply chains, which could disrupt production, and the damage to confidence from uncertainty about trade policy.

These effects skew the possible outcome markedly towards the downside.

And there is the danger of retaliation from trading partners. Next time, I will try to quantify these serious global threats.

0 comments:

Publicar un comentario