High-Yield Bonds And The Rise In Rates

by: Downtown Investment Advisory

- The 10-year Treasury has soared from the 2.25% range to nearly 2.90% in the past months.

- Rises in rates are usually correlated with declines in bond prices; in the case of High-Yield bonds, the relationship is less certain.

- High-yields bonds have held up well with the recent rise in rates and increased market volatility.

- Investment grade bonds and treasuries have not fared so well.

- Rises in rates are usually correlated with declines in bond prices; in the case of High-Yield bonds, the relationship is less certain.

- High-yields bonds have held up well with the recent rise in rates and increased market volatility.

- Investment grade bonds and treasuries have not fared so well.

- This idea was discussed in more depth with members of my private investing community, High Yield Bond Investor.

Everyone knows that when interest rates rise, bonds go down in value, right? Many investors believe the same correlation applies equally to high yield bonds (so-called "junk bonds"), and warnings about this asset class are common. This article from CNBC describes how short interest in high yield ETFs have reached the highest level ever recorded, as "An environment of rising bond yields overall has dented the sector's popularity, and investors have been running for the doors."

After all, the 10-year Treasury and other interest rates have risen in recent weeks, so surely this means doom, and continues to mean a downturn is ahead for high yield. The chart below shows the rise in the 10-year Treasury from 2.25% range in October to 2.86%, a 60 b.p. rise, a sharp move up, mostly since the start of 2018.

10-Year Treasury Rate data by YCharts

10-Year Treasury Rate data by YCharts

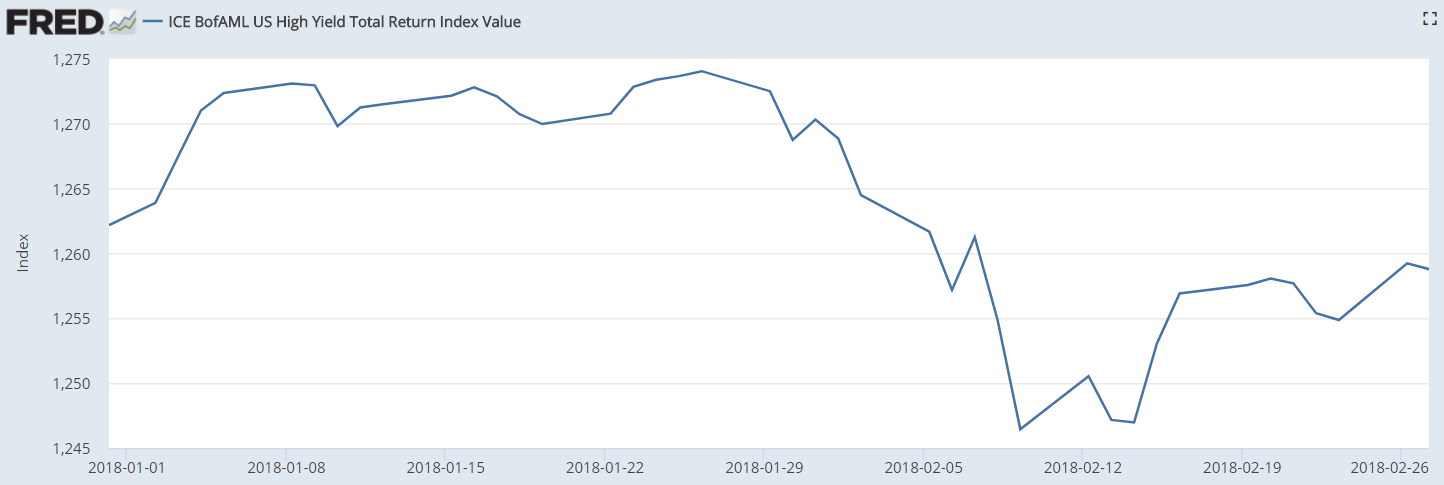

So how have high-yield bonds performed during this storm of rising rates since the beginning of the year? The Bank of America Merrill Lynch US High Yield Total Return Index, the best gauge of the high-yield market in my view (as a total return index, it incorporates interest earnings), shows a decline of only about a quarter of one percent. It is safe to call this "flat" performance.

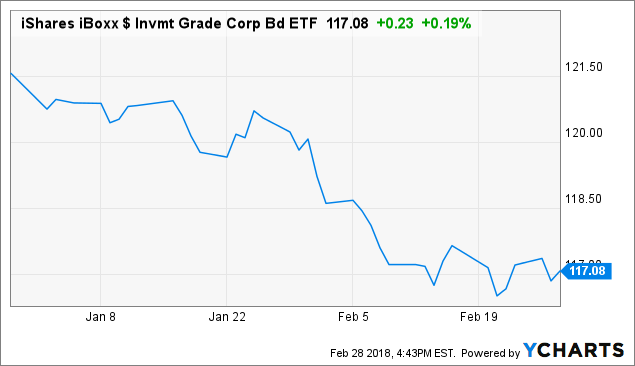

Not much of a move for high yield in the face of a 27% rise in the 10-year treasury rate. The real move down in bonds occurred in so-called Investment Grade bonds and Treasuries. The investment grade ETF, LQD, is shown below. These bonds are down 3.6% on a total return basis, a sharp move down for an asset class that only yields 3.7% - so a year's worth of income decline in only 2 months.

LQD data by YCharts

LQD data by YCharts

The 7-10 year Treasury bond ETF, IEF, has not fared much better, down 3.3% year to date, a decline of nearly 15 months of income in just two months.

IEF data by YCharts

IEF data by YCharts

Why the sharp divergence in performance between high yield and investment grade categories?

Because high yield is a credit risk sensitive asset class while investment grade and treasuries are interest rate risk sensitive. The same dynamics that lead to higher interest rates, such as a robust economy and inflationary pressure, are beneficial to credit risk and boost the performance of high-yield bonds. On the other hand, investment grade bonds already carry low credit risk, so they are priced according to prevailing market interest rates and are therefore far more sensitive to changes in rates.

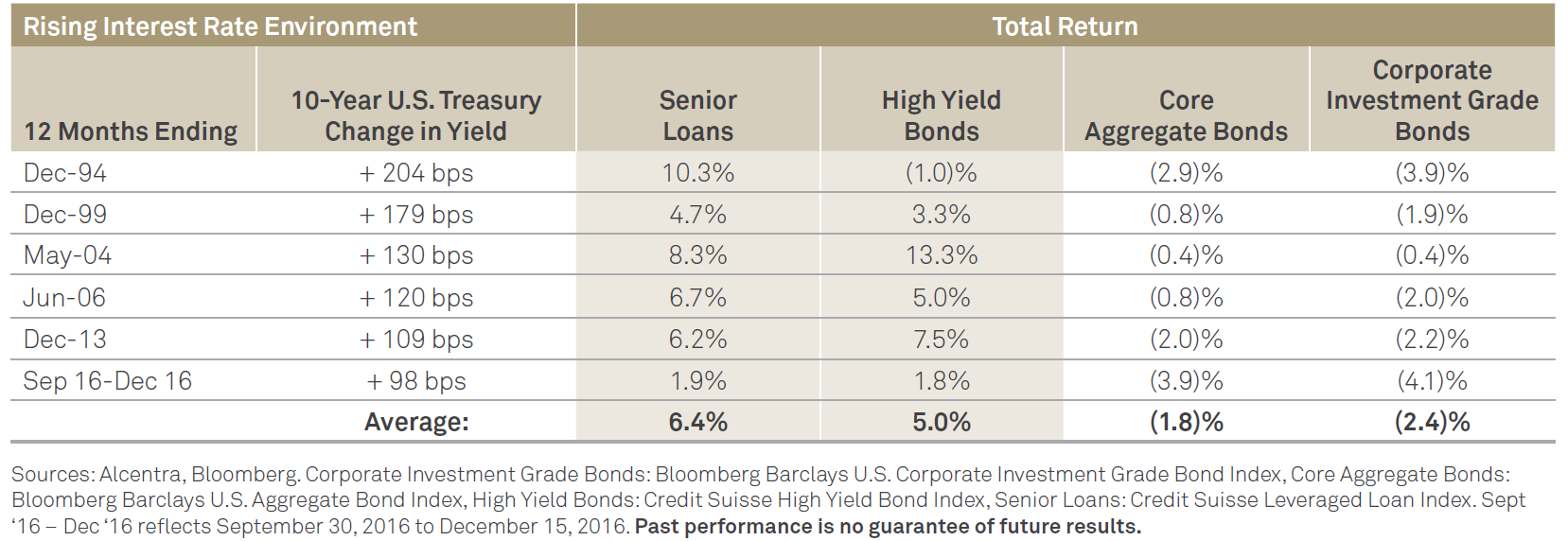

The chart below shows further evidence. On the left are the 12-month periods when the 10-year rate rose by 1% or more (0.98% in the Sep 16-Dec 16 period). As can be seen, Senior Loans, which are typically floating rate, and high-yield bonds performed just fine in these scenarios, while investment grade bonds always fell.

High-yield bonds typically react negatively in the short run to rising rates, like they did in the first two months of 2018, but stabilize and recover after that, usually quickly. My expectation for high-yield bonds for the remainder of 2018, barring any major stock market dip, is that once the 10-year treasury settles into a range, which it may have already at 2.8%-3.0%, bond prices will remain steady and interest earnings will kick in and generate 5%-7% returns for high yield for the remainder of 2018.

Fed fund increases are already well known and may likely be incorporated into today's 10-year Treasury rate. High-yield bonds will decline if the stock market corrects (again) or worse, as high-yield bonds are considered "risk" assets that typically fall when the stock market falls - but by far less (high-yield bonds are about 33%-40% less risky than stocks) with a far quicker recovery (as was the case in early-2000s and 2008 crashes).

The idea of shorting high yield, which I hear about from time to time, makes no sense to me. Just to break-even with a high-yield short, bond prices have to decline by about 6%, as the short seller has to cover the interest earned by the bonds. Factor in shorting costs, and the break-even "decline rate" is probably at least 7%-8%.

If an investor wants to short an asset class due to expectations of rising rates, shorting long-dated Treasuries or investment grade bonds makes far more sense. If an investor wants to short an asset class due to expectations of market tops or economic fears (or other shocks), shorting stocks makes far more sense - they will drop far more than high-yield bonds.

0 comments:

Publicar un comentario