Hanging Curve

by: Eric Parnell, CFA

- Economic growth is accelerating, inflation is increasing, and bond yields are on the rise!

- What if something entirely different is actually unfolding?

- What does the hanging curve tell us about what we should reasonably expect going forward?

- What if something entirely different is actually unfolding?

- What does the hanging curve tell us about what we should reasonably expect going forward?

- This idea was discussed in more depth with members of my private investing community, The Universal.

It is a message we keep hearing about in the mainstream financial media today. Bonds yields are on the rise. The optimists attribute the increase to a budding phase of accelerating economic growth and the higher inflation that comes with it. The more skeptical among us believe that an inevitable outbreak of higher inflation will induce the Fed to tighten more quickly than currently expected.

Despite their differing views, both leading narratives rely on the key underlying premise that inflation is going higher. But what about a third outcome? What if higher inflation never comes to pass? And what if this takes place at the same time that the economy sputters while the Fed is still raising rates?

What then?

Scoffs Of Derision

Dare raising the possibility of this third outcome in the mainstream financial media. I can hear now the haughty scoffs and see scornful glances of derision being cast upon the market heretic for even raising such a possibility. But here's the thing. Every single year since the calming of the financial crisis we have heard the same exact themes being uttered. Economic growth is accelerating! Higher inflation is right around the corner! Yet every single year to date through today, such an outcome has never come to pass. So forgive my cynicism, but given that this narrative has been largely wrong the last eight years and counting, why exactly is it absurd to think it might happen for a ninth time in a row? Just sayin'.

But 2018 is different! We are now in a phase of synchronized global economic growth. And we just had the passage of a massive tax cut program that is propelling corporate earnings projections to new all-time highs. It is only a matter of time now before corporations pass along this bounty to its workers in the form of higher wages that will result in too much money chasing too few goods. Hence, bond (BND) yields are set to go flying to the sky.

OK. Maybe. But how much has this recent perception of synchronized global growth been fueled by the fact that the European Central Bank and the Bank of Japan has been buying virtually every asset in sight at the same time that the People's Bank of China resumed expanding its balance sheet after a two-year hiatus? Adding more than $3 trillion to the collective global major central bank balance sheet can do wonders to foster the perception, and perhaps the illusion of synchronized global growth. And now all of this stimulus is in the process of being slowly drawn away.

As for the corporate tax cuts, the boost to the corporate earnings outlook has been impressive indeed. But will companies actually pass along these higher earnings to its employees not in the form of one-time bonuses but instead in repeatable wage and salary increases? Or will these higher earnings instead get channeled to shareholders in the form of increased buybacks and dividends? If history is any guide from more than a decade ago when corporations last received a major tax break to fill their coffers, we still have good reason to believe it may be more of the latter until proven otherwise when core inflation gauges remained relatively subdued as well.

Final mention: a global trade war is not good for synchronized global growth. Nor is it good for corporate earnings. We'll see how this all plays out.

So can I see the potential that the ninth time will finally be the charm in 2018 for the long anticipated breakout in economic growth and higher inflation? Absolutely. But given that such predictions have been flat wrong eight years prior, it is prudent to require more than just an easy narrative to conclude that such a sunny outcome is inevitable this time around.

Hanging Curve

It is in assessing the data to find confirmation of this higher economic growth, higher inflation, higher bond yield narrative where things start to break down.

To begin with, forecasted economic growth remains positive, but hardly robust or anything notably better than what we've already been experiencing in recent years. But it is possible that despite recent downward forecast revisions that these projections will prove gross underestimations.

What of the inflation data? The latest core consumer price index reading for January 2018 came in at 1.85% on a year-over-year percentage change basis, which is up from the 1.69% reading in August 2017. But this number is still much lower than the 2.25% reading from this same time a year ago. And at below 2%, it has not even risen yet to the Fed's target level much less climbed to anything that would be considered heralding a major inflation outbreak. But the CPI is a lagging indicator, so let's see what reading for February holds that comes out next Tuesday to see if we're getting any traction. If the latest reading on wages from Friday's employment report is any guide, next week's report may not be lighting any fires, but we'll see.

So what then do the leading indicators tell us? Bond (TLT) yields certainly have risen in recent months. Isn't this telling us that inflationary pressures are set to take hold? Let's take a closer look. And in order to do so, let's take a walk through recent history to put where bond yields are today into better context.

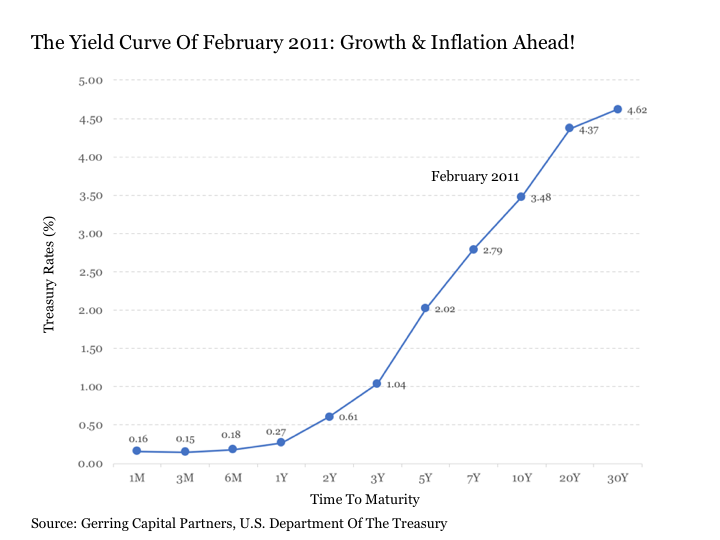

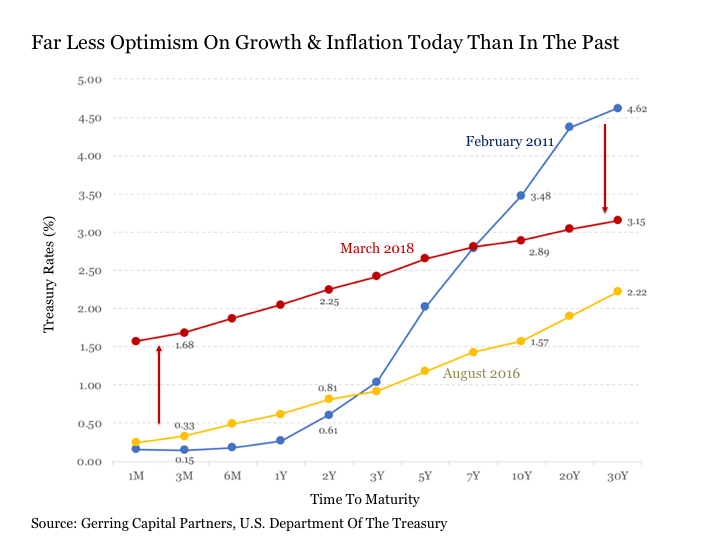

We will begin our journey back in time to February 2011. If ever there was a moment more than any other during the post-crisis period where the market was signaling to its investors that a phase of sustained economic growth and higher inflation was poised to break out, it was February 1, 2011. For it was on this date that the U.S. Treasury curve was at its steepest slope throughout the entirety of the post-crisis period to date. Why is this significant? Because a steep yield curve signals optimism among investors about the economic outlook due to the fact that they are requiring a more significant premium to tie up their capital in an increasingly longer duration bond instrument and forgoing the potential to participate in higher growth opportunities from the likes of equities while at the same time exposing themselves to the greater risk that inflation will erode the real value of the coupon payments they are set to receive in the future.

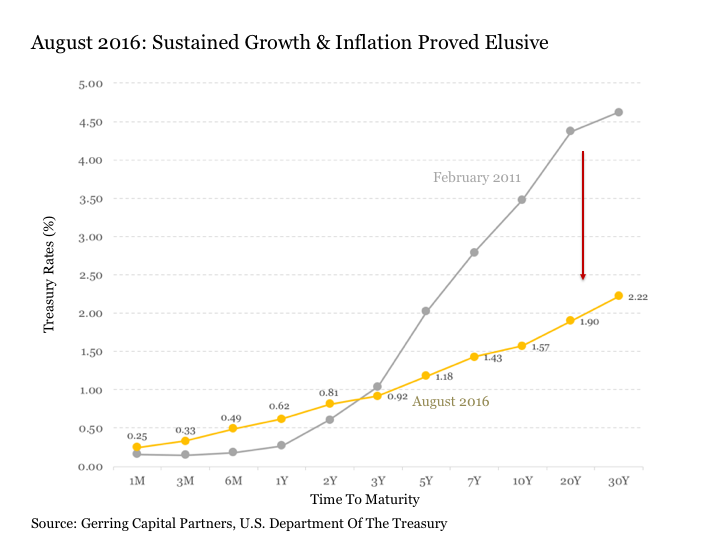

Thus, what has taken place in the seven years since has been a slow deterioration of the optimism implied during this still early phase of the post-crisis period. Put simply, the anticipated breakout in economic growth never really materialized. Neither did the sustainably higher inflation expected by so many despite the fact that central banks were relentlessly pumping monetary stimulus into the financial system (why higher inflation is going to break out now that central banks are moving to take this stimulus away today is a topic for another debate). This evolution over the next five years brought us to the following yield curve by contrast in August 2016.

While the short end of the curve remained effectively pinned to the floor, the long end of the curve had essentially collapsed. The fact that investors had become much more willing to accept a meaningfully smaller maturity risk premium for moving further out the yield curve suggested that investors had become vastly more skeptical about the prospects for economic growth and higher inflation going forward. This was confirmed by the fact that the five-year breakeven inflation rate, which indicates the rate of inflation investors are anticipating over the next five years, had fallen from as high as 2.64% in 2011 to as low as 1.21% in 2016, which of course is well below the Fed's target inflation rate of 2%.

Of course, much has changed in regard to the economic, corporate earnings, and inflation outlook since the summer of 2016. What then has the yield curve telling us about our prospects going forward?

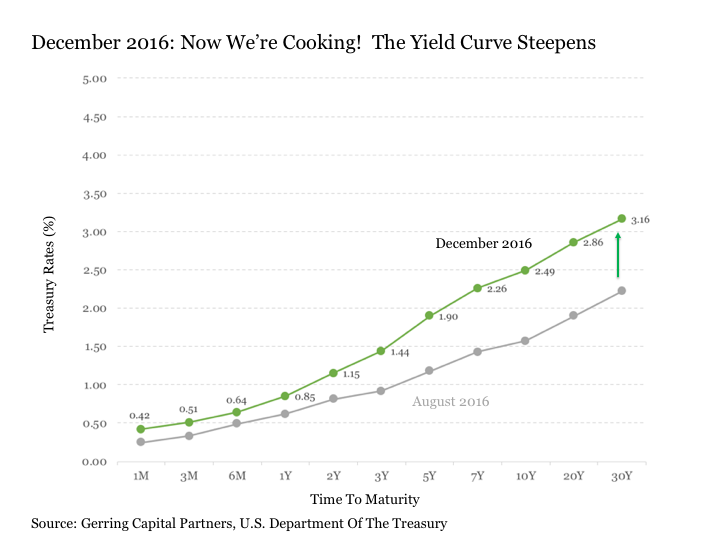

The first major event was the 2016 U.S. election. Capital markets initially cheered the outcome, and the yield curve began notably steepening.

While the shift was nowhere close to the slope seen in February 2011, it was a strong push in the right direction for the economic and inflation outlook.

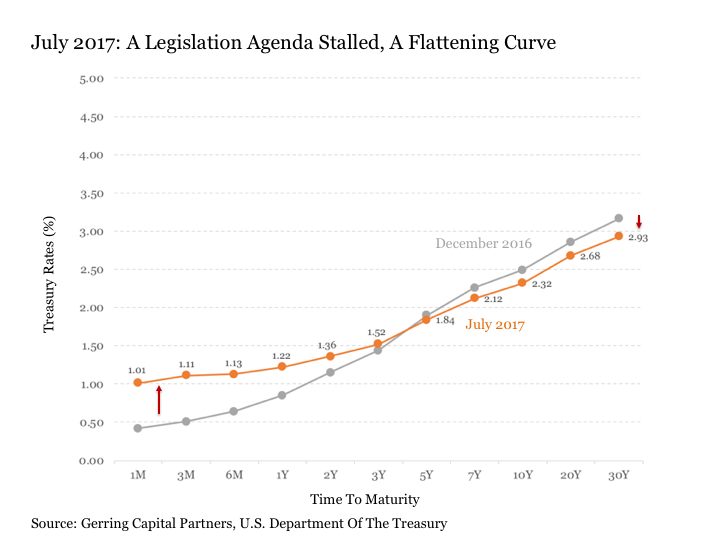

But then things stalled. Much of the legislative agenda that the market initially priced in to effectively take place on Inauguration Day ended up getting stuck in the mud. While regulations were relaxed across many segments of the economy, infrastructure was put on the back burner, the repeal and replacement of the Affordable Care Act was repeatedly delayed before finally fizzling out, and the fate of tax cuts much less tax reform was looking increasingly uncertain. And all of this was taking place at a time when the Fed had finally cast off its fear and started to move more assertively in raising interest rates, thus lifting short-term interest rates off of the floor. The result was a notable drop in optimism in the economic and inflation outlook as implied by the yield curve.

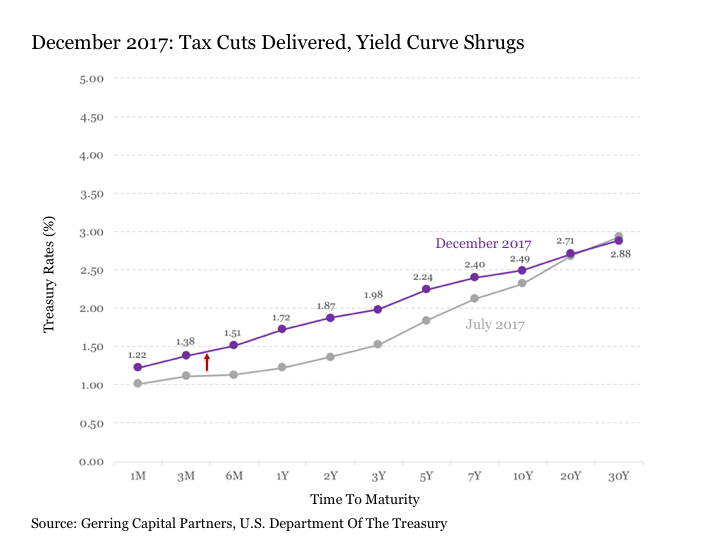

But then the legislative agenda finally started to turn. The notion of tax reform was quietly set aside as the focus turned to landing some measurable tax cuts. Leading among them were major corporate tax cuts including measures to encourage the repatriation of profits stashed overseas. After months of wrangling and debate, the Congress completed a tax cut package that was signed into law by the White House by late December 2017. While economic growth and corporate earnings projections were immediately revised higher, the yield curve remains notably subdued. If anything, it had notably flattened with the long end remaining effectively unchanged as the Fed continued to push forward in lifting the short end of the curve. In short, it was signaling even greater consternation about the outlook, not optimism, as the yield curve had reached its flattest levels to date in the post-crisis period.

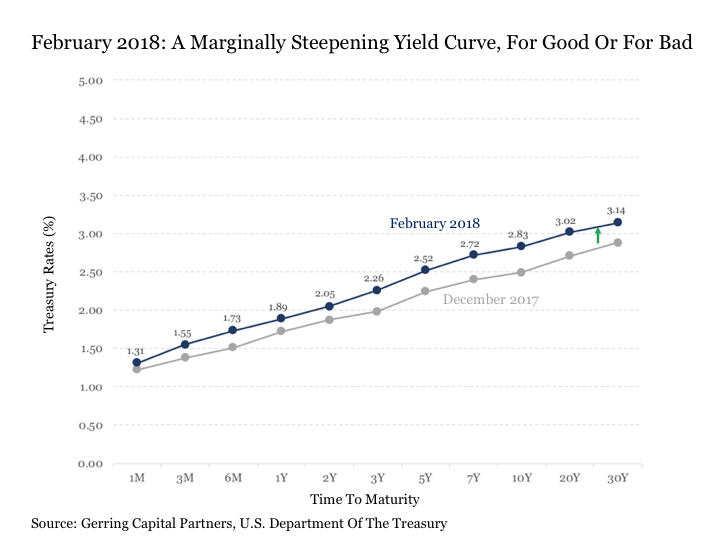

Of course, the calendar flipped to 2018 and it seemed that the mood had suddenly changed.

Stocks (SPY) stormed out of the gates in the new calendar year to the upside. And they were followed higher by a surge in long-term rates. While certainly nothing close to the magnitude of what existed in February 2011, it was a notable move in its own right that exceeded the pace of implied further tightening by the Fed. All of this was supporting the more optimistic narrative for a few weeks in January, but then concerns supposedly suddenly erupted about the threat of higher inflation ruining the party, sending stocks careening to the downside with a notable spike in volatility in early February (never mind the fact that the inflation report came in hot a week after this quick and dirty stock market mess - let's stick with the narrative for now that this was an "inflation concern" induced issue and not something else entirely). Nonetheless, the yield curve was still moving, albeit marginally, in the right direction by early February.

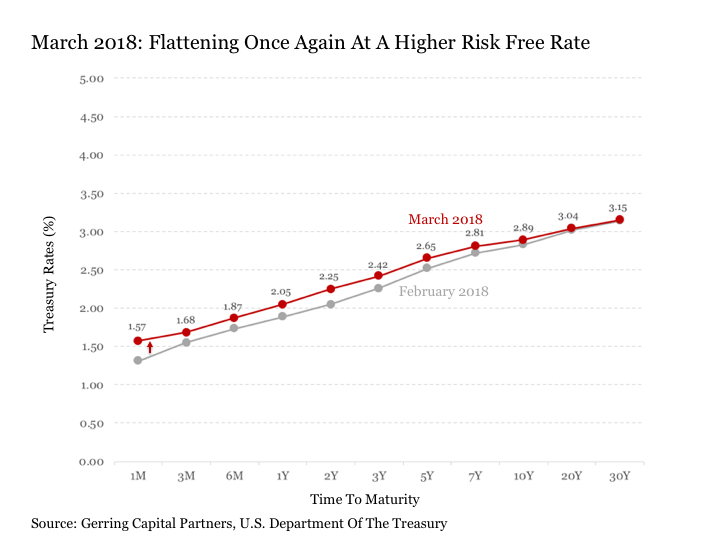

But what have we seen since through today in mid March? The yield curve has been steadily flattening once again. In the process, it is quickly descending to the flattest post-crisis levels set at the very end of 2017 across the curve. Put simply, while the stock market has stabilized and the ability to melt higher no matter how bad the news on any given trading day has returned, the concerns implied by the flattening yield curve are persisting.

Putting this altogether we have the following three points of contrast from February 2011, August 2016, and today.

Put simply, the long end of the yield curve is much lower versus where it was seven years ago, and the short end of the yield curve is much higher today versus where it was as recently as 18 months ago in the summer of 2016. This has resulted in a yield curve that is about as flat as it has been throughout the post-crisis period despite all of the continued talk of economic growth optimism and higher inflation.

The Key Takeaways

What are the key takeaways from this walk through yield curve's past?

First, the yield curve implied optimism about the growth and inflation outcome is nothing like it was back in February 2011. Sustained economic growth and higher inflation didn't materialize then, and the current yield curve suggests we should maintain a healthy degree of skepticism that it is going to materialize going forward from today. For it is in fact telling an entirely different story about the future outlook. Sure, stock prices may rise in the meantime, but as evidenced over the past decade, higher stock prices are not economic growth and they are not higher inflation.

Second, not only has the yield curve flattened markedly since August 2016, but it has done so with an overall shift in the curve itself to a level that is several percentage points higher today versus where it was the summer before last. In short, the risk-free rate is much higher today than it was less than two years ago when stocks were surging their way back from their last near accident from the summer of 2015 through the winter of 2016. And the risk-free rate as implied by the shorter end of the yield curve is set to rise measurably still in the coming year with the Fed expected to raise interest rates by a quarter point as many as three times on average in 2018 with some estimates going as high as five hikes this year. As short-term rates continue higher, this will apply increased pressure on stock prices given their historically high valuations, as increasingly pressure gets applied to the equity risk premium required by investors to take on the added risk of owning stocks. Moreover, if the long end of the curve continues to move slowly in following the short end higher in the coming months as the Fed continues to raise, it only brings the specter of the next economic recession all the closer, an outcome of which is very much the opposite of economic growth and higher inflation.

Lastly, the movements in the yield curve particularly over the past year should highlight why investors much exercise caution and do their own homework before reacting too swiftly on any news about economic growth, higher inflation, higher interest rates and steepening/flattening yield curves.

If one were to listen only to the news, they might perceive that these indicators are flying all over the place. But the reality remains that while such moves may seem dramatic in the isolation of a handful of trading days, they have still been relatively minor in a broader historical context. Put more simply, avoid being reactive and maintain your discipline amid any seemingly major market moves at any given point in time.

The yield curve may ultimately find its mojo and start sustainably steepening as the elusive hopes and dreams of economic growth and higher inflation are finally realized. But to date, the latter remains unconfirmed while the former continues to foretell an entirely different tale as evidenced by the hanging curve.

Be careful out there in today's markets. And be prepared for the outcomes that the broader market may least expect.

0 comments:

Publicar un comentario