Kill the Quants

In the past few days we have heard endless

explanations for the market’s big “Oops!” and the return of volatility. The

commentary has centered on the Fed and its sister central banks as they begin

to batten down the hatches on inflation and trim their balance sheets

(prematurely, in my view).

In the midst of all the hoopla – and for a long time

before the recent Day of Reckoning – my good friend Doug Kass has been

something of a voice shouting at us from the wildnerness, with the resounding

refrain “Kill the quants before they kill our markets!” Here’s Doug,

explaining himself:

I believe the precipitous

market drop in the last week has little to do with the projected course of

interest rates or, for that matter, fundamentals. It likely was a function of

the distorted, dangerous world of new investment products and strategies….

[T]he proliferation of short vol, volatility trending and risk parity

strategies when combined with an explosion of leveraged ETFs and ETNs – many of

which were derivatives of derivatives and had no business existing except to

please gamblers – had altered the market structure…

There is an interesting thing about ETNs. These are

exchange-traded notes, and while I don’t want to get to arcane on you, a key

feature of them is that there has to be a bank or a guarantor on the note. Even

though we’ve had at least two shortfall ETNs literally blow up and go to zero,

the investors in those funds are going to get “something.” If you put in your

withdrawal request while there was still a price, there is an extraordinarily

good case that you are due your money.

And of course, the ETN fund doesn’t have any money.

But the bank that guaranteed the ETN is on the hook. One of the ETNs was

evidently backed by Credit Suisse. Credit Suisse made an announcement before

the market opened yesterday morning that they had 100% of their liabilities

hedged out in the marketplace. Of course, they didn’t say hedged out to whom,

and that will make us all wonder about counterparty risk; but we won’t have

answers on that for a long time, and while a significant amount of money is

involved, it is not life-threatening to a bank the size of Credit Suisse. More

like annoying than life-threatening.

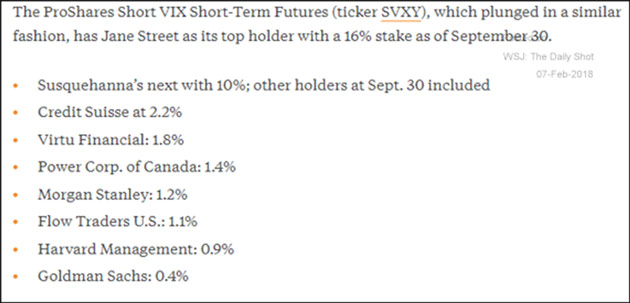

Just for grins and giggles, I submit this list of the

largest shareholders in SVXY, one of the short-vol VIX funds. Interesting to

see Harvard Management in there. Really? Harvard is reaching for yield?

Source: WSJ/The Daily Shot

I was probably making two calls a day to my go-to guys

in the high-yield market, to see how high-yield bonds were responding. I think

ultimately the collapse in high-yield will precipitate “the Big One.” You just

can’t understand how much in high-yield bonds has been sold, how poorly the

covenants are managed, and how badly investors are going to get screwed.

You watched this last week as the VIX fell out of bed.

I am telling you that what is going to happen in the high-yield market is going

to be more – much more – of the same. It’s going to seemingly fall out

overnight. The bids are going to disappear, and high-yield bonds are going to

be sold to what are essentially distressed-debt funds at distressed-debt

prices.

Further, as we get into late 2018 and then into 2019

(not to mention 2020), the amount of high-yield debt that has to be “rolled

over” becomes significant. And it is obviously going to have to be rolled over

at higher interest rates. There will be some companies that will be able to

handle those rates, and there are some companies that are simply way out over

the tips of their skis, trying to schussboom down a double black diamond slope,

and the outcome is going to closely resemble one of those “agony of defeat”

moments from the old Wide

World of Sports TV show. We’re talking some spectacular face

plants. You do not want to be involved, unless from the short side, when that

happens.

The Fed is inadvertently increasing the risk for these

funds by raising rates. Now, frankly, I don’t think the Fed should be paying

any attention to how much pain they are causing the high-yield bond market when

they make decisions on interest rates. Theoretically, you should be a big boy

to be playing in that market. Except that there are a lot of mutual and ETF

funds that allow very small mom-and-pop operations to reach for yield just like

Harvard Management. That was an annoying moment for Harvard, but it’s a

rounding error. If guys like me weren’t calling them out on it, nobody would

even notice. But I’m not even on their Christmas card list, so….

But let’s get back to Uncle Doug Kass. This week’s OTB

is a composite of some of the recent letters he has done for Real Money. I

thank him for giving me permission to republish.

By the way, did anybody else notice that the

high-frequency traders who are always bragging about how they provide liquidity

to the markets simply disappeared as the markets fell through the floor? Where

was this liquidity they were talking about? They have the inordinate privilege

of front-running everybody’s money, taking basis points from every trade, on

the theory that they are providing liquidity. And they simply withdrew it via

their completely quantitatively computer-controlled system. High-frequency

trading should be reined in, and any bid or ask prices submitted by computers

should be made the last for at least 0.5 seconds. Slow enough for a young

trader with good twitch speed to hit the button on their own computer and

execute.

That would of course mean that volumes on the NYSE

drop significantly, but that’s volume we don’t need; it’s meaningless. It’s not

there when you need it – witness this past week.

So I’ll get off my personal rant and turn you over to

Uncle Doug. You have a great week. (On a personal note, the cold and nasty

weather we are experiencing in Dallas makes me love high-rise living and having

my office and gym inside the building!)

Your paying attention to interest rates analyst,

John Mauldin, Editor

Once Again: “Kill the Quants (and the Levered ETFs and ETNs) Before They Kill Our Markets”

By Douglas A. Kass, Seabreeze Partners Management Inc.

* Friday was likely the day the short volatility trade

died.

* A massive regulatory overhaul is needed to counter

the destabilizing influence of strategies and exchange traded products that

have overwhelmed our markets.

For years I have warned about the explosion in

popularity (and listings) of ETFs (which now outnumber the number of publicly

traded companies) and ETNs – in an oft repeated column entitled... “Kill The

Quants Before They Kill Our Markets.” In pointing out the risks of the “new”

versions of strategies purporting to be able to control risk (on the fly), mine

was a voice in the wilderness, ignored by the majority of market participants

who were enjoying the bullish fruits and impact of these newfangled strategies.

Indeed it took a bit over six years for XIV (an inverse VIX product, it’s VIX

spelled backwards!) to rise from $10 to $144 but only one day for the product’s

price to implode to $0. As blogger Quoth The Raven tweeted this morning: “Six

years of picking up pennies in front of a bulldozer wiped away in one session.”

Nomura’s Charles McElligott (who I have quoted extensively over the last year)

was another voice:

The “grey swan” we all have

spoken about for years – that

being the absurd “tail wagging the dog” potential of VIX ETN market structure

(inverse and leveraged products) AND the massive growth in “negative convexity”

/ “vol target” / “vol rebalancing” strategies to either generate extra income

or “systematically allocate risk” (looks good in the prospectus, right?!) –

finally “broke” the volatility market, and has now bled-through to the

“underlying” spot equities market...as

the short vol trade went “lights out.”

The ETNs are the “patient zero”

of this current market meltdown. It

is estimated that there was anywhere from ~$125mm to $200mm of vega / VIX futs

to BUY on the close from the two main “short VIX” ETNs that rebalance daily

(XIV and SVXY). As S&P traded -50 handles AFTER the cash

close from 4:00pm to 4:15pm into the market’s anticipation of the massive

rebalancing of volatility (buy to cover) on the close, XIV then saw a delayed

and terrifying ~-87

PERCENT move after the close, as some who owned XIV puts as crash protection

sniffed this potential and speculated liquidation from the ETN, which is set

per a rules-based system to buy back short vega after an 80% “crash

trigger”(which again isn’t a certainty because they use a blend of 1st and 2nd

month). The asset pool nonetheless was seemingly / largely

wiped-out and the note is guaranteed to “pay out” to their shareholders as set

per their prospectus. It

is likely that this thing has indeed been “triggered” and will be forced to

liquidate. SVXY doesn’t have the firm 80% “trigger” but too is seeing its NAV

“wiped out” and is trading ~-80% post-close as well.

The issue NOW is the pile-on

going-forward across assets, as the systematic “short vol” community’s models

are now completely toast, and they too will be forced to cover remaining “short

vol” positions that didn’t trade today-i.e. BE PREPARED FOR A MAJOR VIX

FOLLOW-THROUGH TOMORROW.

VaR-based models need to be

reset across all asset-class strategies, forcing further de-risking over the

coming days and potentially weeks, as heads of funds and heads of risk try to

figure out how much their models are forcing them to “gross-down.” Shorter-term

vol target / vol allocation strategies (think CTAs) and longer-term models like

risk-parity and too will reset and “rebalance” their risk (lower) as realized

vols are re-priced. Structured products, annuities and other vehicles with

built-in protection? Also purging exposure on the vol reset. Finally, it also

shouldn’t be lost on the popularity of “short VIX” trades in the retail

community, and the “butterfly flapping its wings” relationship to the recent

melt-down in the crypto-currency space.

Until Friday, when we experienced a “come to Jesus”

moment for structured products and relational quant strategies (e.g. risk

parity and short vol ), few listened to our concerns of a possible Short

Volatility Armageddon caused by a rapidly changing and dangerous market structure in which VIX products multiplied like

weeds. I believe the precipitous market drop in the last week has little to do

with the projected course of interest rates or, for that matter, fundamentals.

It likely was a function of the distorted, dangerous world of new investment

products and strategies. As discussed below (and above), the proliferation of

short vol, volatility trending and risk parity strategies when combined with an

explosion of leveraged ETFs and ETNs – many of which were derivatives of

derivatives and had no business existing except to please gamblers – had

altered the market structure in as extreme a manner as Portfolio Insurance did

30-1/2 years ago (which led to the October, 1987, crash). Back then, Portfolio

Insurance proved to be a bridge too far that added a dynamic component that

would attempt to increase the hedge as the market was declining but which (1)

served to actually increase

the downward volatility of the market and (2) whose very ability to be executed

depended on market liquidity being available but which their strategy of

selling more

at lower prices (as the market declined) would quickly exhaust and then destroy

that liquidity very, very quickly. The SEC was asleep then (in 1987) and the

SEC is asleep today. The kennel of VIX related products (that have become the

tail that wags the market’s dog – should be closed down, post haste. Market

participants (and regulators) have little understanding of the technical nature

of these products/strategies or the domino and ripple effect. Many of these ETF

products and options should be suspended and outlawed and the issuers should be

held to account. It’s bigger than bitcoin – and bitcoin is a dumb idea!

Unfortunately I cannot see with clarity how the genie of quant strategies, ETFs

and ETNs are taken out of the (market) bubble – particularly with the inertia

of the regulatory authorities like the SEC. Last night I sat next to the New York Times’ Jim Stewart

at dinner – with my iPhone between us, spewing out the news that the market

disequilibrium had been upset like nothing I had seen in decades. Jim and I

chatted while watching (laser focused) the overnight market disorder – at its

nadir, DJIA futures fall by -1200, S&P futures nearly -125 and Nasdaq

futures collapsing by over -220 against fair market value. I expanded further

on some of continued concerns regarding the market’s structural problems in

yesterday’s opening missive; and in my last post on Monday evening,

“Revenge of the Machines”:

“Surprise #9: In 2018, the

global volatility bubble bursts in a spectacular fashion, with stocks falling

by 15% in one session.”

– Kass Diary, A Market That Continues to Underprice Risk

I spent the better part of 2017 and all of 2018

warning about the possibility of another flash crash – caused by a dangerous

shift in the market structure which was led by leveraged actors who conducted

short volatility and risk parity strategies – who are agnostic to balance

sheets, income statements and intrinsic value. (Read my 15 Surprises for 2018 and this morning’s lengthy discussion

in my opening missive.)

That shift in structure coupled with the popularity of

passive strategies (ETFs) continued to have a pronounced impact on the markets,

pushing volatility to (a hat size) of record lows and stocks to record highs –

arguably, creating something of a “buyers’ panic” in January as late-coming

retail investors (suffering from “FOMO”) poured a record $50 billion into the coffers

of domestic equity funds. This buyers’ panic occurred in a backdrop of less

liquidity and lower market volume – further exacerbating the late 2017/January

gains. That buying forced RSIs towards unprecedented levels as investor

sentiment surveys made multi-decade bullish highs. As stocks climbed ever

higher, skepticism and doubt were nearly abandoned and assessment of risk vs.

reward took a back seat to bullishness.

The constant shorting of volatility, I warned, could

resemble having the role of portfolio insurance, which caused a rapid drop in

stock prices in October, 1987. I even called short vol having the potential

label of Portfolio Insurance (Part Deux). The S&P Index (adjusted for the

after-hours S&P futures weakness of about another 30-40 handles) is now

almost 285 handles below the level of only a few days ago. This has served,

according to my calculus, to move the downside risk relative to upside reward

from 4:1 (negative) to less than 2:1 (negative) – using an expected trading

range for the S&P Index in 2018 of between 2200 and 2800. I am of the

belief that today’s action was forced and, in a sense, a mechanically inspired

decline (remember the S&P Index was actually higher at one point in this

session). Oddly missing in the media discussion today has been the interest

rate reaction – a flight to safety that took the ten-year US note down by

nearly fifteen basis points (to 2.70%)! This move may be interpreted as

confirmation that the market’s precipitous drop today was structural and not

necessarily rate related. That is not to say that we will necessarily have a

“V” type reaction. I dont know ... and anyone who expresses certainty (as many have)

should be avoided and ignored. We must wait and let the derisking of short vol

and risk parity work itself out and run its course. The magnitude of the

short-term market decline has likely contributed to margin calls and retail

redemptions which will further complicate the timing of a recovery. I

aggressively traded a lot of Spyders (SPY)

today and I am currently paying $260.20 in after-hours – based on a view that

this is a short term opportunity (but solely for a trade). And I covered a

number of shorts (at what I believe to be favorable prices) – particularly in

financials – during the quick whoosh lower in the late afternoon. I took a

number of shorts off of my Best Ideas List as the risk/reward ratios have

abruptly changed – with many stocks down by 10% to 20% from a week ago. Values

will likely be created in the days and weeks ahead. But in order to capitalize

on those opportunities one has to be almost emotionless – not an easy task in a

downturn like we have experienced in the last few days. Let me end a hectic day

with a column just written by JPMorgan’s global quant, Marko Kolanovic,

entitled “Flash Crash, Flows and Investment Opportunities”:

In last week’s note, we noted

that volatility, at the time, was not sufficient to trigger systematic strategy

de-risking. On Friday, the market dropped ~2% on a day when bonds were down

~40bps. The move on Friday was helped by market makers’ hedging of option

positions (as gamma positions turned from long to short midday). Friday’s move,

on its own, was significant as it pushed realized volatility higher, which is a

signal for many volatility targeting strategies to de-risk. Anecdotally, broad

knowledge about the risk of systematic selling kept many investors fearful and

waiting on the sidelines (both in equity and volatility markets). Midday today,

short-term momentum turned negative (1M S&P 500 price return), resulting in

selling from trend-following strategies. Further outflows resulted from index

option gamma hedging, covering of short volatility trades, and volatility

targeting strategies. These technical flows, in the absence of fundamental

buyers, resulted in a flash crash at ~3:10pm today. At one point, the Dow was

down more than 6%, and later partially recovered. After-hours, the VIX reached

38 and futures more than doubled – it is not clear at this point how this will

reflect on various short volatility products (e.g., some volatility ETPs traded

down over 50% after hours).

Today’s large increase of

market volatility will clearly contribute to further outflows from systematic

strategies in the days ahead (volatility targeting, risk parity, CTAs, short

volatility). The total amount of these outflows may add to ~$100bn, as things

stand. However, we want to point out the massive divergence between strong

market fundamentals and equity price action over the past few days. The large

market decline over the past few days will likely draw fundamental investors

and even trigger pension fund rebalances (those that rebalance on weight

thresholds). We also want to highlight a strong probability of policy makers

stepping in to calm the market.

Rapid sell-offs, such as the

one today, can also be followed by market bouncebacks as liquidity gets

exhausted by programmatic selling. With next year P/E on the S&P 500 now

below 16, further positive impacts of tax reform and stabilization of bond

yields (e.g., note the current record level of CFTC bond short positions), we

think that the ongoing market sell-off ultimately presents a buying

opportunity.

0 comments:

Publicar un comentario