Flattening yield curve points to calm about US budget deficit

But those hoping for a great acceleration in the economy will be disappointed

Matthew C. Klein

The famed “bond vigilantes” are clearly unconcerned about the government’s ability to fund its debt issuance. The US government’s real long-term borrowing costs are lower now than they were at the beginning of 2016.

That is not what you would expect if traders were exercised by the prospect of large future budget deficits, nor is it what you would expect if traders were optimistic about the growth Outlook.

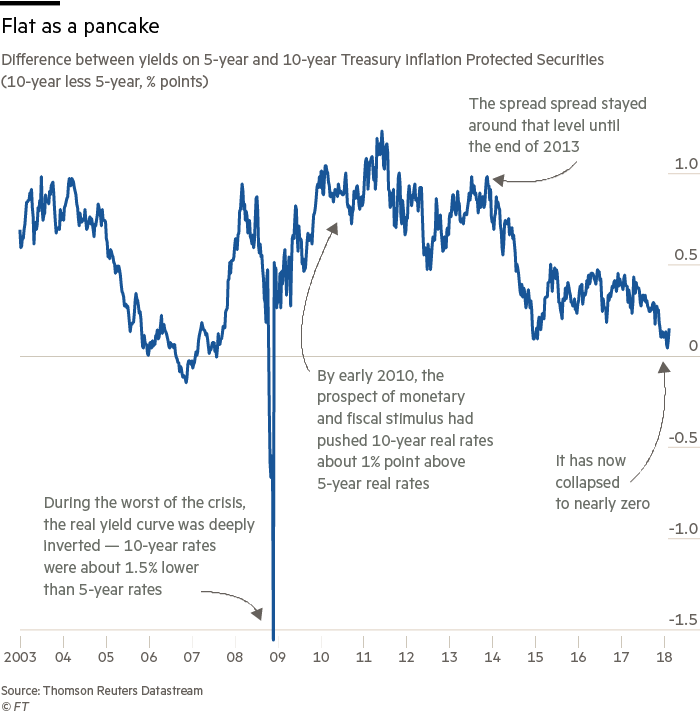

There is also useful information in the absolute difference between shorter and longer-term real yields. If 10-year yields are higher than five-year yields, for example, then that probably means traders expect some combination of faster growth and tighter monetary policy in the future relative to today.

During the worst of the crisis, the real yield curve was deeply inverted — real 10-year rates were about 1.5 percentage points lower than real 5-year rates. By early 2010, the prospect of monetary and fiscal stimulus had pushed 10-year real rates about 1 percentage point above 5-year real rates. This spread stayed around that level until the end of 2013. In the past year it has collapsed to zero.

This curve flattening does not necessarily mean recession is imminent, but it also suggests the future will not be much different from the way things are right now. Market pricing implies those hoping for a great acceleration will be disappointed. The better future promised in the past has already arrived.

0 comments:

Publicar un comentario