Boo!

The markets deliver a shock to complacent investors

Out of a clear blue economic sky, volatility returns and may linger

EVERY good horror-film director knows the secret of the “jump scare”. Just when the hero or heroine feels safe, the monster appears from nowhere to startle them. The latest stockmarket shock could have been directed by Alfred Hitchcock. The sharp falls that took place on February 2nd and 5th followed a long period where the only direction for share prices appeared to be upwards.

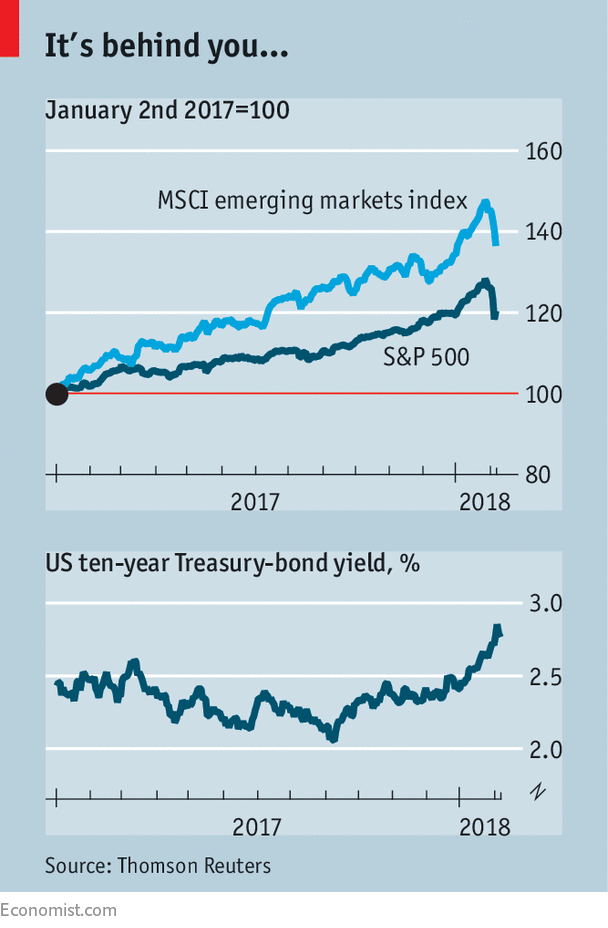

In fact the American market had risen so far, so fast that the decline only took share prices back to where they were at the start of the year (see chart). And although a 1,175-point fall in the Dow Jones Industrial Average on February 5th was the biggest ever in absolute terms, it was still smallish beer in proportionate terms, at just 4.6%. The 508-point fall in the Dow in October 1987 knocked nearly 23% off the market.

Still, surprise rippled round the world. Between January 29th and early trading on February 7th, the MSCI Emerging Markets Index dropped by 7.5%. The FTSE 100 index fell by 8.2% from its record high, set in January. A late recovery on February 6th, in which the Dow rebounded by 2.3% (or 567 points), restored some calm.

What explains the sudden turmoil? Perhaps investors had been used to good news for so long that they had become complacent. In a recent survey investors reported their highest exposure to equities in two years and their lowest holdings of cash in five. Another sign of potential complacency was the unwillingness of investors to pay for insurance against a market decline, something that showed up in the volatility, or Vix, index. Funds that bet on the continuation of low volatility lost heavily (see article).

The wobble may also reflect a decision by investors to rethink the economic and financial outlook.

Ever since 2009 central banks have been highly supportive of financial markets through low interest rates and quantitative easing (bond purchases with newly created money). There was much talk of an era of “secular stagnation”, in which growth, inflation and interest rates would stay permanently low.

But the Federal Reserve and the Bank of England are now pushing up interest rates, and the European Central Bank is cutting its bond purchases. Future central-bank policy seems much less certain. A pickup in global economic growth may naturally lead to fears of higher inflation.

The World Bank warned last month that financial markets could be vulnerable on this front.

Bond yields have been moving higher since the autumn; the yield on the ten-year Treasury bond, 2.05% on September 8th, reached 2.84% on February 2nd. On that day American employment numbers were released, showing that the annual rate of wage growth had climbed to 2.9%. That suggested inflation may be about to move higher. Furthermore, the recent tax-cutting package means that the federal deficit may be over $1trn in the year ending September 2019, according to the Committee for a Responsible Federal Budget, a bipartisan group. Making such a large amount of bonds attractive to buyers might require higher yields.

Higher bond yields are a challenge to the markets in a couple of ways. First, by raising the cost of borrowing for companies and consumers, they may slow economic growth. Second, American equity valuations are very high. The cyclically adjusted price-earnings ratio (which averages profits over ten years) is 33.4, compared with the historical average of 16.8. Equity bulls have justified high stock valuations on the ground that the returns on government bonds, the main alternative asset class, have been so low; higher yields weaken that argument.

Most analysts seem to think that the latest equity decline is a temporary setback. BlackRock, the world’s largest asset-management group, has called it “an opportunity to add risk to portfolios”. Economic-growth forecasts are still strong. Fourth-quarter results for companies in the S&P 500 index have so far shown profits up by 13% and sales 8% higher than the previous year. Tax cuts will give profits a further lift and companies may return cash to shareholders via share buy-backs. All this will provide support for share prices.

Meanwhile inflation worries seem premature. Core inflation in America (excluding food and energy) is just 1.5%. Despite a higher oil price, Bloomberg’s commodity index is nearly where it was a year ago. The same goes for American inflation expectations, as measured in the bond market.

Two issues will determine whether analysts are right to be sanguine. The first is whether the recent gyrations in the stockmarket were reactive, responding to the recent rise in bond yields, or predictive, in the sense of spotting future trouble.

The second relates to the theories of Hyman Minsky, an economist who argued that when growth has been strong for a while, investors tend to take more risk. This risk eventually rebounds on them, just as in 2007, when subprime mortgage loans proved worthless. Perhaps the slump in volatility-based funds or even crypto-currencies could cause a crisis at some financial institution, inflicting a dent in confidence more generally.

For the moment such dangers seem possibilities rather than probabilities. But like a horror-movie audience, once investors have been scared once, they may prove twitchy for a while.

0 comments:

Publicar un comentario