Who Wants America's Debt? A Closer Look

by: The Heisenberg

- In light of the ongoing debate about China's alleged plans to "halt" U.S. Treasury purchases, I thought I'd go over some of the scenarios for you.

- Obviously, this is an important issue given the Fed's efforts to shrink the balance sheet and Treasury's increased borrowing needs.

- What other options does China really have and what other factors are at play here?

- Obviously, this is an important issue given the Fed's efforts to shrink the balance sheet and Treasury's increased borrowing needs.

- What other options does China really have and what other factors are at play here?

Unsurprisingly, people are still debating whether China truly intends to "halt" their purchases of U.S. Treasurys or otherwise rethink their strategy with regard to how they allocate their reserves.

The Bloomberg story on this hit early Wednesday morning. I talked a ton about it over at Heisenberg Report and I wrote a piece on it for this platform as well.

Officially, Beijing suggested the Bloomberg story "might have cited wrong sources or may be fake news." I shouldn't have to say this, but somehow I feel like it's necessary: just because China says it's "fake news" doesn't mean it's not true. Increasingly, Americans seem to believe that when a story comes out that either reflects poorly on a third party or else puts the subject of the story in an uncomfortable position, the ultimate arbiter of truth is somehow the subject of the story. Clearly, that's absurd. Something like: "your Honor, my client is accused of robbing the local McDonald's, but I asked him and he said that's 'fake news', so I rest my case." Additionally, assuming nothing was lost in translation, the above quote from SAFE makes no sense. How does SAFE not know whether it's false or not? That is, what's with the "might" and the "may"? There is only one entity who knows this for sure and it's SAFE, so even if you can't necessarily trust them when it comes to whether they'd admit it if the story were true, they definitely know whether it is or it isn't, so it makes no sense for them to use the terms "might" and "may."

Anyway, there are a couple of obvious conclusions one can pretty quickly come to about this. First, China wouldn't jawbone the value of their Treasury portfolio lower if they were about to sell. That wouldn't make any sense. So if they are considering diversifying away from USD assets, it's going to unfold over the longer term. Second, this was almost surely an intentional leak designed to send a message to the U.S. about China's capacity to retaliate in the event the Trump administration gets aggressive with the trade rhetoric. I talked about this in the second linked post above. (Basically, China can drive up rates vol. and if suppressed rates vol. is what's ultimately keeping cross-asset vol. tamped down across the board, then China could theoretically try and engineer a jump in the VIX and an equity selloff in the U.S. by pushing up Treasury yields with vague threats about halting purchases.)

All of that said, this is something that's worth discussing, especially in light of the fact that Treasury's borrowing needs are set to rise going forward thanks in part to the tax bill increasing the deficit (see full projections here) and the Fed allowing its balance sheet to run off.

Additionally, it seems like some coincidence that Bloomberg just happened to get the information that served as the basis for their story on Wednesday when 10Y yields had just hit 9-month highs following the BoJ cutting purchases on 10-25Y JGBs and amid calls from the likes of Bill Gross for the beginning of a bond bear market. It is not at all far-fetched to suggest that Beijing saw an opportunity to amplify the message they wanted to send to Washington so they threw a bit of gas on the fire.

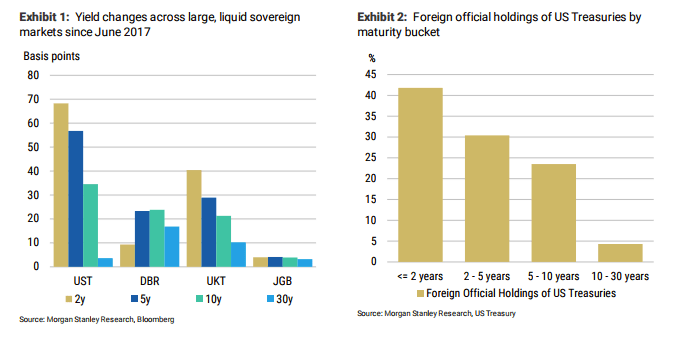

Well, according to Morgan Stanley, it's not realistic for China to make a concerted push away from U.S. debt. For one thing, comparable debt (in terms of quality and liquidity) simply doesn’t yield as much. Here's the comparison:

(Morgan Stanley)

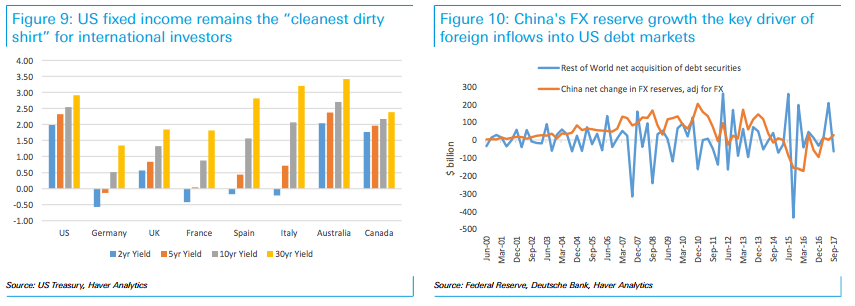

Deutsche Bank made a similar point on Friday evening on the way to adding a bit of additional color the gist of which is that the sheer size of the flows make the U.S. market the only realistic option. To wit:

It remains the case that the US, and perhaps more broadly speaking members of the dollar bloc, generally offers the highest nominal yields – this is the “cleanest dirty shirt” argument. However, the sheer size of Chinese flows creates a natural limit to the ability of investors from this market to diversify away from Treasuries.

Indeed, the flow of funds report and reserve balance data illustrate that the average increase in Chinese FX-valuation adjusted reserves has frequently and significantly exceeded the total net flow of capital into debt securities from the “rest of the world”.

The simple fact remains that in the short run, the US fixed income market is the only market with sufficient size and depth to accommodate the bulk of the demand from China.

BofAML (and Bloomberg's Richard Jones) suggested that the timing of the news out of China isn't coincidental for another reason (i.e., in addition to the fact that it seemed deliberately timed to coincide with a burgeoning selloff in Treasurys). Here's BofAML:

The announcement is timely as it coincides with French President Macron’s official visit and an interesting takeaway from the comments is that China officials have cited trade tensions as a factor in their decision. With politics in the Euro Area on a more stable footing, improving macro fundamentals and the end of ECB QE in sight, the EUR as a reserve currency appears to be an increasingly attractive long-term proposition.

That QE bit is important. As the ECB tapers, UST-EGB spreads should narrow, making the latter more attractive than they are currently. But that seems like a shift that would take place over the longer term. (I mean, I don't even know if this would be a concern, but if you moved into EGBs too quickly, the mark-to-market losses as the ECB tapers would offset the yield pick-up, so you'd probably want to wait until that had played out.)

Moreover, China still runs a trade surplus and assuming exporters repatriate the dollars they receive; the PBoC will have to do something with those dollars or else exchange them for other currencies in order to buy non-USD assets. Here's Morgan Stanley on that (from the same note cited above):

If China’s central bank keeps the US dollars instead of converting them into other currencies, what does it buy that is (1) cheaper and (2) offers comparable liquidity to US Treasuries?

That's a rhetorical question. Morgan Stanley doesn't think China has any good options in that regard.

But look, the bottom line here is that international demand for Treasurys is something to keep an eye on in an environment of rising supply and decreased Fed support for the market.

Reduced policy divergence between the ECB/BoJ and the Fed (i.e., the ECB taper and presumed 2019 hike and the BoJ's first steps away from accommodation) will naturally play a role as will the evolution of hedging costs (basis swap levels).

The irony is that in the event a severe Treasury selloff triggers a tantrum that flips stock-bond correlations positive (i.e., there's no diversification and balanced portfolios experience a drawdown), the flight to safety could end up underpinning the very assets that sparked the panic in the first place.

0 comments:

Publicar un comentario