The world economy hums as politics sours

But growth remains vulnerable to financial crises, inflation shocks and war

Martin Wolf

© Bloomberg

The world at the beginning of 2018 presents a contrast between its depressing politics and its improving economics. Might this divergence continue indefinitely? Or is one likely to overwhelm the other? And, if so, will bad politics spoil the economy, or a good economy heal bad politics?

As I argued last week, we can identify several threats to a co-operative global political order. The election of Donald Trump, a bellicose nationalist with limited commitment to the norms of liberal democracy, threatens to shatter the coherence of the west. Authoritarianism is resurgent and confidence in democratic institutions in decline almost everywhere. Meanwhile, managing an interdependent world demands co-operation among powerful countries, particularly the US and China. Worst of all, the risks of outright conflict between these two superpowers are real.

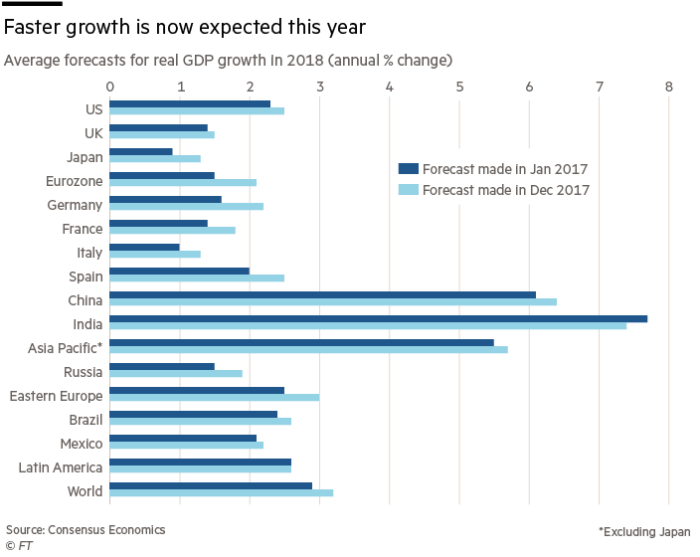

Yet the world economy is humming, at least by the standards of the past decade. According to consensus forecasts, optimism about prospects for this year’s growth has improved substantially for the US, eurozone, Japan and Russia. The consensus also forecasts global growth, at 3.2 per cent next year (at market prices), slightly above the rapid rate of 2017. (See charts.)

The economist Gavyn Davies is still more optimistic. In his view, the consensus still lags behind the exceptionally strong quarterly numbers identified in “nowcasts”. He expects further upward revisions to forecasts. He even argues that global activity is currently growing at an annualised rate of about 5 per cent (measured at purchasing power parity, which raises global growth rates by about half a percentage point above growth at market prices).

This would also be over a percentage point above trend growth. On the face of it, this rate is unsustainable. An optimistic response might be that forecasters have underestimated the trend.

More important, investment is playing a big role in generating stronger demand, especially in the eurozone. In turn, stronger demand drives higher investment. In the second half of 2017, notes Mr Davies, investment in the US, eurozone and Japan increased at quarterly annualised real rates of 8-10 per cent, far better than anything since 2010. A virtuous circle of fast growth driving faster potential growth is surely conceivable.

If this growth rate proves unsustainable, the question is whether it comes to an end smoothly or with a bump. The risks of bumps are significant, given elevated levels of debt and high asset prices, notably of US stocks. Meanwhile, happily, inflation remains subdued, and real and nominal interest rates low. For the moment, the latter conditions make debt more bearable and high asset prices more reasonable. Disruption could easily arrive, however, perhaps from stronger inflation or doubts about the solvency of big debtors. It could also come from collapses of overvalued asset prices or turmoil in overstretched debt markets. If economies then started to slow substantially, the room for manoeuvre on monetary or fiscal policy of the high-income countries would seem small.

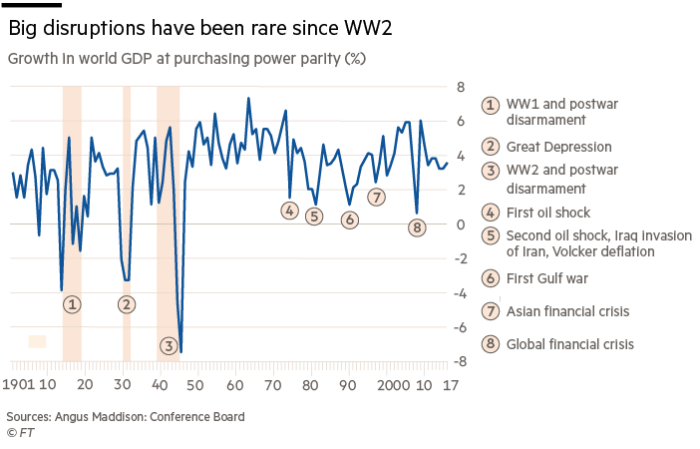

Nevertheless, as I argued a year ago, such big economic disruptions are rare events.

Remarkably, the world economy has grown in every year since the early 1950s. Moreover, it has grown by less than 2 per cent (measured at purchasing power parity) in only five years since then: 1975, 1981, 1982, 1991 and 2009.

What has created sharp (and usually unexpected) slowdowns? The answers have been financial crises, inflation shocks and wars. War is the biggest political risk to the economy. In the early 20th century, few Europeans imagined the economic and social devastation that lay ahead. Nuclear war could be two orders of magnitude more destructive.

Wars among oil producers have also been highly disruptive: consider the two oil shocks of the 1970s. A war between Iran and Saudi Arabia might be quite devastating. Policy and so politics also play the dominant role in generating inflation and subsequent disinflation shocks. Politics also drives protectionism and irresponsible financial liberalisation. Overall, the risks of disruptive politics might be higher today than in decades.

Politics also shape the longer-term policies that determine the performance of economies. We know policies are often far from being as supportive of widely-shared and sustainable growth as they might have been. Neither the right’s idea that the only thing necessary is to slash taxes and regulations, nor the left’s view that a more interventionist state would solve everything makes sense. Reigniting dynamism is challenging.

Yet it is also possible to have a more optimistic perspective. The bad politics of today are, in significant part, the result of the bad economics of the past, especially the post-crisis malaise in high-income countries and the impact of the subsequent commodity price collapse on many emerging and developing countries. One may hope that as the world economy recovers and optimism about the future becomes entrenched, the distemper of politics in so many countries will start to heal. This might also begin to restore confidence in political and economic elites.

That might make politics less bellicose and more consensual. It might also pull debate away from the wilder shores of populism.

For some time, then, economics and politics can go their somewhat separate ways. In the longer term, however, the questions must be whether the economy fails on its own, the politics end up ruining the economy, or, best of all, the economy cures the politics. Let us hope for the last.

That is worth struggling for.

0 comments:

Publicar un comentario