US yield curve flattens at fastest pace since financial crisis

Short-term rates shoot up as Congress nears passage of sweeping tax bill

John Plender

US President Donald Trump meets with small businesses to discuss tax reform, which has contributed to recent yield curve steepening © EPA

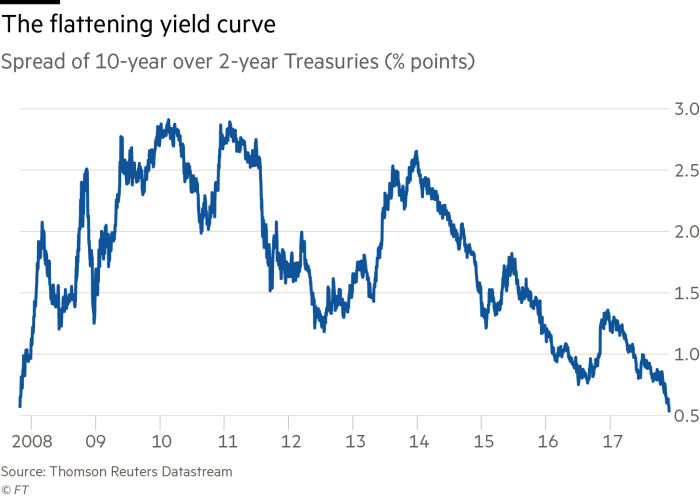

The difference between short-dated and longer-dated US Treasury yields has narrowed at its fastest pace since 2008, as investors anticipate a quicker rate of policy tightening from the Federal Reserve next year.

The difference between two- and 10-year yields has fallen 33 basis points to just 52 basis points over the past 30 days, while the difference between five- and 30-year yields has fallen 34 basis points, surpassing declines prompted by the European sovereign debt crisis in 2011 and reaching a pace last seen during the financial crisis, according to analysts at Citi.

It marks a pronounced “flattening” of the yield curve, with investors receiving decreasing returns for holding longer-dated bonds compared to shorter-dated notes — typically a harbinger of economic recession.

But some investors and analysts say the driving forces for the current move are different. Heightened expectations for the passage of tax reform into law could offer a short-term boost to the economy, but were unlikely to trigger a long-term boost to inflation that would drive longer-dated yields higher, said Ian Lyngen, head of US interest rate strategy at BMO Capital Markets.

“It’s pretty straightforward. It will keep the Fed on path to keep normalising but it won’t trigger the kind of stimulus that might introduce more significant inflation,” he said.

The probability that the Fed will increase the target Fed funds rate when it meets in December have hit 98.3 per cent as implied by the markets, up from 87.5 per cent the day after the Fed last met at the beginning of November.

Increasing expectations of interest rate rises from the Fed have helped drive the more policy-sensitive two-year Treasury yield up 54 basis points since early September to 1.80 per cent this week. In contrast the 10-year note yield has remained stuck between 2.30 per cent and 2.46 per cent since mid-October and on Wednesday was around 2.33 per cent.

Mr Lyngen also pointed to the Senate’s inclusion of the alternative minimum tax — a baseline, parallel tax assessment that permits fewer deductions — as damping the stimulative effect of tax reform. It may still be removed as the House and Senate seek to align their proposals but analysts say its inclusion would provide a floor to the benefit received by companies, with effective tax rates already below the statutory 35 per cent.

Market gauges of investors’ inflation expectations have remained muted since the passage of the Senate’s tax proposal. The 10-year break-even inflation rate edged slightly lower on Tuesday to 1.88 per cent.

Analysts also point to strong demand for longer-dated bonds as another factor weighing on yields.

Foreign investors have been big buyers of Treasuries this year, attracted to the higher-yielding asset compared to high-quality government debt elsewhere across the globe. Domestically, traders say pension funds have been driving recent demand.

“That is going to continue to put pressure on the yield curve to flatten,” said Andrew Brenner at National Alliance.

0 comments:

Publicar un comentario