Time To Talk About A Revolution

by: Eric Parnell, CFA

- Recent focus has been on the tax debate in Washington.

- The discussion about the trees largely misses the bigger problem with the forest.

- Where are the surpluses in one of the longest economic expansions in U.S. history with stocks trading at all-time highs for several years now.

- It is time to talk about a revolution in the way we think about economic policy going forward.

Who or what is next?

- This idea was discussed in more depth with members of my private investing community, The Universal. Become a member today >>

Talk about taxes has shifted into high gear. The daily financial headlines are filled with play-by-play updates on how the development of prospective legislation on U.S. “tax reform” is evolving both in the House and the Senate. And the media airwaves have no shortage of debate about the nuances of the debate as it unfolds on a daily basis. But completely missing from the ongoing discussion is a much bigger issue. Instead of talking about tax cuts, it’s time to begin talking about a revolution in fiscal policy unlike anything we have seen in our lifetimes.

The Trees

The financial news media has been flooded as of late with discussion about taxes. What was once a dialog about “tax reform” has since evolved into talk about “tax cuts”. And it all makes for interesting headlines to follow as we quickly wind our way toward Thanksgiving here in the United States.

But here is the thing. The whole debate is largely pointless. For example, we read a headline about a prospective change being made to the legislation being put together in the House, and analysts will come together to opine over its implication for the economy and financial markets.

Securities prices might even move, sometimes dramatically, in knee jerk response to such headlines. But the fact of the matter remains that much of whatever ends up in the House bill is likely to disappear once the debate makes its way through the Senate and then to conference between the two chambers to create the final bill. All of this assumes that a bill can even make it through the House and then through the Senate. And all of this is supposed to happen by the end of the calendar year. Good luck, my friends.

Overall, the probability of any tax related legislation being signed into law by the end of 2017 is increasingly fading. According to PredictIt, the probability for individual tax cuts by the end of the year has fallen below 10% in recent days after odds were as high as one-in-three at the start of the month and fifty-fifty during the summer. The implied odds for corporate tax cuts are equally bleak at roughly 20%, which is down from 35% at the start of the month.

Put simply, the markets never had a high degree of confidence in recent months that “tax reform” or “tax cuts” were going to happen by the end of the year, and any lingering hopes for legislation are increasingly fading as the clock on the 2017 calendar year starts to run out.

The primary argument in favor of tax legislation getting done before the end of the year is a qualitative one. Simply, the thinking goes that Republican lawmakers simply have no choice politically but to get something done before the end of the year. But a similar case could have been made for healthcare reform, yet nothing was passed at the end of the day despite multiple attempts.

And it appears that too many internal conflicts may exist within the tax legislation debate to thwart agreement this time around as well. Such are the challenges of governing that are faced on both sides of the political aisle at various points throughout time.

What about 2018? The potential certainly remains for legislation to be passed sometime next year.

But the closer we draw to the mid-term election cycle, the more difficult it will become to get anything done from a legislative standpoint, particularly if a bill includes aspects that may prove controversial in the political debate with middle class voters.

Putting this all together, the “tax reform” debate that eventually evolved into the “tax cut” debate is largely moot. Despite the various ideas being discussed, it remains unlikely to happen in 2017 and potentially not at all. This is not at all a political statement. Instead, it is the reality implied by calendar and the betting markets.

The Forest

What is genuinely bothersome to me about the recent tax debate as it relates to fiscal policy is the following. Why the heck are we even having the conversation that we are having about taxes in the first place?

Consider the excerpt from an effectually factual update article shown below:

“The latest version of the House bill would add $1.7 trillion to the federal deficit over 10 years, said the nonpartisan Congressional Budget Office, which tallies the costs of legislation. That would violate a rule requiring the legislation to add no more than $1.5 trillion to the deficit. But Representative Kevin Brady, Republican chairman of the House tax committee, said he would revise the legislation on Thursday to bring it into compliance.”

- Tax-cut debate in U.S. Congress swings to Senate bill, Reuters, November 8, 2017

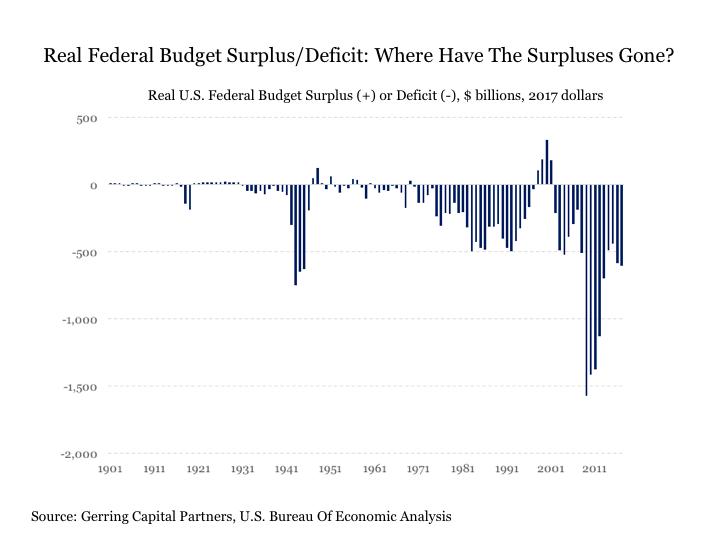

Let’s get this straight. Legislation is being considered that needs to be whittled down to adding just $1.5 trillion to the Federal deficit over the next 10 years. This averages out to another $170 billion being added to the deficit in 2018, 2019, 2020, ..., and 2027. This is on top of an estimated Federal budget deficit for the current year of -$602 billion that is estimated to come in between -$450 billion and -$550 billion each year over the next five years according to the U.S. government itself in the Bureau of Economic Analysis that we all know will end up being more than -$450 billion to -$550 billion per year at the end of the day regardless of what party is in control in Washington.

What in the name of John Maynard Keynes is going on here!?! And why in the world is virtually nobody in the mainstream financial media even talking about the key fundamental problems that exist with what is even being debated in fiscal policy circles at the present time!?!

What exactly am I chirping about here? Why are we even having a discussion about tax cuts that are going to add $1.5 trillion to the deficit over the next ten years (once again, we all know it’s going to end up being a heck of a lot more than $1.5 trillion by the time we reach 2027). In fact, why are we even having a conversation about adding a mere penny to the deficit? Instead, where the heck are the surpluses!?!

Why surpluses, you might ask? For the following reason.

We are already currently in the third longest sustained economic expansion in U.S. history dating back to the mid-1800s. At 98 months, it is quickly closing in on the number two spot held by the 106-month expansion from February 1961 to December 1969. If it can stay on track for another year beyond that, it will claim the all-time top spot currently held by the economic growth period from March 1991 to March 2001. And if a recent note from Goldman Sachs (GS) is any guide, it is assigning a two-in-three chance that the current expansion will pull off becoming the longest on record.

Certainly, the recovery has been anything but robust in magnitude. But it has been extensive in duration. And it is showing no signs of letting up anytime soon under the current set of fiscal policy circumstances. Moreover, if the U.S. stock market (DIA) as measured by the S&P 500 Index (SPY) is any indication (I’m not really sure that it is anymore, but let’s just humor the thought for a moment), then the underlying economic outlook is much more awesome than the past and current economic data might suggest.

If we are already in what may soon become the longest economic expansion in U.S. history with a stock market that has been repeatedly trading at all-time highs for several years now, what then is the theoretical justification for more federal budget deficits? Spare me the “future growth will pay for today’s deficits” argument, as decades of past evidence as shown in the chart below more than confirms that the additional money ends up getting spent elsewhere other than going back into the Federal coffers at the end of the day.

I was generally supportive from a fiscal policy standpoint of the original debate around potential “tax reform”. For “tax reform” implies a larger change in the tax code where tax revenue resources can be redirected from inefficient and wasteful policies that are curbed or eliminated to areas that can support productive and sustainable growth while also creating greater fiscal flexibility for the government going forward. Put more simply, “tax reform” that involves tax cuts that are paid for by making the tax code more efficient with some money left over in the process (ideally surpluses, but I’ll even take a reduction in the deficit) makes good sense, particularly when we are in the midst of one of the longest sustained U.S. economic expansions in history.

But as the 2017 calendar year has evolved, it became increasingly apparent that “tax reform” in its true sense was simply not going to happen. Instead, the debate has slowly morphed into talk about “tax cuts” that are not going to be fully paid for by offsetting changes in the tax code. Put simply, fiscal policy makers are currently trying to figure out ways to spend even more money without the tax revenues to support it. And once again, they are trying to do so in the midst of one of the longest sustained U.S. economic expansions in history.

The Fundamental Problem

Why does all of this matter? So what if we continue to run deficits? Because the instance on continuing to run massive budget deficits not only in the U.S. but also across the globe despite the supposed economic growth and prosperity runs contrary to the economic theory first put forth by John Maynard Keynes and eventually implemented by much of the world’s free market economies during the Great Depression. The so-called Keynesian Revolution replaced the preceding neoclassical economic theory that operated under the principle that the free market would independently adjust itself over time and move toward full employment without government intervention. And since this revolution more than eight decades ago, the global economy has operated under the general direction of Keynesian economics.

The primary fundamental tenant of Keynesian economics is the following. When an economy falls into recession (or worse, depression), the government can intervene with increased spending and lower taxes to help fill the associated output gap and stimulate aggregate demand to promote economic recovery. In other words, the government can justify deficit spending to help smooth out the economic dips and get positive growth up and running again. Global governments include the United States get one mightily resounding check in this regard. Mission not only accomplished but also completely obliterated.

But there is a subsequent step involved with the proper implementation of Keynesian economics that has gone missing for the last half century now as evidenced by the budget surplus/deficit chart shown earlier in this report. And it is a missing step that has become increasingly worse over time. For the important counterbalancing next step of Keynesian economics is that once the economic recovery has been achieved, governments must subsequently run budget surpluses in order to eliminate the debt accumulated during the prior period of economic weakness. Stated more directly, the government can justify running up the Federal credit card during tough times, but only if it pays off these bills once things get better.

In short, properly implemented Keynesian economics is all about balance. But any effort to maintain this balance was abandoned decades ago now. It has been so long ago forgotten now that those in politics on either side of the political aisle as well as those in the financial media hardly even think to consider it anymore. Instead, simply not adding anything more to an already existing massive deficit is considered pious if not stingy, while how much more we can add to the deficit regardless to underlying economic prosperity becomes the crux of the discussion. The imbalance becomes perpetual and increasingly perilous in the process.

Another Revolution Coming To Washington?

Where have these imbalances brought us today in 2017?

We have seen three major economic crises in the past - the stagflationary period of the 1970s and early 1980s, followed by the bursting of two major asset bubbles in the 2000s. Upon reflection, it was no coincidence that each of these trying economic periods came in the wake of the two longest economic expansions in U.S. history. For the longer excesses are accumulated, the more likely they are to lead to increasingly traumatic consequences once they are finally released. It is also no coincidence that the real fiscal budget deficits were sustainably increased in the aftermath of each successive corrective episode, as an even greater amount of deficit spending is required to put out each successively new fire.

All of this brings us to 2017, where what was once described under Keynesian economic theory as government intervention in free markets in order to smooth the recessionary cycle has evolved over time to what has become today the government completely overtaking free markets regardless of where we are in the economic cycle with an overwhelming torrent of fiscal and monetary policy support. It has no longer become a question of whether the government will intervene at any given point but by how much it will intervene at all points in time.

So what has this excessive intervention yielded us? We have income inequality and a wealth gap that is increasingly widening with each passing year. We have real wages that have been stagnant to declining for years if not decades now. We have structural unemployment that has been deteriorating for years across many parts of the United States. We have corporations that have a greater incentive toward share buybacks and dividend distributions than to growth enhancing capital expenditures. And we have increasing social unrest not only in the United States but also across the globe that has resulted in the increasing popularity of politicians and parties that once resided on the left and right fringes of the political spectrum but are now increasingly making their way into the mainstream.

Imbalances continue to accumulate. Disparities continue to widen. People are becoming increasingly frustrated. All that is missing is a major economic event to spark the catalyst for change. And the longer and further that we continue down the current course, the less the question of change becomes about “if” and the more it becomes about “when”.

The Bottom Line

A revolution is coming in the theory that drives our global economies and financial markets.

Keynesian economics has lasted for more than eight decades now, but it is increasingly descending toward its demise in the coming years. It’s certainly not Keynes’ fault, as I strongly assume he would not have advocated the gross, one-sided mismanagement of the implementation of his economic theory for so many years. But the imbalances that have been created over so many years have culminated in extremes whose resolution will likely require the next John Maynard Keynes to soon step forward in the coming years with the next revolution in economic theory to lead our economy through the remainder of the 21st century and into the 22nd.

All of this may sound alarming. I can already imagine some sharpening their “doomsday” knives for the comment section. But the notion of long overdue change is not alarming. Instead, it is necessary to achieve the progress required to more successfully move forward. Today’s reality is that the U.S. and global economy has been increasingly stagnating for years despite the best efforts of policy makers to intervene along the way. We’ve been seeing it in Japan since the end of the 1980s, and we’re increasingly seeing it across the rest of the developed world since the start of the new millennium. The populace around the world is becoming increasingly restless for more widespread prosperity that extends beyond the highest echelon, and staying the course simply will not lead us to this outcome.

The global and U.S. economy is vastly larger today than it was during the Great Depression. And we have John Maynard Keynes and the revolution that resulted from his economic theory to thank for this tremendous progress. But we are now quickly moving toward the next crossroads where a now stale, eight decades old economic theory needs some major refreshing.

Maybe it will become some new modified form of Neo-Keynesianism. Then again, maybe it will be something entirely revolutionary. And it certainly may not require another economic depression to inspire such change depending on how proactively policy makers seek to adapt any potential new way of thinking.

Maybe it will become some new modified form of Neo-Keynesianism. Then again, maybe it will be something entirely revolutionary. And it certainly may not require another economic depression to inspire such change depending on how proactively policy makers seek to adapt any potential new way of thinking.

But the fact that we are now watching a tax debate unfold that is contemplating how much further we may add to an already large deficit in the midst of one of the longest economic expansions in U.S. history demonstrates how far off the fiscal policy path we have gone on both sides of the political aisle from the original Keynesian economic framework and how inevitable an eventual change is becoming. Once again, it is becoming less a question of “if” instead of “when”.

Any such “when” will not happen overnight but instead will evolve slowly over time. But if it does come to pass, it is not likely to take place without disruptions to financial markets. This includes potential dramatic effects on stocks (IVV), bonds (BND), commodities (DJP), precious metals (GLD) (SLV), and the existing and still relatively young at 46 years fiat currency system as we know it today including the U.S. dollar (UUP). This is not to say that any of these assets will necessarily gain or lose value in any potential future transformation process. But what it does suggest is that the record low volatility (VXX) that investors have been enjoying during the monetary policy morphine drip years since the calming of the financial crisis more than eight years ago would almost certainly come to an end with much more dramatic swings in asset prices versus anything we have seen in recent memory taking its place. And with the looming end of net increases in monetary stimulus from global central banks starting in the coming months of 2018, this transformation may start to come sooner rather than later at this point. Only time will tell.

All of this highlights the importance of being prepared for what may lie ahead. Perhaps global capital markets will remain sanguine through it all. Perhaps we will finally achieve the more robust economic growth that has been so elusive throughout the post crisis period of “prosperity”. Then again, we may see something altogether different take place in the coming years. In the event that we do, capital markets will remain rich with upside opportunities that may even be far more attractive than what is on offer today. But such opportunities will not necessarily come easy and will require more work and a plan that extends beyond buying and holding the latest index fund du jour and hoping for the best. And those that are prepared in advance and remain watchful of what might unfold on the policy front in the coming years will be those that are best positioned to capitalize once something other than everything being absolutely awesome finally arrives on the global capital markets scene.

Continue to enjoy the stock market upside as we have for so long during the post crisis period.

But also remain watchful and prepared for what may lie ahead. For the latest tax policy debate is yet one more confirmation that a revolution may eventually be coming to the way we all think about economics going forward.

0 comments:

Publicar un comentario