The Federal Reserve Has Never Printed 'Money': The End Game

by: Eric Basmajian

- The first three parts to this series covered the mechanisms of Federal Reserve operations, the unintended consequences of too much debt and the resulting issues from the increase in bad debt.

- Critics say that the US will not be able to repay its debt obligations and that hyperinflation will result in a collapse of the US dollar; this is likely inaccurate.

- Currencies are valued on a relative basis and our major trading partners are far more indebted, meaning that their currency must depreciate before the dollar.

- The only way all currencies can fall together (since they are relative) is to devalue against gold or some other hard asset commodity - an unlikely scenario.

- Critics say that the US will not be able to repay its debt obligations and that hyperinflation will result in a collapse of the US dollar; this is likely inaccurate.

- Currencies are valued on a relative basis and our major trading partners are far more indebted, meaning that their currency must depreciate before the dollar.

- The only way all currencies can fall together (since they are relative) is to devalue against gold or some other hard asset commodity - an unlikely scenario.

Overview

This is the final segment to this four part series on the Federal Reserve, 'money printing,' the unintended consequences of Federal Reserve policy such as debt accumulation, the impacts to the economy and finally the end game.

The first part to this four-part series covered the mechanisms in which the Federal Reserve conducts open market operations and how the Fed has never actually printed money in its truest sense of the word but rather increased the monetary base through crediting reserve balances of primary dealers.

Reserves are not considered money and are not part of M1 or M2 but rather are part of the Monetary Base. The Federal Reserve had hoped to increase inflation by having the banks loan out their newfound reserves, which would thereby strongly increase the growth in the money supply and cause inflation.

This did not occur as the rate of bank lending never exceed the historical average and was lower than average in most cases, resulting in a growth of the money supply that was consistent with past decades. Because money supply growth was more or less constant and the velocity of money has been in decline, two factors that contribute to aggregate demand, the rate of inflation has been continuing to fall and has not exceeded the 2% Federal Reserve target with any degree of consistency, much to the surprise of popular market opinion.

The first part covers this process in great detail, and I strongly encourage you to read that part if you have not done so already. You can find the article by clicking here.

The second part to this series covered the unintended consequences of Quantitative Easing (QE) and zero interest rate policy (ZIRP) as well as the structural and secular issues of over-indebtedness, which have been exacerbated by these aforementioned polices.

The overload of debt that has accumulated recklessly over the past few decades, compounded by misguided Federal Reserve policy, has brought the economy to a point where we have mortgaged all our future growth for current (past) consumption. The anemic rates of growth over the past decade are a result of a massive debt increase in the four critical non-financial sectors of the economy (Federal, State & Local, Corporate, Household).

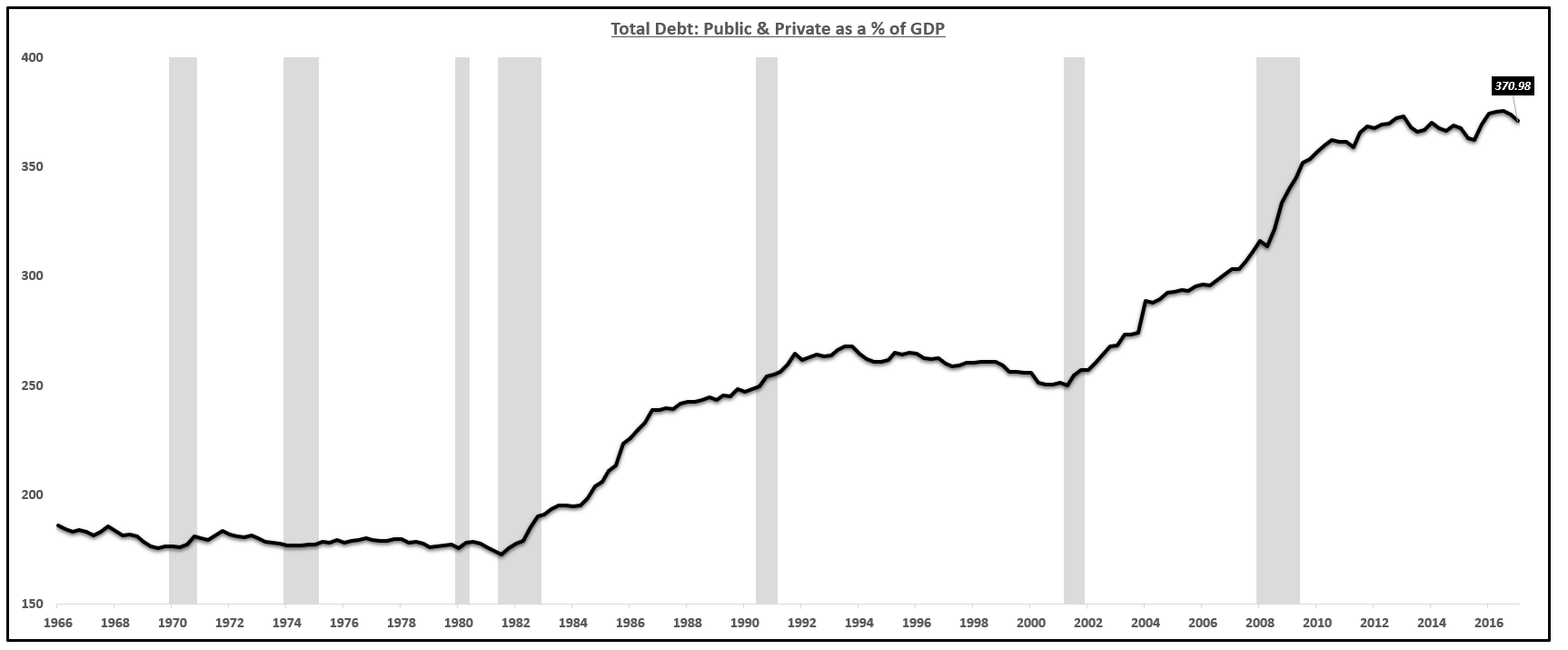

Total economic debt for the United States (public and private) has surpassed $70 trillion and now stands over 370% of Gross Domestic Product [GDP].

Total Public & Private Debt As A % Of GDP (Excluding "Off-Balance Sheet" Items):

Source: Federal Reserve, Bank For International Settlements, US Treasury

Source: Federal Reserve, Bank For International Settlements, US Treasury

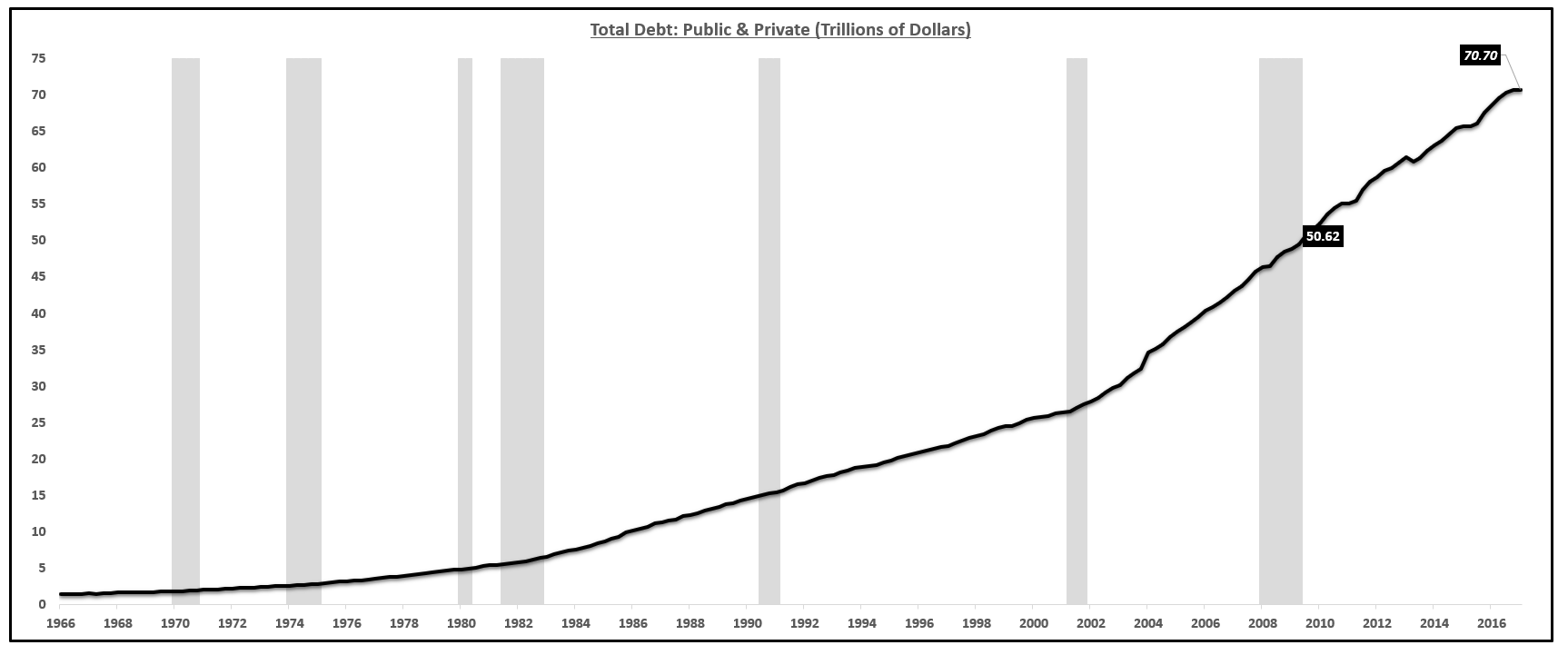

Total Public & Private Debt (Trillions) (Excluding "Off-Balance Sheet" Items):

Source: Federal Reserve, Bank For International Settlements, US Treasury

Source: Federal Reserve, Bank For International Settlements, US Treasury

Part II of this series outlines the debt problem across all the economic sectors in more detail as well as how the increase in debt will mathematically guarantee lower rates of growth in the future without some positive shock to the economy. You can find the article by clicking here.

The penultimate part to this series on the Federal Reserve detailed the consequences and symptoms of an over-indebted economy.

Increases in debt raise the cost to service that debt, which lowers the saving rate, lowers the velocity of money, lowers long-term interest rates and causes companies to forego growth-generating projects in exchange for financial engineering.

These dynamics further decrease the productivity of the labor market, which cause a secular decline in wage growth, amplifying the problem and making it more difficult to pay down debt.

The Federal Reserve, through ever-tightening monetary policy, is taking steps to further decrease the growth in the money supply (M2), which multiplied with falling velocity, will stand to reduce the growth rate of the economy at an accelerating pace.

This final part will cover why the end game to this problem of over-indebtedness will not end in hyperinflation as many suggest but more likely will end with one of crushing deflation, similar to the results of the 1930s and 2008, two massive economic issues brought about by a systemic issue of over-indebtedness.

As I stated in part III, my current forecast is that the Federal Reserve is going to reverse the course of monetary policy before the end of 2018 due to severe disinflation and anemic or even recessionary levels of growth brought on by excessive debt, and that the equity market (SPY) will experience a much choppier ride due to these factors. The Federal Reserve is likely to cut interest rates by the end of 2018 due to falling long-term rates (TLT) that will cause a very flat or inverted yield curve (IEF), hurting the banking sector (XLF) and changing investor sentiment to one of more caution and fear of a pending economic slowdown.

Before moving on to the end game, and ultimately how we may choose to exit such a problem that we have created, it is important to take a look at past instances of over-indebtedness, the issues that led to such levels of debt, the consequences of that debt build-up and finally, the end game or the solution to the problem.

While these occurrences of debt-induced crashes happen at irregular intervals, which is one of the challenges in forecasting the next panic year, the build-up of debt, the actions during the build-up phase and the end game/solution have all followed similar paths.

We currently sit in the fifth major occurrence of debt accumulation in the United States since the 1800s and the current build-up of obligations dwarfs the past four debt peaks which led to panics and crashes that had lasting consequences.

It comes as no surprise that the level of economic growth that we face today, with the largest build-up of debt relative to GDP in the country's history, is at its lowest point and the polices that have been implemented to fix the problem are not only unhelpful in finding a solution but are actually magnifying the same consequences that have been associated with each past instance debt accumulation.

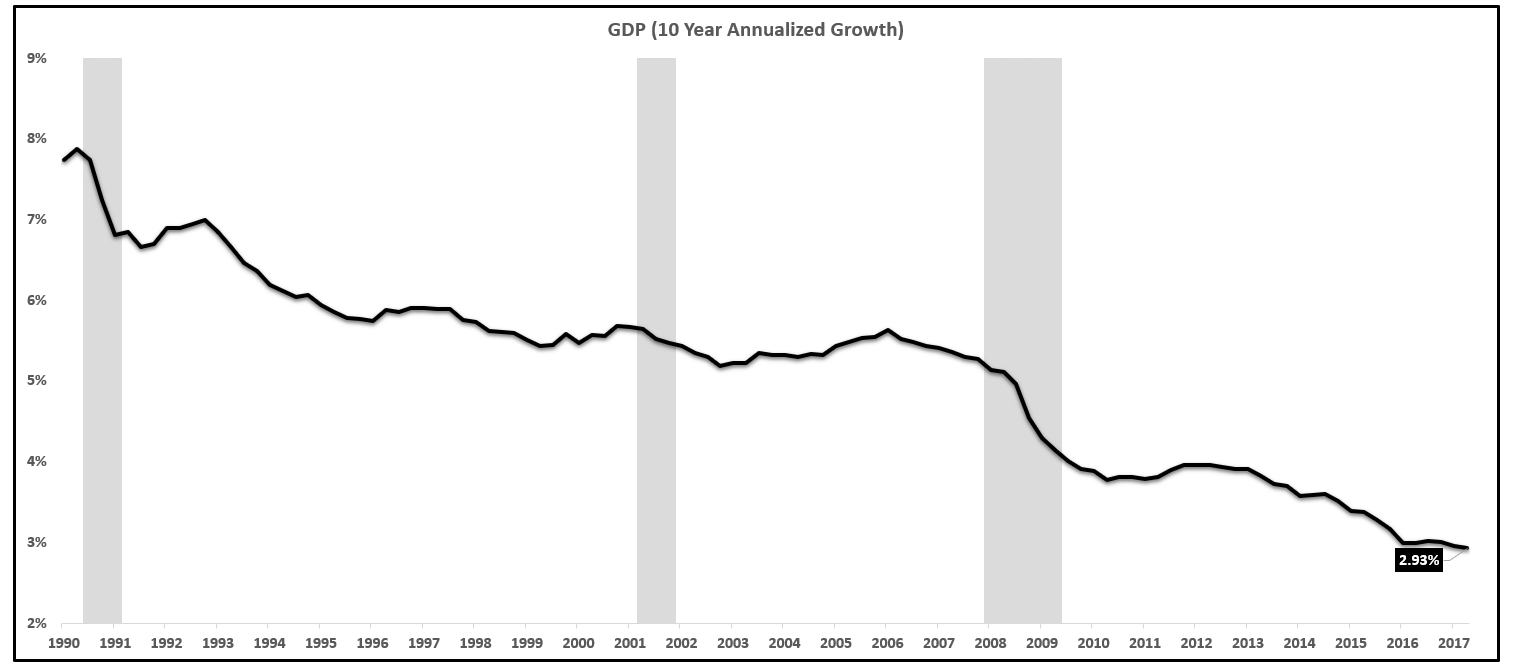

Long-Term Annualized Rate Of Economic Growth Deteriorating:

Source: BEA

Source: BEA

With debt to GDP over 370% (~$70 Trillion), nominal economic growth - that is growth and inflation - of less than 3% on a long-term trending basis is a massive problem.

You cannot grow out of debt when it is debt that is the problem causing the slow growth.

When debt reaches the levels of today, you cannot grow out of debt, you cannot inflate your way out of debt and you certainly cannot increase debt to solve the problem. You cannot fix debt with more debt. Unfortunately, the later seems to be the path we are choosing to take and have no signs of changing course.

The only solution, which I will discuss at length, is austerity. Before that discussion, let's take a look at past debt-induced panic years in the United States to spot the similarities and provide context for the magnitude of today's problem.

Brief History Of Debt Problems In The United States

There have been four major debt episodes since the 1800s, not including today's, that have all followed similar paths.

I want to preface the discussion on the past four instances of debt accumulation and the resulting panic year by saying that each of these episodes can take on a lengthy discussion, but for the sake of this paper, I will only briefly summarize each period. Invariably there will be events that contributed to each occurrence that are not mentioned but the general theme, which is what I will cover, shows consistency across time. At the risk of being overly reductionist, I will first cover the similar phases that these manifestations of debt undergo.

The process of bad debt accumulation begins with artificially created incentives. These incentives are most often created by the government, not in all cases but most commonly. The poor incentives create a desire to speculate on those manufactured incentives typically done by accumulating debt in order to fuel the speculation. The debt is used to "gamble" on these assets, most often stocks, real estate, commodities and other low cash-flow generating goods.

The cash flow that is generated from these speculative assets are not enough to repay the principal and interest of the debt that has been taken on in order to facilitate the speculation and thus the buyer has no steam of income and must rely on higher prices (greater fool theory) in order to pay down the debt. This phenomenon causes a large boom in the asset of the time. (Tulips, housing, stocks, commodities etc.)

A minority of the population sees the problems that can arise from the build of non-productive and non-cash flow producing debt in order to speculate on assets and choose to pay down their debt and exit the situation, saving themselves money and hardship in the long run in exchange for 'watching the game go on' for a period of time while others get rich, on paper, only to have it all vanish in the panic year.

After a minority of the investors' exit and additional credit (debt) becomes less available to increase further speculation, the asset prices begin to flat-line, not even decline just cease their acceleration in price growth. Due to the fact that the accumulation of debt had no cash flow and the only way to pay it back was to have a rise in the asset, a halt in the rise of the price is enough to cause another wave of investors to cut their losses and sell their speculative assets.

Once this occurs, the rest "smell the smoke at the same time" and all try and exit at once. This results in the panic year.

This process can be simplified to an issue of artificially created incentives that drive debt-financed speculation in non-cash-flow-producing assets (Ponzi-Finance), which require higher assets prices in order to repay principal and interest; a reduction in the price of the asset that has been speculated on makes the debt unpayable since the investor is now underwater and does not have a stream of cash from the asset causing a wave of selling to cut losses and a resulting crash/panic in the asset class that was primarily speculated on.

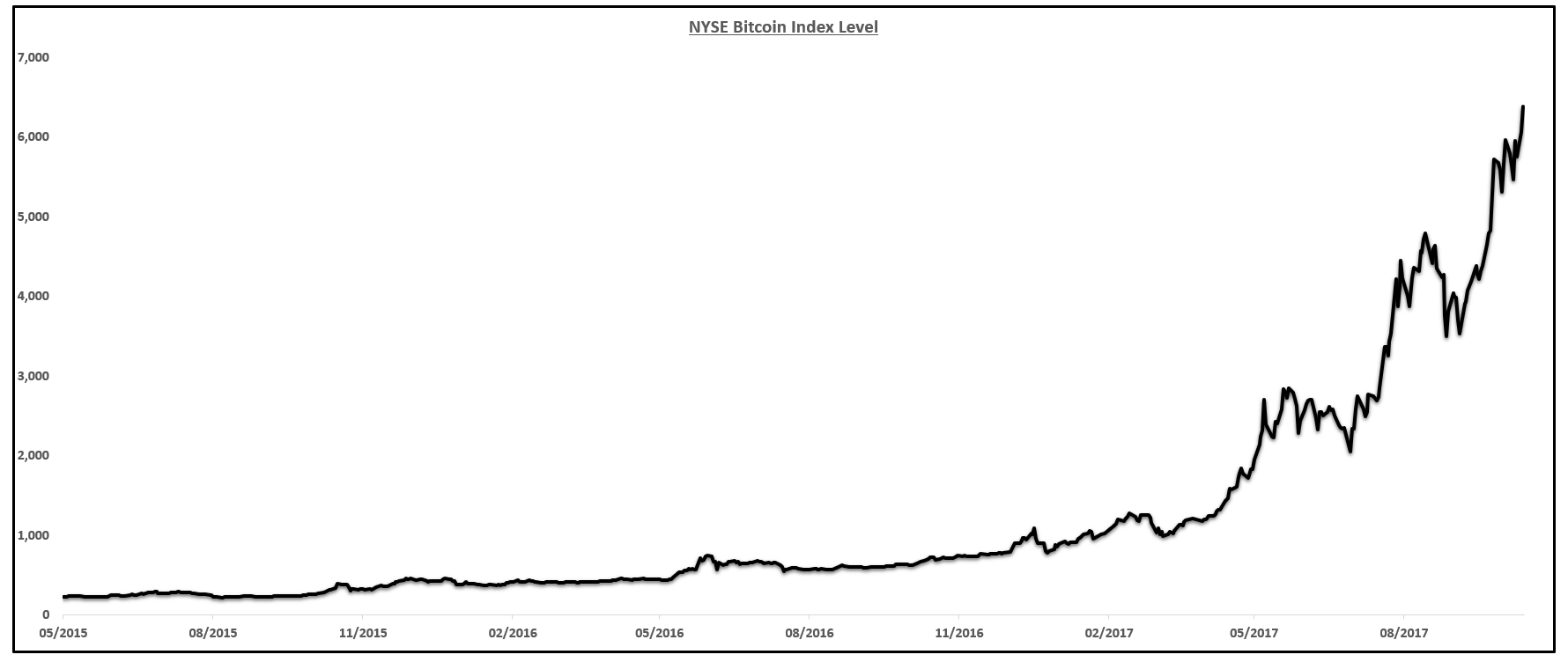

This has occurred four major times in the United States since the 1800's and is likely to happen again today due to the level of debt that has been accumulated again, for unproductive uses (stocks, real estate, bitcoin, share buybacks etc.).

Again, these summaries are overly reductionist, but the trend described above can be seen clearly in each example.

History Of Debt Accumulation:

Source: BEA, Federal Reserve, Hoisington, Census Bureau

Source: BEA, Federal Reserve, Hoisington, Census Bureau

The first episode occurred in the 1830s in which there was a massive build-up of debt in order to build the steamships, canals and other infrastructure. While this was not the worst use of debt, the issue came from speculation in real estate along the canals as well as poorly thought out factories and other investments that did not have an immediate cash flow but rather were built as a way to "flip" for an increase in price. Investors took on debt to build homes near the major ports that caused a boom in home prices. Cotton, a non-cash-flow-producing commodity, was also speculated on using debt which caused the price to soar. The bank of England saw the easy money flowing out, their reserves declining and decided to raise interest rates, and reduce the amount of money loaned. Once the availability of credit contracted and that made its way to the United States, home prices stop rising at the same rate, factories and other projects failed, cotton prices fell and the money that was borrowed was not able to be repaid since the assets purchased did not produce the cash-flow needed to repay the money. Home values fell, a portion of the debt was defaulted on, and 1837 was the panic year.

The panic of 1837 lasted until the 1860s in which another round of debt was accumulated in order to build the railroads of the United States. This was financed primarily by the government. Again, this created the incentive to speculate on real estate and other infrastructure along the rails, all fueled by an increase in household debt. Once the government sponsored railroads failed, all the assets that were driven up artificially by debt-financed speculation crashed and 1873 was the panic year.

The third episode of debt-induced panic led to the great depression. In the 1920s, shortly after the creation of the Federal Reserve, easy money policy (similar to today) was enacted and this flooded the market with liquidity and caused massive speculation in stocks, real estate and commodities. The stock market reached levels it had never seen before and multiplies exploded to their highest level the markets had seen. There were also other assets that were speculated on, incentives that were created by low interest rates and easy money, including wheat, steel and cars (non-cash flow producing commodities). When interest rates began to rise, credit availability contracted and debt was unable to expand in order to continue the rise in asset prices, a minority began to sell their assets and this caused an initial decline in asset prices.

By the time the rest of the population began to "smell the smoke," the panic year was upon them and the assets declined dramatically and the debt that was accumulated in order to speculate was not able to be repaid.

Again, I fully understand that all of these episodes are complex matters that have much more detail, but the processes that each period went through have similarities that are consistent with debt-fueled speculation.

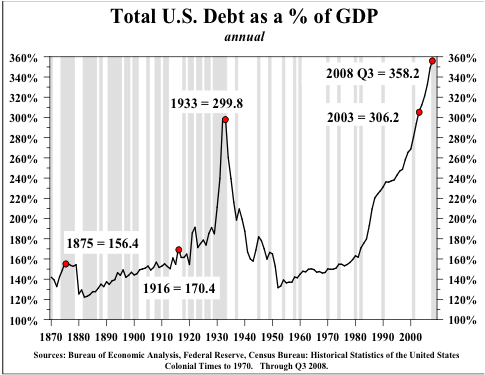

In 1933, debt to GDP was nearly 300%. Over 100 points higher than any past crash which is why the great depression was so much more severe than the past panic years.

It took over 70 years for the United States economy to reach a level of indebtedness that surpassed the 1930's.

In 2008, the economy had a level of debt over 350% of GDP. Low interest rate policy as well as other government-created incentives fueled debt-financed speculation, primarily in residential real estate, a non-cash flow producing asset. When the bubble in home prices was clear, the Fed began to raise interest rates, banks contracted lending, and the rise in home prices began to accelerate as a slower pace, declining in some instances. When the rise in the price of homes ended, the debt that was taken on by households in order to speculate on the value of homes was underwater, unable to be repaid, and a crash in home prices and a panic year ensued.

Another complex economic time, but it truly can be boiled down to artificially created incentives that caused a debt-fueled speculative bubble with the only path to repay debt was through a rise in price (greater fool theory) rather than through a stream of cash great enough to cover principal and interest. A contraction in the availability of debt in order to speculate stops the rise in that asset and causes the model of Ponzi-finance to collapse.

For those who claim the bubble was not clear, easy to spot, or not fueled by low interest rates, I humbly submit that you simply were willingly blind.

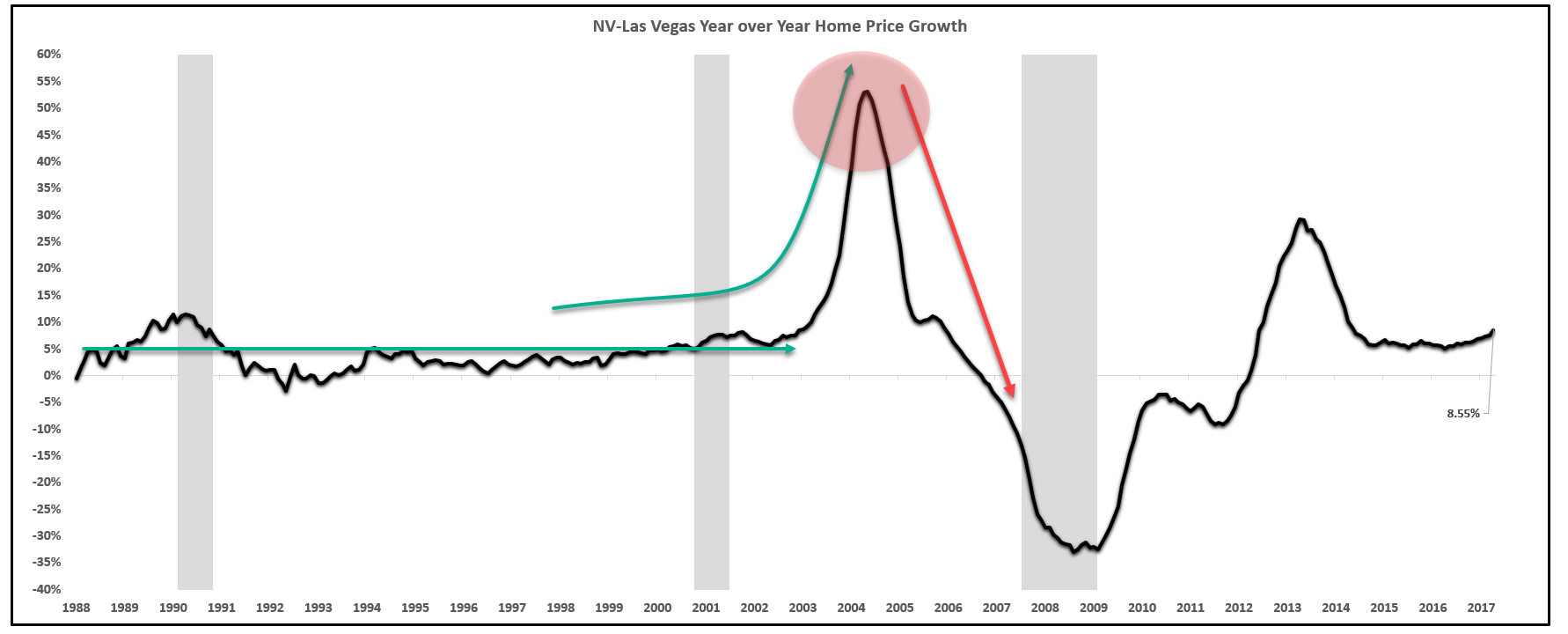

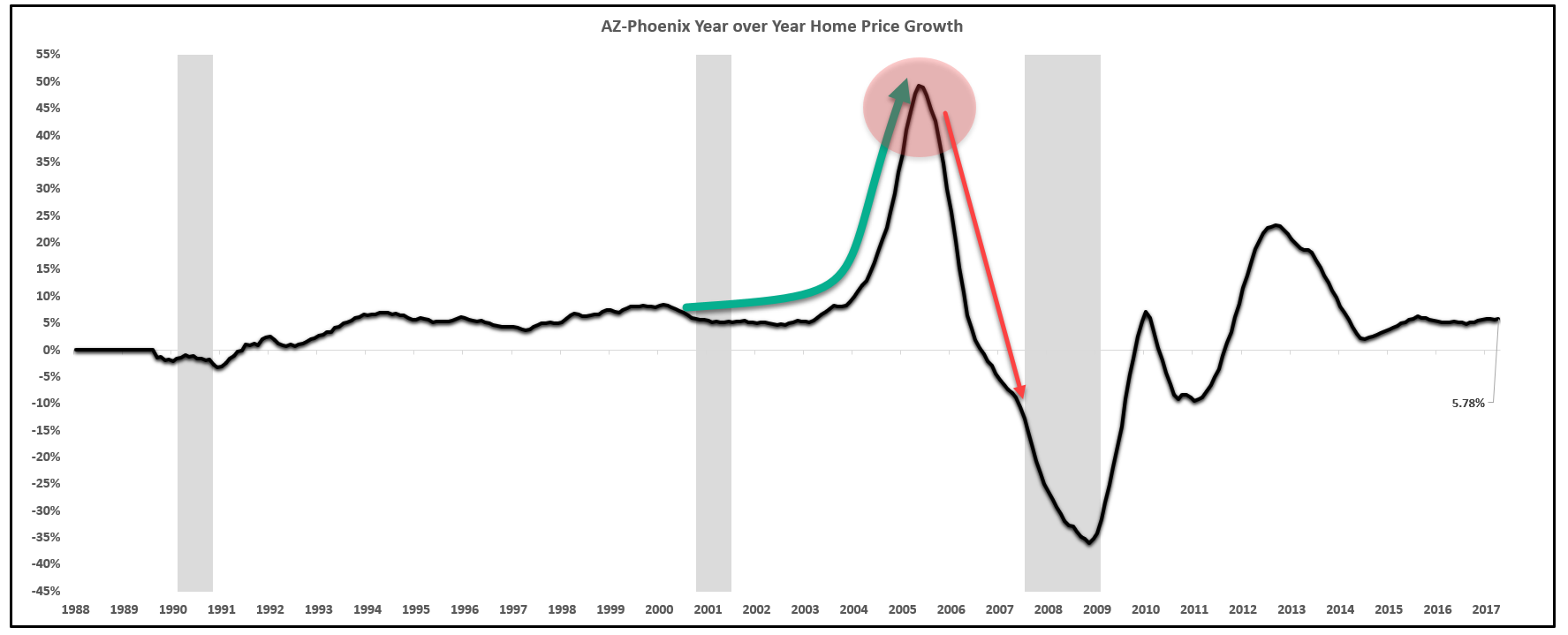

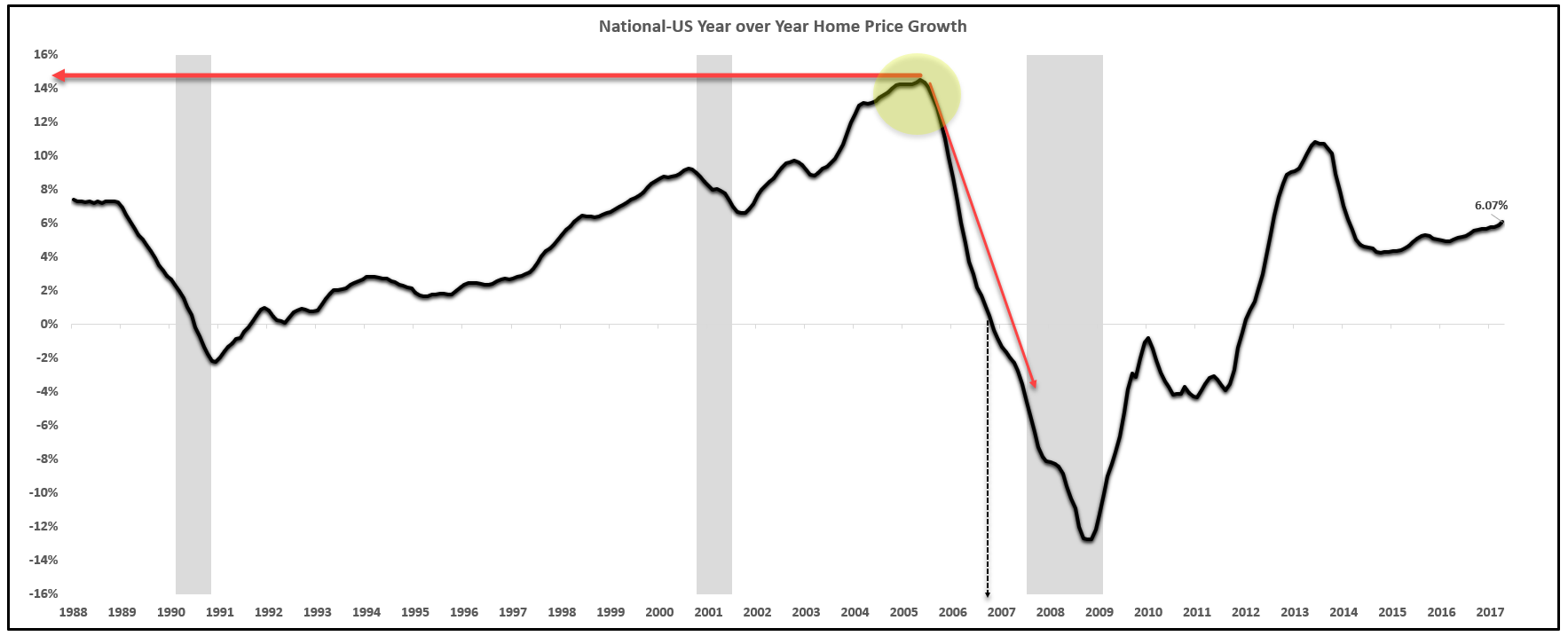

Below are three charts including home price growth in Las Vegas, Arizona, and nationally. You can see home prices growing over 50% year over year in the peak of the bubble. How this was missed is hard to imagine. Not only was the run-up clear, the decline in home prices also occurred prior to the recession as it followed the same three to four phases I outlined above.

Home Price Growth Las Vegas:

Source: S&P, Dow Jones

Source: S&P, Dow Jones

Home Price Growth Arizona:

Source: S&P, Dow Jones

Source: S&P, Dow Jones

Home Price Growth National Level:

Source: S&P, Dow Jones

Source: S&P, Dow Jones

There was a commensurate rise in home-building stocks such as Lennar (LEN), KB Home (KBH), Toll Brothers (TOL), Home Depot (HD) and D. R. Horton (DHI), which peaked in 2005, not 2007, when the meteoric rise in home price growth peaked.

Stock Price Growth of Major Housing Stocks:

Source: YCharts

Source: YCharts

The panic year of 2008 was arguably the worst in the United States history, and had it not been for unprecedented government bailouts, the economy would have been in a depression that lasted longer than the 1930s. (Some argue we have been in a depression for the bottom 90% of income earners.)

While the stock market and the financial assets that were speculated on were saved, after they crashed when debt was unavailable, the issue was not solved. In the past three crises that I mentioned, the debt was wiped out and the economy was able to reset with a clean balance sheet. After the 1930s crash, debt to GDP fell from 300% all the way down to a healthy level of just 120%. It took over 70 years to reach the same level of indebtedness that caused the great depression, and unsurprisingly, the same level of debt caused an equal-sized crash.

It took just a few years this time to surpass the level of debt that caused the 2008 crisis as we now sit with debt over 370% of GDP. It can only be assumed that since the higher the debt, the worse the crash, that the following panic year will be worse than the four preceding it.

While these occurrences of debt-induced crashes happen at irregular intervals, which is one of the challenges in forecasting the next panic year, the build-up of debt, the actions during the build-up phase and the end game/solution have all followed similar paths.

The pattern this time around is exactly similar to the past four.

Government-created incentives have fueled a debt-driven speculative rise in asset prices. The assets that have been speculated on, again, are non-cash flow generative and like the past, as long as the assets being speculated on continue to rise, all is well as the debt can be repaid with higher prices. Once the prices stop rising, and there are not higher prices nor cash flow to repay the debt that was used to gamble on the assets, the panic year will ensue - and this time, with levels of debt that are higher than any panic year in history.

Debt Is Higher Than Any Point In History

Total Public & Private Debt As A % Of GDP (Excluding "Off-Balance Sheet" Items):

Source: Federal Reserve, Bank For International Settlements, US Treasury

Total Public & Private Debt (Trillions) (Excluding "Off-Balance Sheet" Items):

Source: Federal Reserve, Bank For International Settlements, US Treasury

Below are a few examples of the assets that have been driven to record highs fueled by debt-driven speculation.

Stock Prices:

Source: YCharts

Source: YCharts

Real Estate Prices:

Source: S&P, Dow Jones

Source: S&P, Dow Jones

Bitcoin:

Source: YCharts

Source: YCharts

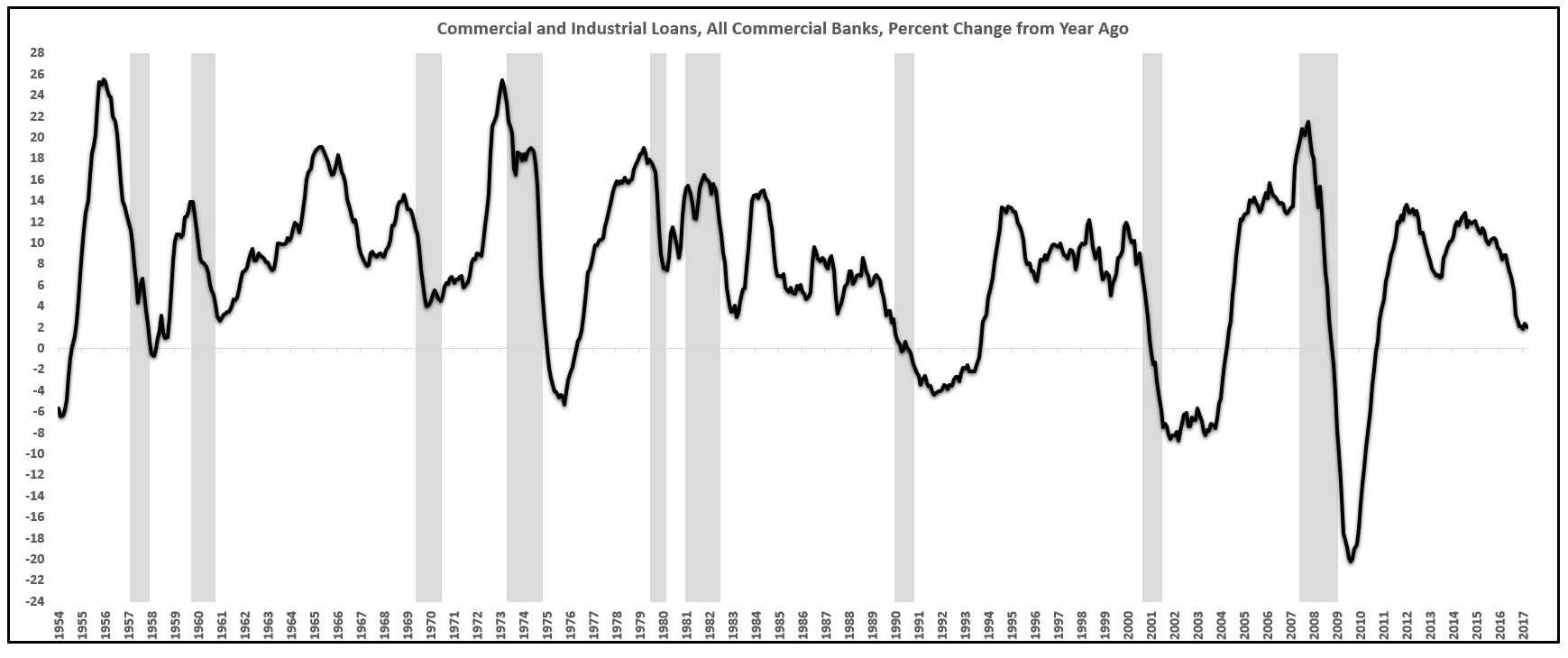

As history shows, once bank lending contracts and the ability to expand credit (debt) further in order to drive higher asset prices (multiple expansion, not fundamentally higher economics) the greater fool theory falls flat.

Of course it is impossible to predict when this occurs, but in fact, bank lending has already begun to contract in growth quite substantially as well as the growth in the money supply which indicates that credit availability is more scarce and the bang point may be closer than most people believe.

Bank Lending Growth Contracting:

Source: Federal Reserve:

Source: Federal Reserve:

Money Supply Growth Contracting:

Source: Federal Reserve

Source: Federal Reserve

Prior to 2008, the three episodes of debt-fueled panic were followed by periods of economic prosperity for many years. The difference after 2008 was that aside from the rise in asset prices, economic growth did not rise to new highs but in fact, was slower than the last cycle.

The reason we continue to have slower rates of growth is because we have not solved the problem of debt like we did in past episodes.

After the 1930s there were 70 years of prosperity in which incomes rose, economic growth was robust and the standard of living rose.

Austerity was the cause for a resulting period of prosperity. The debt level fell almost 200% as a percentage of GDP and the country was able to move forward with a clean balance sheet.

After 2008, there was no such austerity, we chose to add more debt to solve the existing debt and the result was more of the same. Slow growth, reduction in velocity, more booms and busts in asset prices driven by easy money speculation.

The best evidence today suggests that each increase in debt creates 3-5 quarters of transitory gains that give the illusion of growth. After the gains dissipate, the economy is more indebted and worse off as incomes did not rise and the standard of living did not rise but debt levels did.

We continue to choose to increase the debt after each transitory spurt in growth subsides.

Debt mutes the business cycle.

All seems well today as the asset prices have not fallen but if/when they do, there will be no cash flow to repay the record high levels of debt that have been accumulated.

When debt reaches the levels of today, you cannot grow out of debt, you cannot inflate your way out of debt and you certainly cannot increase debt to solve the problem. You cannot fix debt with more debt. Unfortunately, the latter seems to be the path we are choosing to take, with no signs of changing course.

You cannot grow your way out of the problem because debt is the reason growth is so slow to begin with. Tax cuts or any other fiscal or monetary policy may induce transitory gains but the issue of debt will actually be amplified by increased budget deficits which will add to the debt, reduce velocity of money, and create slower growth and in the end, higher levels of debt that are even more difficult to repay.

You cannot inflate your way out of debt because as inflation rises, which it will likely not do because debt is the reason inflation is so low (velocity is too weak), interest rates rise in proportion to the rise in inflation.

Interest on the debt is already in the top three most expense categories of the budget. For those who believe that inflation is a way out, if inflation rose to 20%, interest rates would rise accordingly and the debt that rolls over will now incur an interest rate of 20% and the interest payments will take up over 100% of tax receipts and there will be no money left to repay the existing debt.

The notion that you can inflate your way out of debt ignores the fact that the interest expense will rise in proportion to the rise in inflation and make the problem worse, not better.

Defaulting on the debt denies futures borrowing so that option is very poor as well.

Since you cannot grow your way out of a debt problem and you cannot inflate your way out of a debt problem, the only long-term solution to the debt burden is austerity, a solution that no one wants to hear.

Austerity is the end game.

End Game To A Debt Problem

In order to move on to a long-term period of prosperity in which incomes rise, the standard of living rises and the economy grows at a reasonable rate, you need to clean the countries balance sheet by reducing the debt burden. This is the only way to increase the velocity of money and create long-term high economic growth. To pay down the debt, you need a period of pain or austerity which most economists define as a long-term rise in the savings rate.

Sometimes this period of austerity is imposed for you, other times it is the collective decision of the country but in either case, history shows there has never been a major developed economy that has solved a debt problem without a period of austerity.

For example, many assume the United States got out of the great depression due to World War II. This is a superficial analysis and not completely true.

The real reason the US was able repair the economy was due to austerity imposed by the government.

The war had begun and our trading partners were in need of war time supplies from the United States.

Our industries boomed to fill this newfound demand and this created income and a trade surplus for the country.

You need to go one step further to understand how this created prosperity.

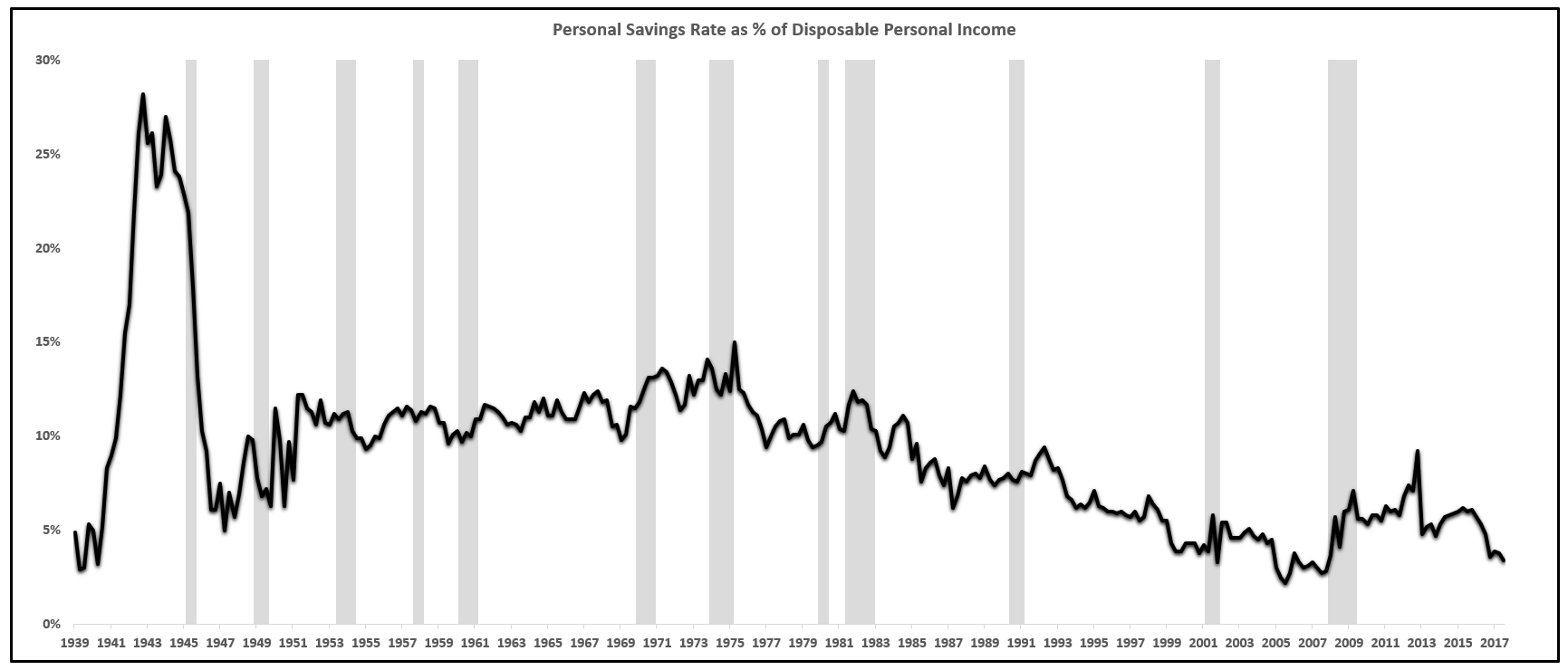

While it is true the war created a boom in exports, the US government imposed mandatory rationing, which meant that households were not allowed to spend the rise in incomes they were receiving. This caused the savings rate to soar (austerity defined as a long-term rise in the savings rate) up to 25% (currently at 3% today), and this rise in the savings rate allowed the country to pay down the debt of the 1920s and 1930s.

Savings Rate Rose Due To Imposed Austerity:

Source: BEA

Source: BEA

The ratio of debt to GDP did not trough until the savings rate rose in the 1940s. The imposed austerity and reduction in the debt down to 120% of GDP from 300% is what cleaned the balance sheet of the country and allowed us to prosper for almost 70 years.

A reduction in debt and a clean balance sheet is what is needed again today although with debt levels way higher than the 1930s, the austerity will be even more painful which is why we seem to not have the political will to solve the problem.

Why Austerity Is Essential To Fix The Economy & What Investments Will Benefit

I want to focus on the United States economy, but in order to do that, I have to address our major trading partners, Europe, Japan and China who are more indebted than the United States and face bigger challenges than the United States. This is both a blessing and a curve for the United States for reasons I will outline.

Many critics of the United States' debt burden claim that a collapse of the US dollar (UUP) is inevitable and that our debts will be repaid with worthless dollars. This is a very poor analysis of the situation as it does not take into account the global situation.

The first point to make is that currencies are valued on a relative basis. The euro and the dollar cannot both go down against each other at the same time.

The only way that all currencies can depreciate simultaneously is if they are devalued against gold (GLD), silver (SLV) or some other commodity (USO). More on this later.

Operating under the assumption that all currencies will not depreciate relative to gold for a minute, that leaves one currency to be the "winner" or the strongest relative to the others. I am referring to a long-term multi-year trends in the currencies, not monthly or yearly moves.

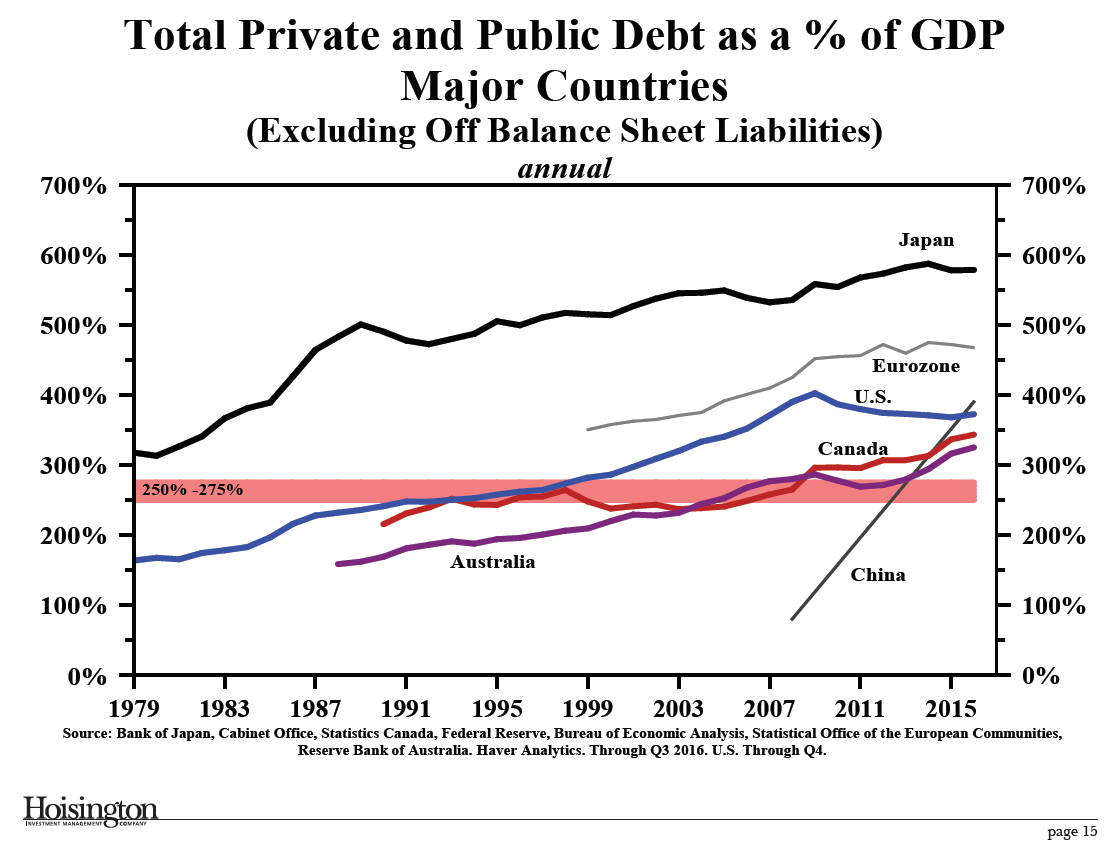

The relative indebtedness of Europe, China and Japan are significantly worse than the United States.

The United States stands at debt 370% of GDP, China at nearly 400%, Europe around 475% and Japan at almost 600%.

Country Debt To GDP Level:

Source: Hoisington, Bank of Japan, Cabinet Office, Statistics Canada, Federal Reserve, BEA, Statistical Office of the European Communities, Bank of Australia, Haver Analytics

Source: Hoisington, Bank of Japan, Cabinet Office, Statistics Canada, Federal Reserve, BEA, Statistical Office of the European Communities, Bank of Australia, Haver Analytics

If the United States cannot repay its obligations then surely countries who are more indebted cannot repay them either and will default faster should that be the case.

If the other three largest countries will by definition have to default faster than the United States, due to higher levels of debt, that serves to put a long-term bid under the US dollar.

How can Japan not default prior to the United States if they have a level of debt almost two times as great. If Japan defaults prior to the dollar, then the yen (FXY) will fall dramatically and cause a massive upward pressure on the exchange rate between the dollar and the yen.

Unless you believe that the US, the relatively least-indebted country, will default with less debt than other countries with more debt AND slower economic growth, then the long-run trend in the dollar must be higher.

This does not refer to small moves in the dollar caused by knee-jerk reactions to Federal Reserve policy but rather large multi-year trending moves in the exchange rate of the dollar against other currencies.

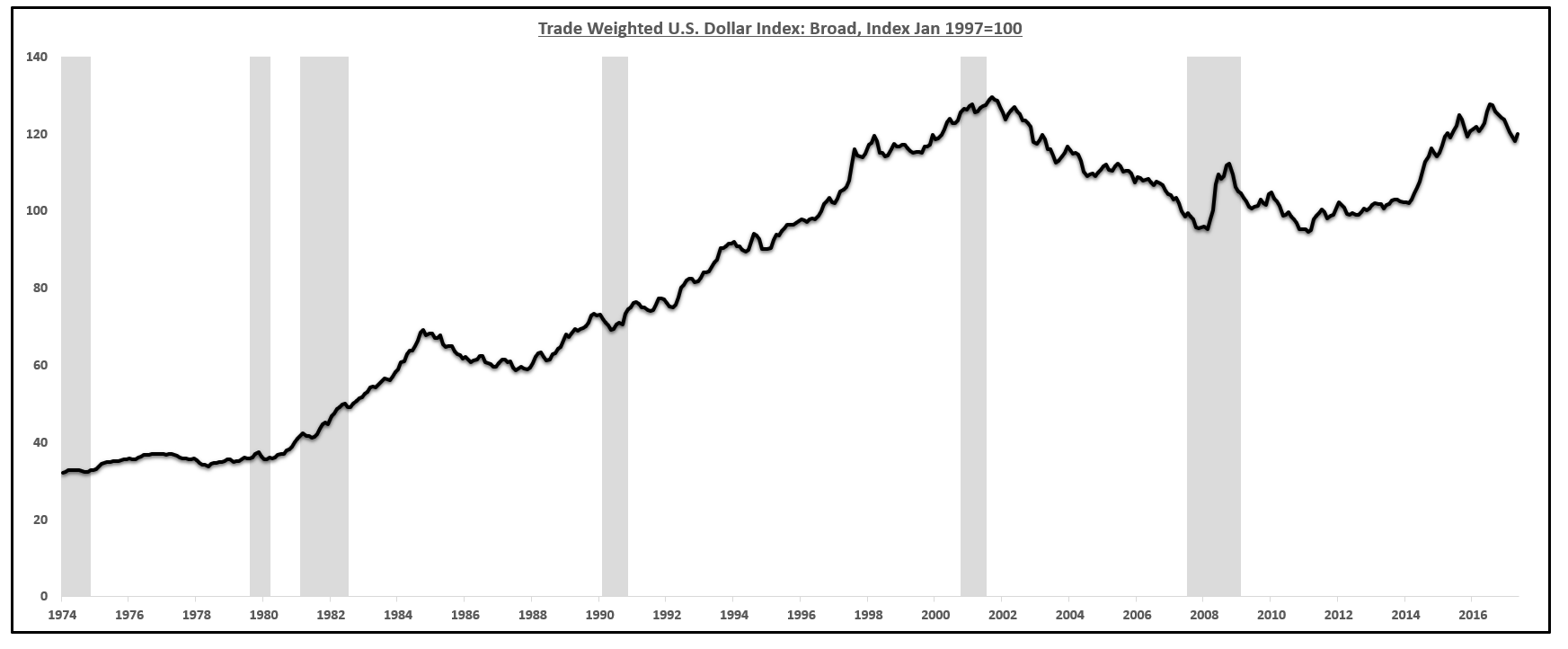

Long-Term Trend In The Dollar:

Source: Federal Reserve

Source: Federal Reserve

The long-term trend is the dollar is higher relative to other currencies. If countries that are significantly more indebted than the United States default first or continue on the path to higher levels of debt relative to the United States, there must be a long-term bid under the dollar keeping its value relative to other currencies.

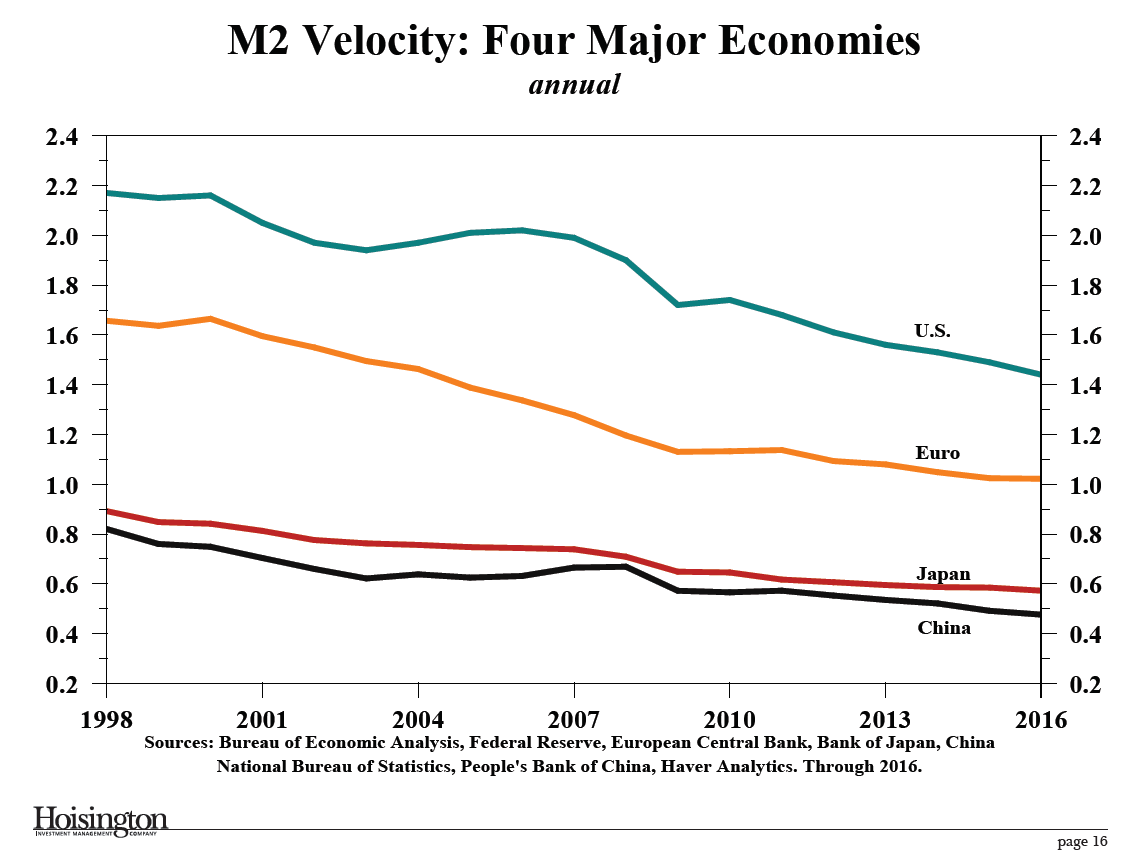

Higher levels of debt cause the velocity of money to decline, which is why the countries that I mentioned which have higher levels of debt also have lower levels of velocity, which causes lower long-term interest rates.

Velocity of Money Across Countries:

Source: Hoisington, Bank of Japan, Cabinet Office, Statistics Canada, Federal Reserve, BEA, Statistical Office of the European Communities, Bank of Australia, Haver Analytics

Source: Hoisington, Bank of Japan, Cabinet Office, Statistics Canada, Federal Reserve, BEA, Statistical Office of the European Communities, Bank of Australia, Haver Analytics

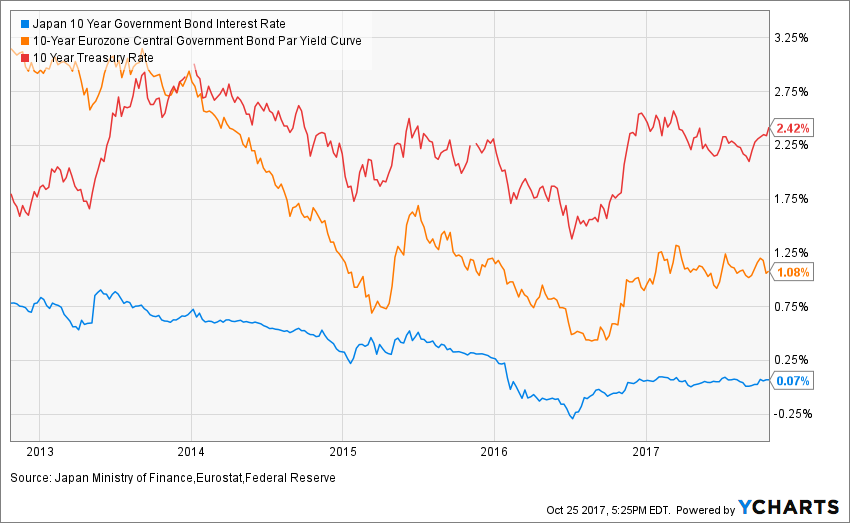

The United States, having the highest relative long-term interest rates, low on a nominal level but high relatively, since currencies trade on a relative basis, will also serve as a factor keeping a long-term bid under the dollar as foreign money will demand our higher interest rates.

Interest Rate Comparison:

Source: YCharts

Source: YCharts

The factors above, higher interest rates and low relative levels of debt, will serve to keep the value of the dollar relative to other currencies.

This, as I mentioned, is a blessing, as the risk of default for the United States essentially cannot come prior to other countries, but also a curse as higher levels of the US dollar relative to other currencies is a deflationary pressure that serves to lower economic growth and make the debt harder to repay.

I mentioned briefly the possibility of all currencies falling relative to gold or some other commodity.

This is a low probability, but it is worth mentioning.

I believe that the long-run trend will be upward for the US dollar for the reasons mentioned.

There is the possibility that no country can repay their debts and all fiat money loses its value.

In this scenario, gold will reprice to multiples of the current level (estimates are roughly $10,000 per oz) in this instance.

The value of stocks, bonds, and other assets would be worthless in this case, so the discussion around inflation hurting bonds but not stocks is an irrelevant point. The only protection against this scenario is hard assets.

In the portfolio I run in my Marketplace service, EPB Macro Research, I always have a certain allocation to gold as a protection against this scenario (very unlikely in the near future); the exact allocation changes based on market conditions, of course, is exclusive to my subscribers.

That being said, the analysis that suggests that there is a collapse of the dollar on the horizon does not take into consideration the debt of other countries that by definition, almost have to default prior to the United States and therefore keep long-term severe upward pressure on the US dollar.

A small allocation to gold protects against a total fiat currency collapse which is very unlikely, but serves as an insurance policy that is worth holding on to. I do like a small portion of gold as a long-term investment and believe it should be part of everyone's portfolio.

Austerity

Now that the probability of hyperinflation has been thoroughly reduced, the situation returns to the United States and to one of deflation as ever-increasing levels of debt will make our economic situation mirror that of our trading partners who are several years ahead of us in terms of debt, velocity, low growth, low inflation and low interest rates.

Unless we, as a country, stop the increase in debt, which we seem to have no intention of doing, the velocity of money will continue lower towards the figures seen in Europe and Japan. Lower rates of nominal growth will be the result and similar interest rates will follow. 2.4% interest rates will be a distant memory once the velocity of money in the United States falls below 1, as will 2% economic growth.

The economy is too indebted for interest rates to rise and stay up.

Monetary policy has been proven to be ineffective as the last 7 years of experiments from the Fed have raised stock prices, but have resulted in the lowest level of economic growth in decades.

Fiscal policy, in the form of tax cuts, will also have an immaterial effect.

Many will scream to look at the Reagan tax cuts as a proxy for how the new potential tax cuts will benefit the economy, but a major hole in that logic is that Reagan had a debt to GDP ratio of around 40% at the Federal level, not 107%.

Many will scream to look at the Reagan tax cuts as a proxy for how the new potential tax cuts will benefit the economy, but a major hole in that logic is that Reagan had a debt to GDP ratio of around 40% at the Federal level, not 107%.

Also, Reagan had the benefit of the best demographic mix the country has ever seen. Today, the demographic situation is materially worse as population growth has been declining as well as fertility rates.

That leaves austerity.

The problem is too large to be solved by spending alone or tax increases alone. There needs to be compromise on all sides for reasons I will outline.

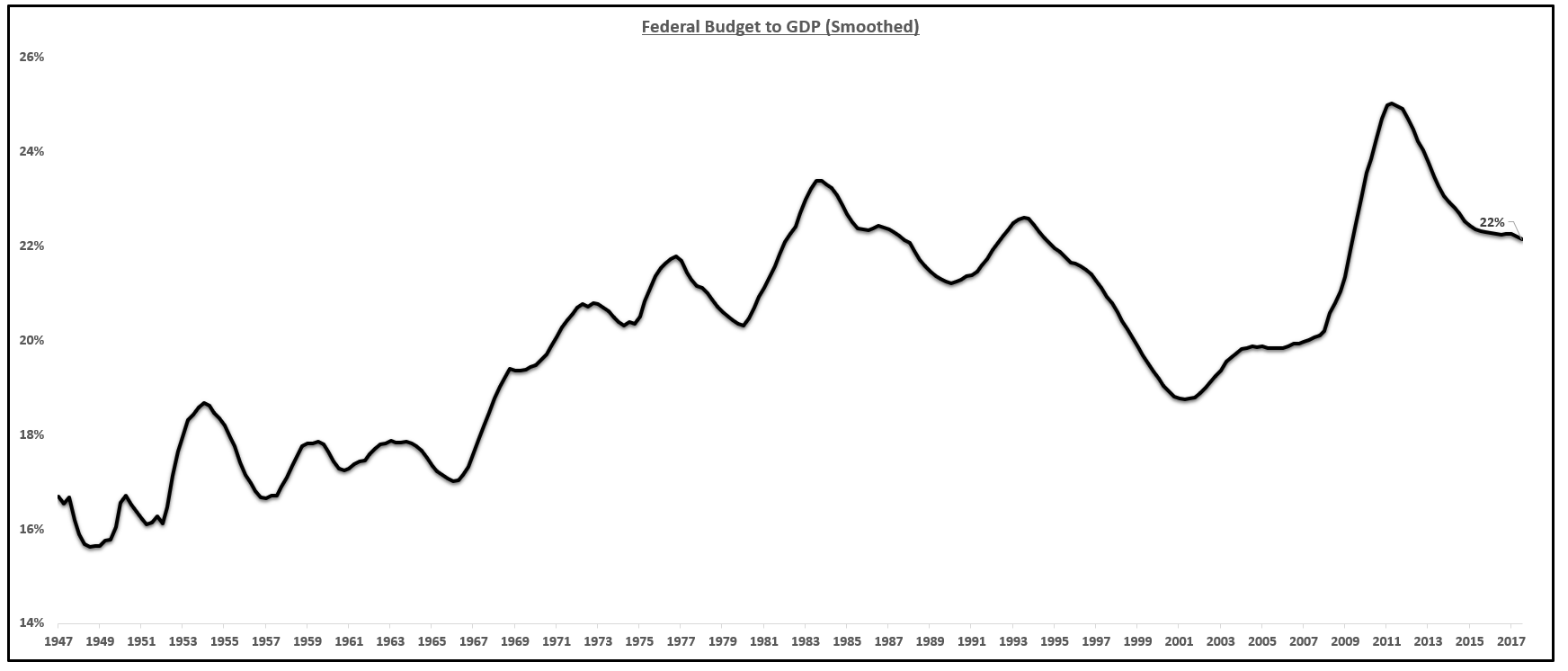

Currently, the Federal Budget is roughly 20% of GDP.

Federal Budget to GDP:

Source: BEA

Source: BEA

Without any changes to policy, due to obligations that we have promised including debt repayment, social security and Medicare the unfunded liabilities are near $100 trillion and will cause the federal budget to rise to 40% of GDP in 20 years, according to the IMF.

This does not take into account future borrowing that we are likely to incur so it is the most optimistic and conservative forecast.

In 20 years, if the nominal rate of growth averages 2% (3% currently) that means in GDP will be roughly $30 trillion.

If the budget increases from 22% to 40% of GDP, that is an 18% transfer from working households to retired households that we have promised. 18% of a $30 trillion economy is a $5.4 trillion per year increase in spending that needs to come out of the economy. Again, that is per year.

The only way to find an additional $5.4 trillion per year, is to borrow it, further adding to the debt problem and raising the interest payment expense or to tax it. That is on top of the current taxes.

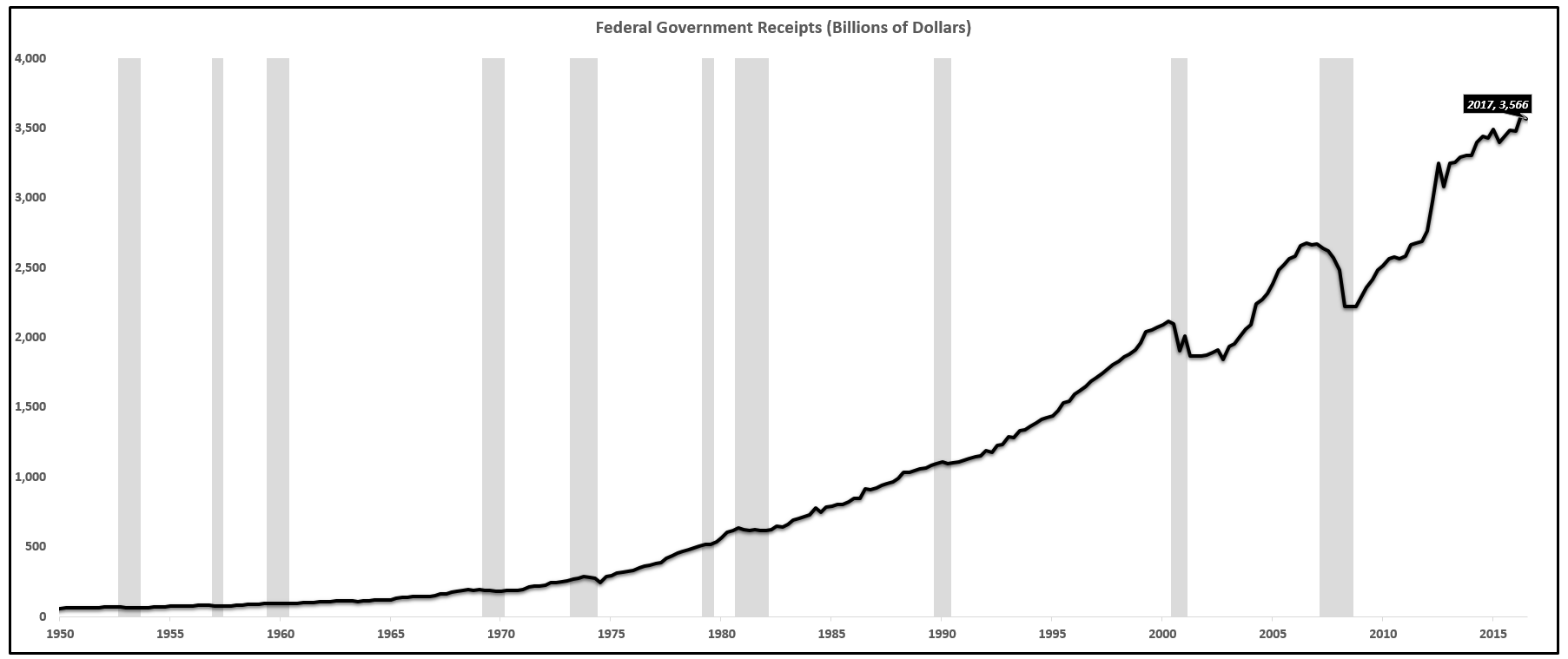

Taxes collected are only about $3.5 trillion today.

Total Taxes Collected:

Source: BEA, IRS

Source: BEA, IRS

This implies that over the next 20 years, without any additional debt (nearly impossible) that the taxes need to rise to $9 trillion in order just to keep the level of debt to GDP ratio the same at 370%, not to mention trying to reduce it.

Increasing the level of taxes over 100% is essentially impossible and would certainly grind the economy to a halt.

The only solution has to come from a combination of spending cuts, tax increases and a long-term rise in the savings rate.

The issue is that the best analysis suggests that a $1 increase in the marginal tax rate reduces economic growth by $2-3, a negative multiplier.

Reducing loopholes, of which there are currently over 3,000, does not have the same negative multiplier and is more effective.

Therefore, a reduction in spending, an increase in taxes by reducing loopholes but NOT by raising the marginal rate (in fact you can cut the marginal rate to spur growth if the loopholes are closed and the tax base rises), and a long-term rise in the savings rate are the only hope to get the economy back on track. On top of this, there would likely need to be a consumption tax. Ironically, a consumption tax and no income tax is the best way to run a prosperous economy but the days of that being the only solution are long gone; the problem is too great.

Thomas Hobbes said "income is what you give to society, consumption is what you take from society."

By taxing income, we are punishing contributions and encouraging consumption (lack of savings). A consumption tax leads to high rates of saving, a vital component to a long-term healthy economy.

There needs to be structural reform to social security and Medicare because even with the above prescription, which would be enormously painful in the short run, it is not enough to meet the obligations and debts that we have assumed.

If we do follow the above plan, short-term pain for long-term gain, we are looking at a multi-year decline in GDP.

We do not seem to have the political will to go down that path and we instead are choosing a path of increased debt on top of old debt.

By following the same path, we are going to get the same result. Students of history will understand that we have been down this road four times before and will make investments accordingly.

Long-term interest rates will fall due to increased debt, reduced velocity and lower growth/inflation will make long-term bonds (TLT) (IEF) a strong long-term investment for the capital appreciation that will come when interest rates fall to the level of Europe and Japan over the next 10 years. Of course this should be hedged with gold for the reasons outlined in the above sections.

The gain on a long-term bond from 2.5% down 1% or lower is enormous. Anyone who bought a Japanese JGB at 2% is in good shape with rates now at 0%. They are getting 2%, and have a massive appreciation on the bond.

Since we know the path that Europe and Japan took, and we have no political will to follow the above prescription but rather are following in their footsteps, we will get the same result.

The path to lower nominal growth and therefore lower interest rates is set in stone due to the increases in debt.

If we continue on the path towards the indebtedness of Europe and Japan, our economy will mirror those results. Velocity will crash which will make any fiscal or monetary policy ineffective because the increase in money supply will not circulate fast enough to spur the required growth.

The lows in long-term interest rates are nowhere near the current levels. If we continue on the path of Japan we could see 10-year yields at the same level, sub 1%.

That is likely more than 10 years away, so the current forecast, outlined in the introduction, is that the Federal Reserve is going to reverse the course of monetary policy before the end of 2018 due to severe disinflation and anemic or even recessionary levels of growth brought on by excessive debt, and that the equity market (DIA) will experience a much choppier ride due to these factors.

The Federal Reserve is likely to cut interest rates by the end of 2018 due to falling long-term rates that will cause a very flat or inverted yield curve (BND), hurting the banking sector - JPMorgan (JPM), Bank of America (BAC), Goldman Sachs (GS) - and changing investor sentiment to one of more caution and fear of a pending economic slowdown.

The result of Federal Reserve policy that created a horrible incentive of too much debt will be one of deflation, not inflation, and create lower growth, lower interest rates and a structurally weaker economy unless we are willing to address the problem. Another panic year will occur and we then have the choice to go in the opposite direction of our trading partners and get a different result or take the same path of more debt and achieve the same result. Until then, long-term bonds, hedged with a small amount of gold is, in my opinion, the best long-term investment out there today. If rates go the way of Japan over the next 10 years, that will be a tremendously profitable investment.

0 comments:

Publicar un comentario