Predicting The Direction Of The Stock Market And The U.S. Economy

by: Centaur Investments

Summary

- All major stock indexes hover near record highs, and retail investors are more optimistic than at any time since the dot-com bubble.

- Household debt balances are now $164 billion higher than the Q3 2008 peak of $12.68 trillion, while the U.S. unemployment rate stabilizes below the long-term natural rate.

- Broken legislative promises of tax cuts, healthcare, and government spending justify skepticism.

- Threats of a nuclear war between U.S. and North Korea have been shrugged off by financial markets, as the VIX declines to historic lows.

- U.S. financial markets approach a pivotal point in history where confidence can erode quickly.

- Household debt balances are now $164 billion higher than the Q3 2008 peak of $12.68 trillion, while the U.S. unemployment rate stabilizes below the long-term natural rate.

- Broken legislative promises of tax cuts, healthcare, and government spending justify skepticism.

- Threats of a nuclear war between U.S. and North Korea have been shrugged off by financial markets, as the VIX declines to historic lows.

- U.S. financial markets approach a pivotal point in history where confidence can erode quickly.

In November 2016, Centaur Investments published a series of market outlook articles under the attention-grabbing title of “Trumped-Up Economics.” The article series was more of an economic outlook rather than an assessment of the Trump Administration. In the article series, the reader was briefed on U.S. economic history, recent political and macroeconomic developments, and concluded with a prediction of the future performance of individual market sectors. As goes with most market predictions, the warnings presented in the article series were mostly ignored by the market, which continued trend higher. Yet somehow, the points laid out in these articles are quite still relevant. This article will recap those important points and, once again, attempt to project how the market is going to perform.

As the third quarter approaches, and the calendar year comes to a close, the market outlook is still highly uncertain. The American public has yet to see realistic public policy reach the floor for debate in Washington. Promises of legislative action to improve healthcare, infrastructure, and tax code have gone unfulfilled. The legislative attempts that were made took place after being rushed through impossible deadlines. So far, the legislative process has consisted of putting documents together in a matter of weeks with little research or consideration given.

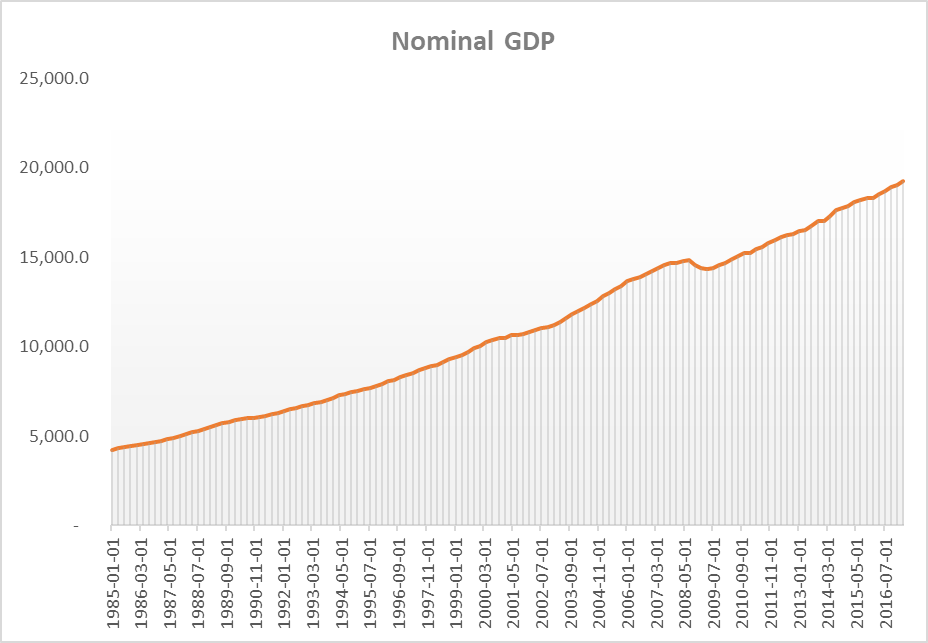

When thinking about the current political environment, it becomes evident that U.S. financial markets have performed well largely because of decade-long efforts to spur economic activity in the post financial crisis era. President Trump has been extremely fortunate to walk into the oval office just as corporate earnings grew moderately, employment continued to expand robustly, and the nation’s gross domestic product maintained its positive trajectory.

When thinking about the current political environment, it becomes evident that U.S. financial markets have performed well largely because of decade-long efforts to spur economic activity in the post financial crisis era. President Trump has been extremely fortunate to walk into the oval office just as corporate earnings grew moderately, employment continued to expand robustly, and the nation’s gross domestic product maintained its positive trajectory.

(Source: Bureau of Economic Analysis & St. Louis Fed, chained 2009 USD)

(Source: Bureau of Economic Analysis & St. Louis Fed, chained 2009 USD)But, obviously, this economic activity is not attributable to the Trump Administration, rather directly attributable to the collective efforts of market participants; hard-working individuals and businesses.

It goes without saying, if the bull market is to continue, it will continue to be driven by these economic forces. If the market stalls or pulls back, it will be due to the ongoing geopolitical climate or a threat of war.

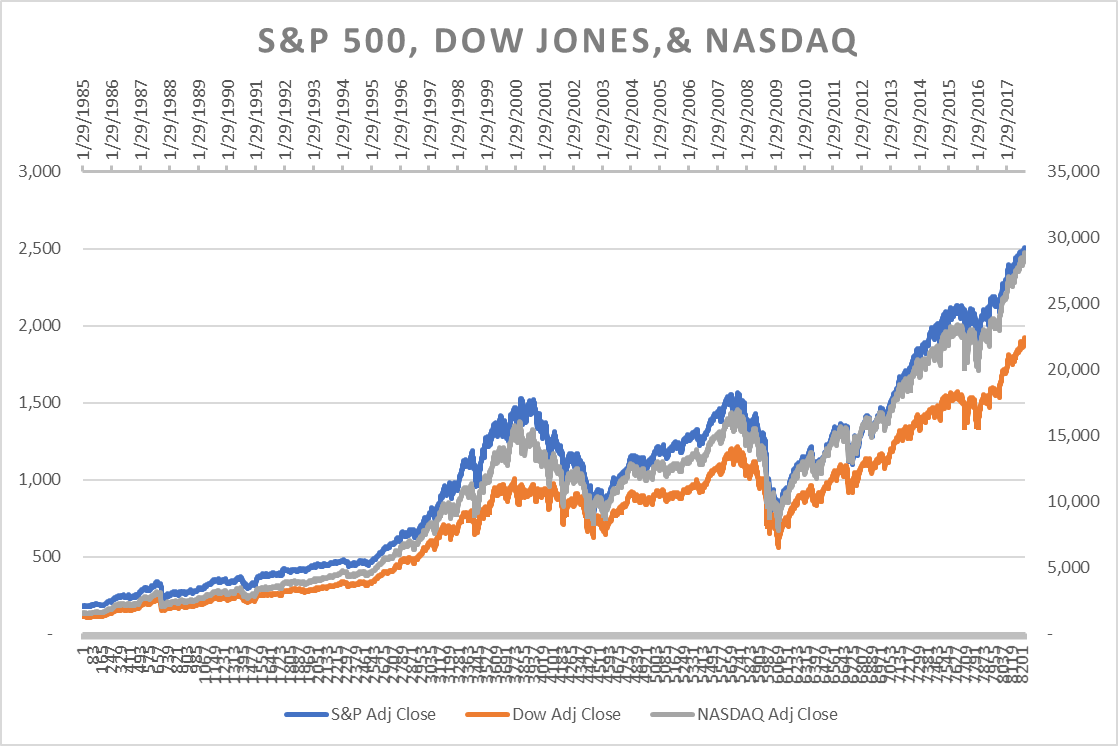

Looking at where the U.S. economy stands today, the market outlook appears promising. In more recent measures of business and consumer confidence, optimism is still at the highest level seen in years. Both inflation and interest rates remain near the decade lows. The level of confidence has continued to spill over into financial markets. Per The Wall Street Journal, retail investors are “more optimistic than at any time since the dot-com bubble.” SPDR Dow Jones Industrial Average ETF (DIA) and SPDR S&P 500 Trust ETF (SPY) are two ETFs closely tracking the Dow Jones and S&P 500 indexes, respectively. The PowerShares QQQ Trust ETF (QQQ) is one of the more popular ETF names for tracking the Nasdaq 100. The performance of these three ETFs is indicative of optimism translating to investor euphoria, as reflected in the next two graphs.

In recent trading sessions, all three major U.S. stock market indices closed near record highs…

In recent trading sessions, all three major U.S. stock market indices closed near record highs…

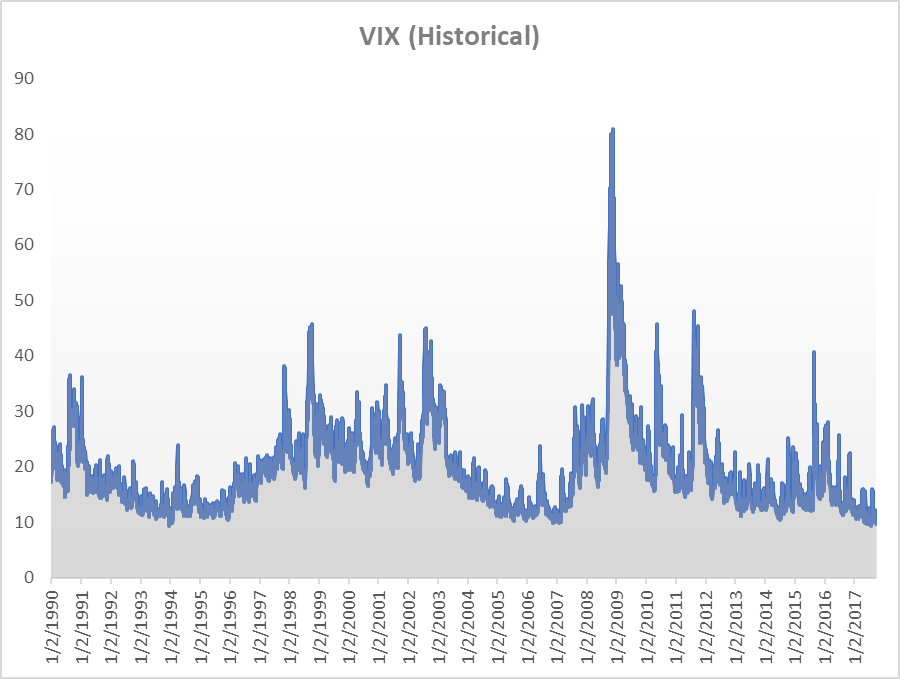

…and the Chicago Board of Options Exchange ((NASDAQ:CBOE)) Volatility Index (VIX) declined to historical lows.

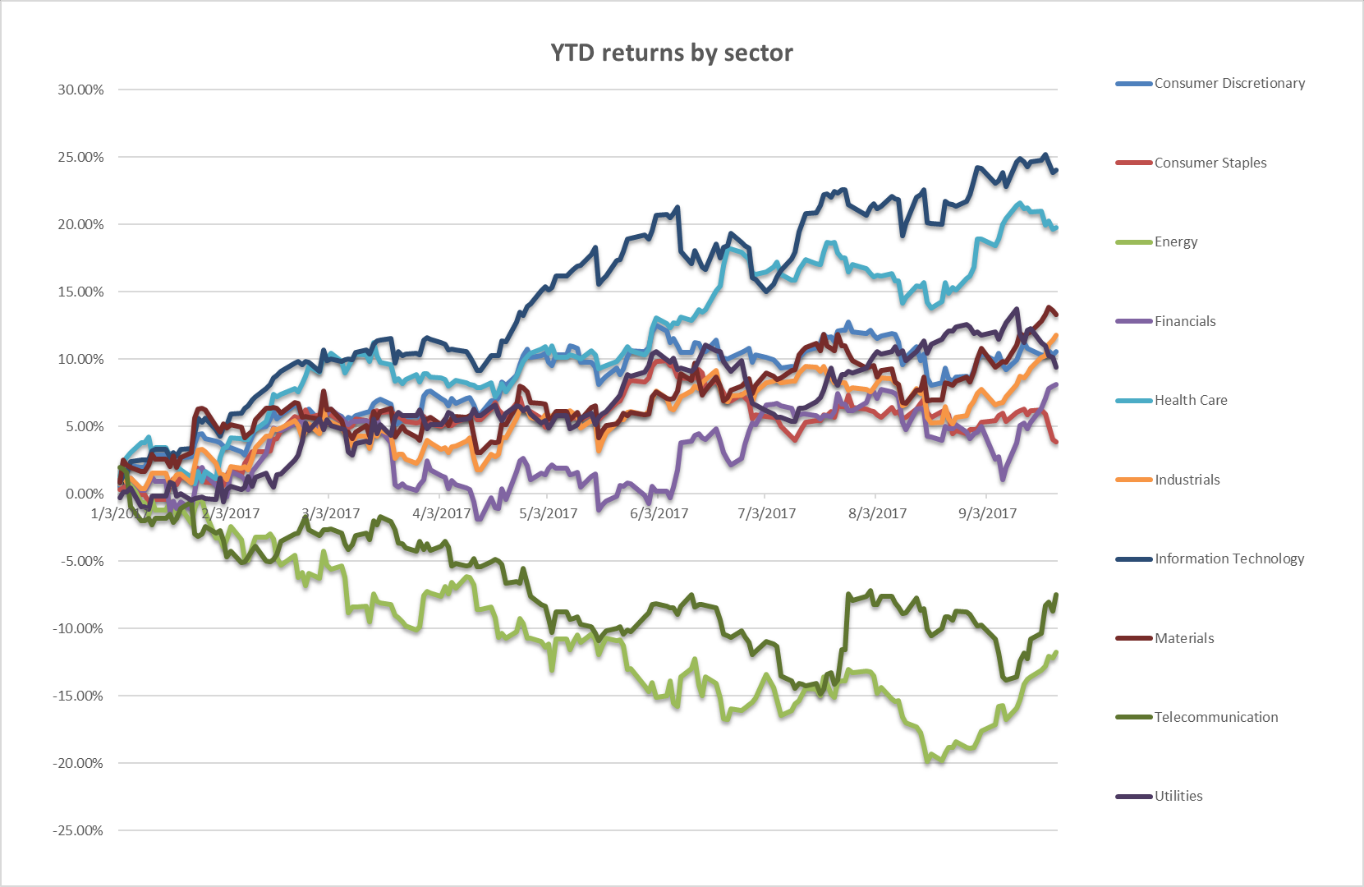

Shorting the VIX has turned out to be one of the most profitable trades of the year. In order to gauge where this market is heading, let us recap individual sector performance while focusing more on the lagging sectors. In the first half of this year, lower oil prices continued to hit corporate earnings, causing energy shares to stumble for most of the year. Recently, efforts from Oil Producing Economic Countries (OPEC) to curb production, along with an unexpected number of tropical storms, managed to elevate energy prices higher. As you will see in the next chart, energy sector returns have started to make a sharp turn upward.

Conversely, price deflation in the telecommunications sector held company share prices down, as competition intensified among carriers. Mobile phone and data plan prices have declined aggressively this year. Additionally, growth has also plateaued in automobile manufacturing volumes and dealership sales. Despite declining new automobile sales and used automobile prices, shares of auto and subprime lenders have shown resilience, advancing right along with the financial sector. See the sector breakdown in the next image.

Per Bloomberg, both Energy and Telecom have been this year’s worst-performing sectors.

Per Bloomberg, both Energy and Telecom have been this year’s worst-performing sectors.

Evident from the illustration above, Energy and Telecom are now racing to catch up with the rest of the market. From a price-to-earnings valuation, the Energy sector appears overvalued. However, if oil prices continue to rise, earnings growth should offset this measure. The upward trend in Telecom on the other hand is questionable. The decline in mobile phone and data plans will continue to put downward pressure on top-line growth among carriers. Recently, disappointing news about the new iPhone’s sales forecast caused shares of Apple Inc. (OTC:APPL) to pull back some. This may have some effect on carriers looking forward to a holiday sales boost from the new device. From a value investor perspective, AT&T Inc. (T) and Verizon Communications Inc. (VZ) offer attractive dividends, and it is unlikely that consumers will ever put their mobile phones away or forgo upgrading to new devices.

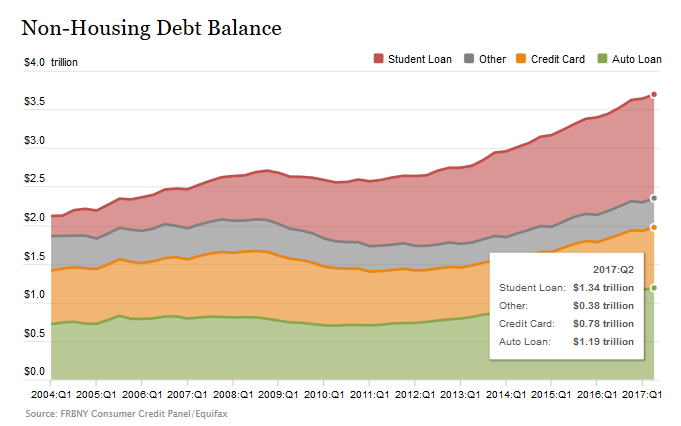

Will Peaking Household Debt Spark A Fire Sale?

Moving now to the economic indicators, let’s start with household debt, which has continued to grow to record levels. In August, the New York Fed published the “Quarterly Report on Household Debt and Credit,” for the second quarter. The report noted that:

“Aggregate household debt balances increased in the second quarter of 2017, for the 12th consecutive quarter, and are now $164 billion higher than the previous (2008Q3) peak of $12.68 trillion. As of June 30, 2017, total household indebtedness was $12.84 trillion, a $114 billion (0.9%) increase from the first quarter of 2017. Overall household debt is now 15.1% above the 20 13Q2 trough.”

There are a few interesting takeaways from this report, mostly regarding the non-housing debt balance, which still appears to be reaching a peak. During the second quarter of the year, household credit card balances grew by more than enough to offset the first quarter declines.

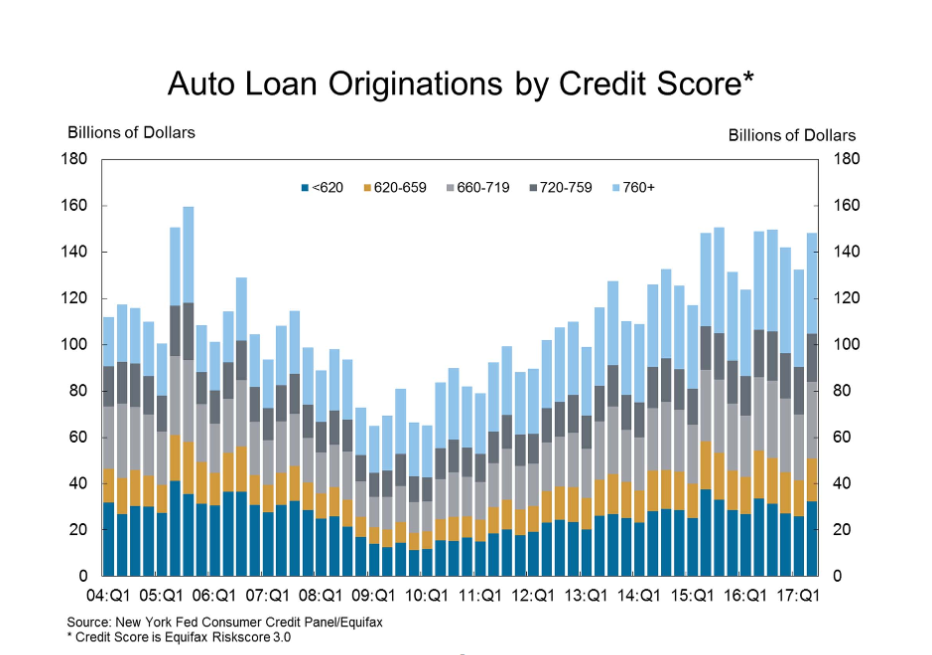

Further, the expansion in subprime auto loan origination was the highest observed in the last four quarters.

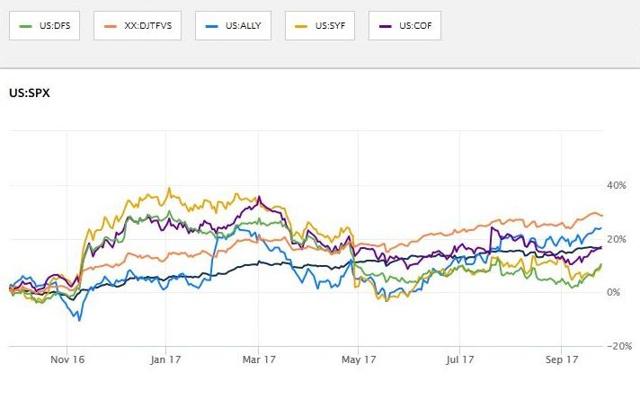

When you look at data from auto lenders, the measure for tightening standards implies that some lenders may be starting to loosen up lending standards again. It is not certain if this loosening in lending standards is due to tepid demand for new autos, increased lender competition, or because perhaps lenders perceive that loan default risks have receded. This last comment is appealing because in the most recent loan data from both the New York Fed and lenders themselves, loan and credit card delinquencies continue to rise. Even with all this publicly available insight, the market capitalization's of financial services companies have continued to rise. Lenders Ally Financial Inc. (ALLY) and Santander Consumer USA (SC) have reached 52-week highs, though some lenders like Capital One Financial (COF), Discover Financial Services (DFS), and Synchrony Financial (SYF), were mostly flat year to date.

Nevertheless, market pricing of this industry continues to appear inefficient.

S&P 500 Year-To-Date Returns Vs. ALLY, SYF, COF, and DFS

(Source: The Wall Street Journal)

(Source: The Wall Street Journal)Conclusions from Inflation, Unemployment, and Interest Rate

Will U.S. equities continue to rise and the VIX continue to trend lower, or are stocks overvalued? It is the writer’s belief that the economy is still about two or three years away from the next recession. A major crash in stock prices is likely also years away, but a correction may be overdue. The economic indicators in this concluding section support the view that a recession is still years away.

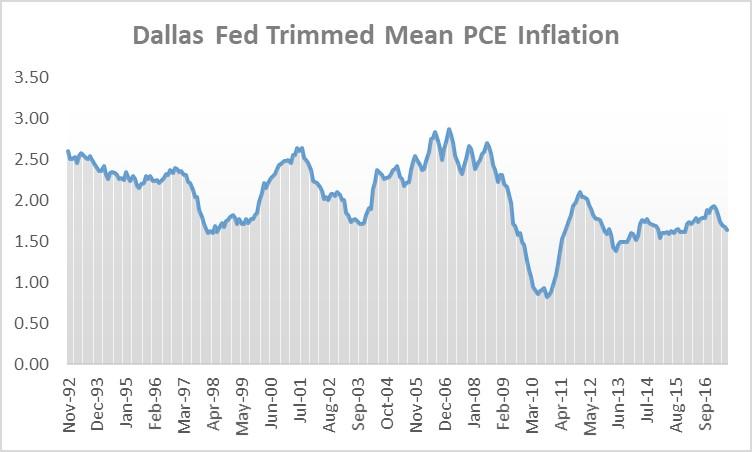

The Federal Reserve’s Open Market Committee (FOMC) plans to continue its course towards interest rate normalization despite the sluggish rate of inflation. The image above illustrates the Dallas Federal Reserve Bank’s Trimmed Mean PCE Inflation. This measure is presented instead of Consumer Price Index ((NYSEARCA:CPI)) or Core-CPI, because it filters out singularities such as a cyclical decline in energy, mobile phone plan, or pharmaceutical prices.

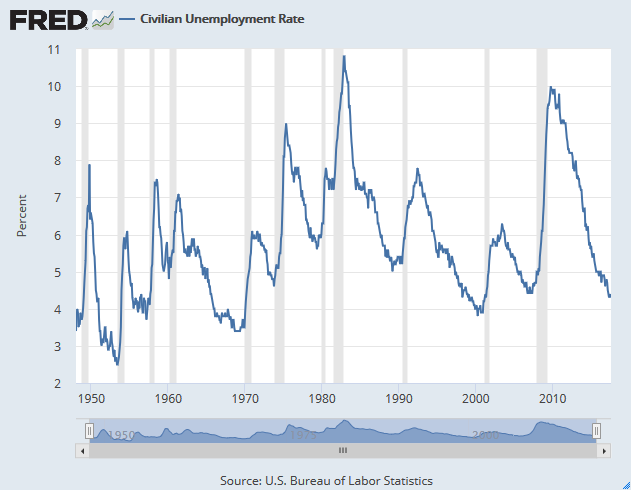

Ideally, this would be a strong indicator if inflation were becoming a threat to the economy. As you can see from the chart, there is no imminent threat observed. The Federal Reserve Board has projected for several years now that inflation would increase dramatically. The Fed’s projections have served as a base argument for raising interest rates in the past. While inflation measures may not be indicating any immediate threats, the current unemployment rate (4.4%) has stabilized below the long-term natural rate (5.8%) for over a full year now. This is one measure that may likely start to reverse in the near term. Take a look at the historical unemployment rate data in the image below.

While the current measure of inflation may not justify the Fed’s interest rate decisions, financial market performance and unemployment do. Additionally, if you observe inflation and unemployment data in close detail, there are usually two or three years of flat activity before a trend reversal becomes apparent.

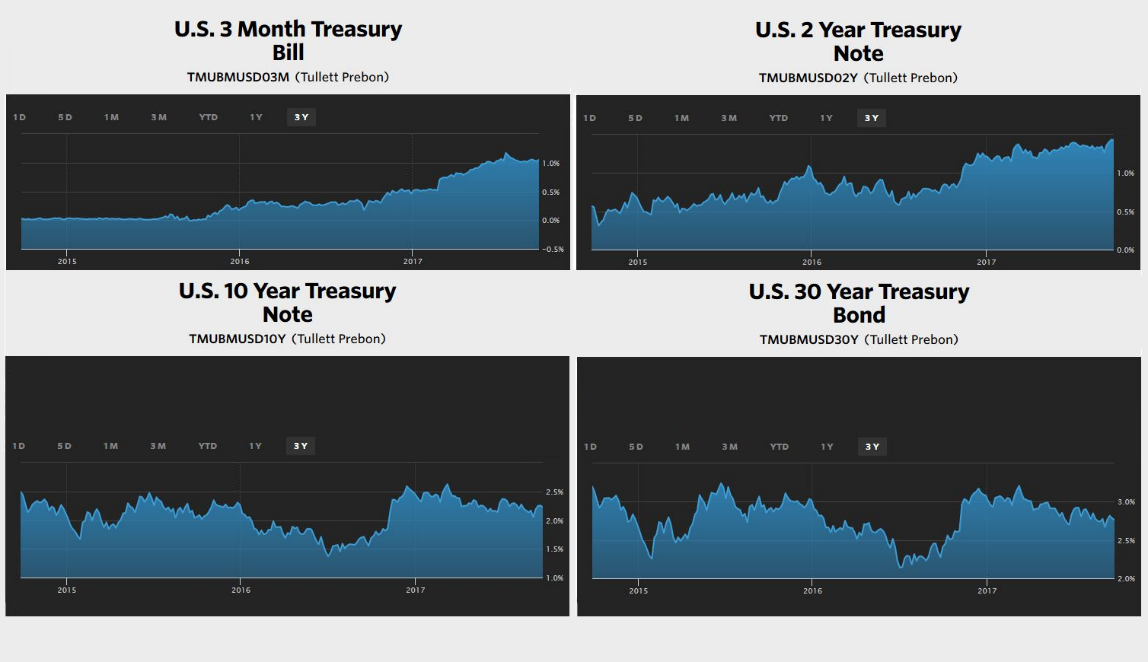

Studying the U.S. treasury yield curves can also help grasp a little more of what market participants see on the horizon. Near-term treasury yields have followed Federal Reserve’s interest rate decisions closely. On the other hand, treasuries with long-term maturities show strange behavior as geopolitical and economic risks are priced in. This observation further supports the idea that while the market may continue to outperform in the near term, the economy has only a couple more years of growth ahead.

The main conclusion to draw from this article is that investors should be cautious moving forward.

The list of uncertainties felt at this time last year are still the same today. There are plenty of reasons to be skeptical about legislative promises of tax cuts or government spending. In addition, the impact that these policies will have on the economy is also uncertain. There may be inflation or there may be a prolonged period of growth. Also, keep in mind that the Federal debt ceiling has only been temporarily increased through December. Expect for this debate to resurface in the not so distant future. Regulation of industries such as healthcare and pharmaceuticals has been clouded by infighting between political parties. Finally, there is this looming threat of war with North Korea.

U.S. financial markets are approaching a pivot point in history where confidence can erode quickly. The best thing to do here is to only add investments which have a considerable margin of safety. In the event that the market does pull back, the worst thing to do is panic sell. History shows that portfolios are capable of recovering from a correction rather quickly. Lastly, in a market environment where institutional investors start to underweight cash, doing the opposite is probably a safer bet. When closing a position whether for gain or loss, the cash collected may be far more useful when markets fluctuate, rather than immediately adding a new name to the portfolio at current valuations.

0 comments:

Publicar un comentario