Imaginative reform is vital for the eurozone to thrive

Another shock could be a disaster so the bloc must grasp the chance to find solutions

by Martin Wolf

The eurozone has survived the twin shocks of the global financial crisis of 2007-09 and its own crisis of 2010-12. It is enjoying a good recovery. That is no justification for complacency, however: the eurozone’s real output per head has suffered a lost decade. The recovery is, rather, an opportunity for reforms, at both national and eurozone level. The question is which reforms to choose.

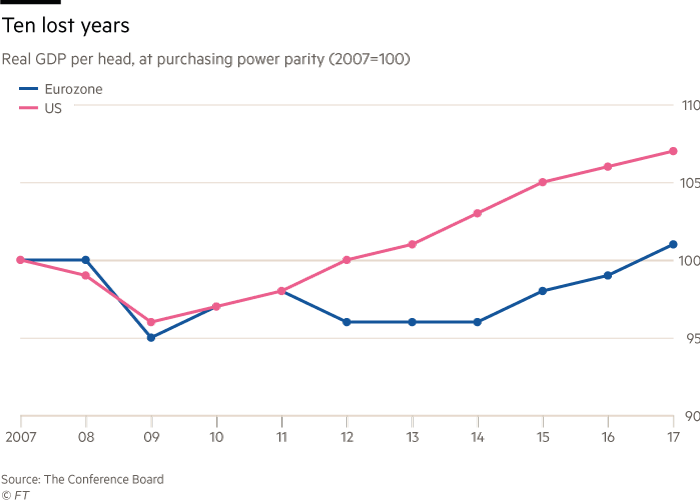

This year, real gross domestic product per head in the eurozone will finally surpass its 2007 level. Since 2013, eurozone output per head has been rising at much the same rate as in the US. The main explanation for this turnround, beyond the normal cyclical forces, has been the determination of the European Central Bank, under Mario Draghi, to do its job properly. (See charts.)

A decisive moment was Mr Draghi’s remark, in July 2012, a moment of crisis in sovereign debt markets, that: “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.” He was right. The announcement of the ECB’s “Outright Monetary Transactions” programme in August 2012 turned his promise into a policy. That shifted market opinion and lowered elevated yields on Italian and Spanish sovereign bonds. The ECB slashed interest rates and, in 2015, also launched its asset purchase programme.

Other steps have included the creation of the European Financial Stability Facility and its permanent successor, the European Stability Mechanism; programmes of support for crisis-hit countries, four of which — those for Cyprus, Ireland, Portugal and Spain — have now concluded successfully; the determination of crisis-hit countries to do what was required to stay in the eurozone; the creation of the Single Supervisory Mechanism for banks; and steps towards a banking and capital markets union. Whatever the mistakes made in creating and running the eurozone, members have shown themselves far more determined to keep it afloat than outsiders, notably in the UK and US, expected.

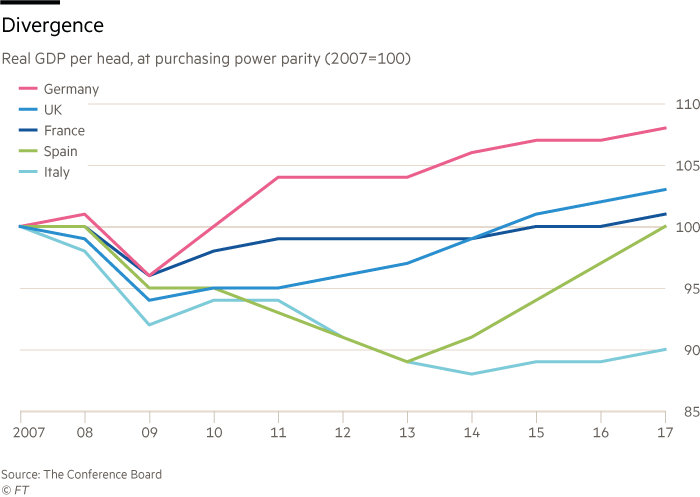

Yet challenges remain. In its most recent analysis of the eurozone, the International Monetary Fund notes that: “The crisis of the years 2007-08 marked the end of the convergence trend and the start of a divergence trend, which is only slowly being corrected.” True, some crisis-hit countries have shown dramatic recoveries, in particular Ireland. The real GDP per head of Portugal and Spain is also back where it was in 2007. Yet Germany’s has risen 20 per cent relative to that of Italy over the past decade. Greek real GDP per head is still more than 20 per cent lower than it was in 2007. Joblessness also remains elevated in Greece, Spain and, to a lesser degree, Italy.

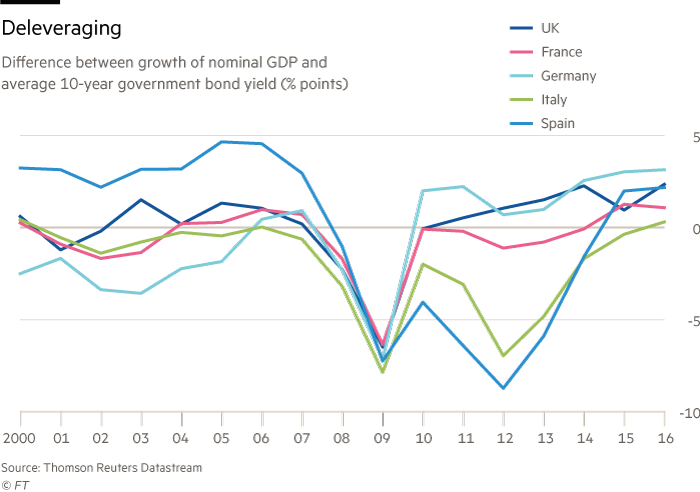

Public and private indebtedness also remains high in many countries. It is helpful therefore that the growth of nominal GDP is now above the yield on government bonds, even in Italy. Partly because of the debt overhangs, but also because the patience of the public has frayed and the room for policy manoeuvre is limited, another shock could be a disaster. This recovery must endure.

So the ECB must not tighten prematurely. After all, core consumer price inflation has been below 2 per cent since 2008. Fiscal policy should also be used wherever there is room, notably in Germany. The weaker economies must also push ahead vigorously with pro-growth and pro-employment reforms.

What, then, of the eurozone reforms? I doubt the wisdom and feasibility of Emmanuel Macron’s proposals, particularly his ideas for substantially enhanced fiscal integration. The results of the German election must also make big moves towards this far harder. The banking union does need a fiscal back-up for deposit insurance. But that may be as far as fiscal integration can go.

Adam Lerrick of the American Enterprise Institute has suggested a scheme for mitigating the impact of asymmetric fiscal shocks, without ECB support and without ongoing fiscal transfers. In a crisis, yields on government bonds of vulnerable countries rise relative to the stronger ones. According to Mr Lerrick, at the peak of the eurozone crisis, in 2012, the unexpected increase in relative interest rates cost Spain and Italy more than €5bn per annum combined. Over a seven-year average maturity, the impact reached more than €35bn.

If a part of the gains of the strong were transferred temporarily to the weak, this impact would be mitigated. Under Mr Lerrick’s proposal: “Members that receive an unexpected decrease in relative financing costs will contribute 50 per cent of their gain into a Eurozone Financing Cost Stabilisation Account.” These funds would go to members that have an unexpected increase in relative financing costs, to cover 50 per cent of their loss. Transfers would halt once relative yields stabilised and would be paid back as they reversed. Countries would only be eligible if they stuck to the fiscal rules.

This plan would not require a new treaty, would not generate ongoing transfers and would not socialise credit risks. But it would be a gesture of solidarity. It would also reduce the need for the ECB’s outright monetary transactions. Politically, therefore, this idea might be attractive to Germans, while strengthening the solidarity that others desire. This is the sort of imaginative idea that the eurozone should be looking at. The eurozone will never be a normal fiscal federation. It is necessary to invent alternatives.

It is vital that the eurozone does not merely survive, as it has, but thrives, economically and so politically. So the period of recovery is an opportunity for members to push ahead with reforms, both individually and collectively. If they fail, still worse crises might arrive.

0 comments:

Publicar un comentario