China state groups enjoy profit revival amid commodity boom

Economists warn the temporary boom leaves structural problems unaddressed

by: Gabriel Wildau in Shanghái

.

China's buoyant property market has fuelled the country's unexpectedly strong economic growth this year and boosted construction activity © Reuters

Despite talk of a “zombie economy”, China’s state-owned enterprises have enjoyed a sharp rebound in profits this year, driven by resurgent commodity prices amid government-enforced capacity cuts.

But economists worry that the revival of groups that once relied on state-directed loans and subsidies for life-support despite persistent operating losses may be unsustainable, and threatens to breed complacency about the need to reform SOEs.

A buoyant property market has fuelled China’s unexpectedly strong economic growth this year and boosted construction activity. Heavy fiscal spending on infrastructure by Chinese local governments has likewise heightened demand for basic commodities such as coal and metals — sectors dominated by state groups.

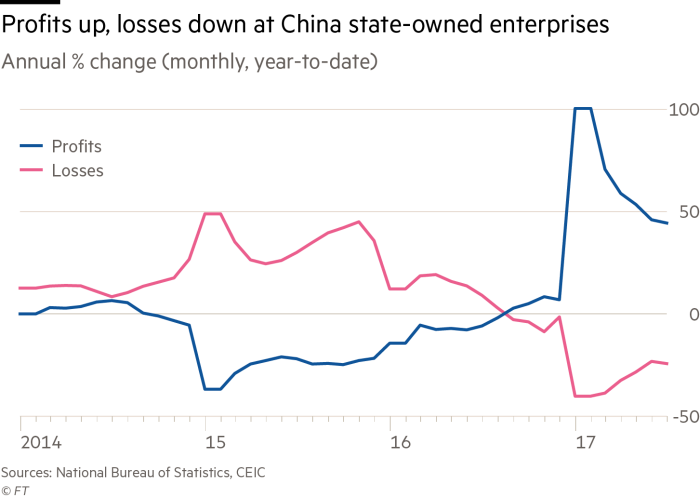

Profits at industrial SOEs surged 42 per cent year on year in the first seven months of 2017, following a meagre 3 per cent gain for all of last year and a 21 per cent drop in 2015, according to government data. Meanwhile, among lossmaking industrial SOEs, the size of losses have declined by a quarter.

“The improvement in profits is striking, especially for upstream sectors,” said Xu Gao, chief economist at Everbright Securities in Beijing. “But this improvement reflects cyclical strength of the economy. The structural issues really haven’t been solved.”

Stronger demand has also combined with tighter supply amid state planners’ efforts to shutter excess production capacity, especially outdated factories that produce heavy pollution.

In a recent commentary, China’s official Xinhua news agency lauded the improved performance of SOEs and credited ongoing reform efforts.

“These changes not only prove that reforms are on the right track but also stiffens our determination to keep nibbling at the bone and wade into the deep water.”

But there are reasons to doubt that SOEs can maintain their strong performance. Growth of property prices and investment are slowing, indicating that construction demand will soon follow.

A top legislator warned last month that the economy was overly dependent on real estate, and big cities are tightening mortgage and purchase restrictions to control runaway prices.

Some analysts also worry that apparent success will weaken policymakers’ resolve to push ahead with politically sensitive efforts to shutter state factories, which can lead to job losses and lower tax revenues.

“I doubt the government will pre-emptively close SOEs. It’s difficult to define zombie enterprises, so if SOEs become profitable now — even if it’s just because of commodity prices — then incentives to shut them down will be much weaker,” said Shuang Ding, head of greater China economic research at Standard Chartered in Hong Kong.

But optimists say the early success of capacity and production cuts in raising prices and boosting SOE profits adds to momentum for reform. At a key policy meeting in July, President Xi Jinping said cutting SOE leverage was a top priority.

They also note that so far, capacity cuts and factory closures have not led to mass unemployment or social unrest.

Jianguang Shen, chief economist at Mizuho Securities Asia, credits the combination of a strong job market and fiscal subsidies to laid-off workers. He expects SOE reform efforts to accelerate following the Communist party’s five-yearly leadership transition next month.

“The top leadership has made it clear that financial vulnerabilities and debt accumulation is the biggest risk. I think they are at the stage where they believe it’s finally time to tackle this issue,” he said. “I think after the leadership change, next year will be the beginning of the deleveraging cycle.”

0 comments:

Publicar un comentario