Why The Next Recession May Come As A Massive Surprise

by: Daniel Carter

- The U.S. yield curve has been used as a reliable recession indicator for decades.

- Because the Federal Reserve adopted a policy similar to the Bank of Japan, the U.S. yield curve may have lost its predictive power.

- If the U.S. yield curve does not invert in this economic cycle, the next recession will catch many investors off guard.

- Now is a decent time to be long U.S. Treasuries.

- Because the Federal Reserve adopted a policy similar to the Bank of Japan, the U.S. yield curve may have lost its predictive power.

- If the U.S. yield curve does not invert in this economic cycle, the next recession will catch many investors off guard.

- Now is a decent time to be long U.S. Treasuries.

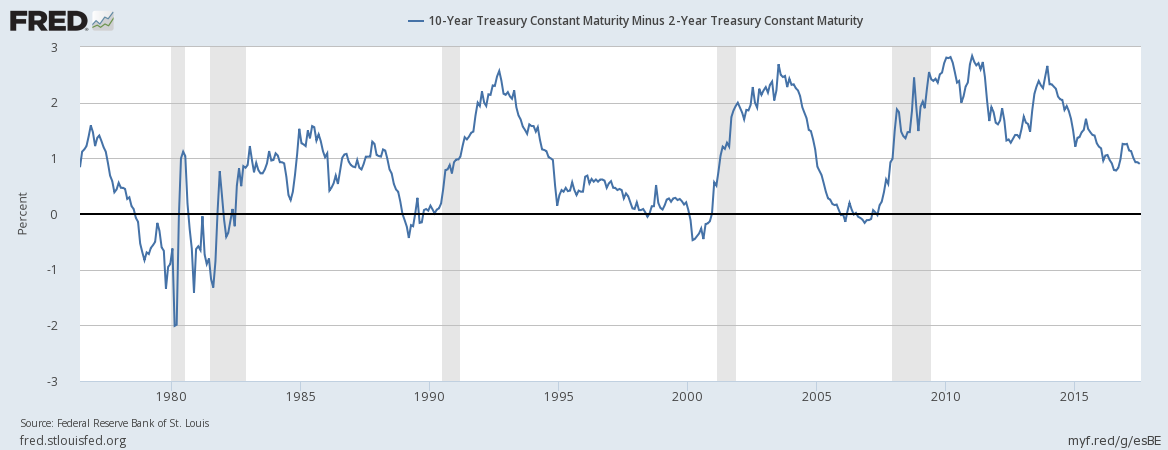

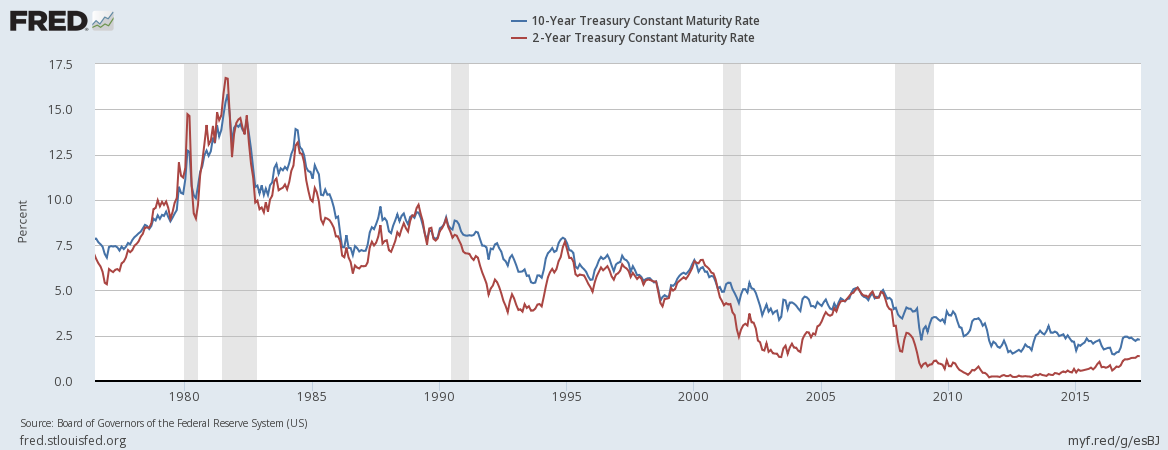

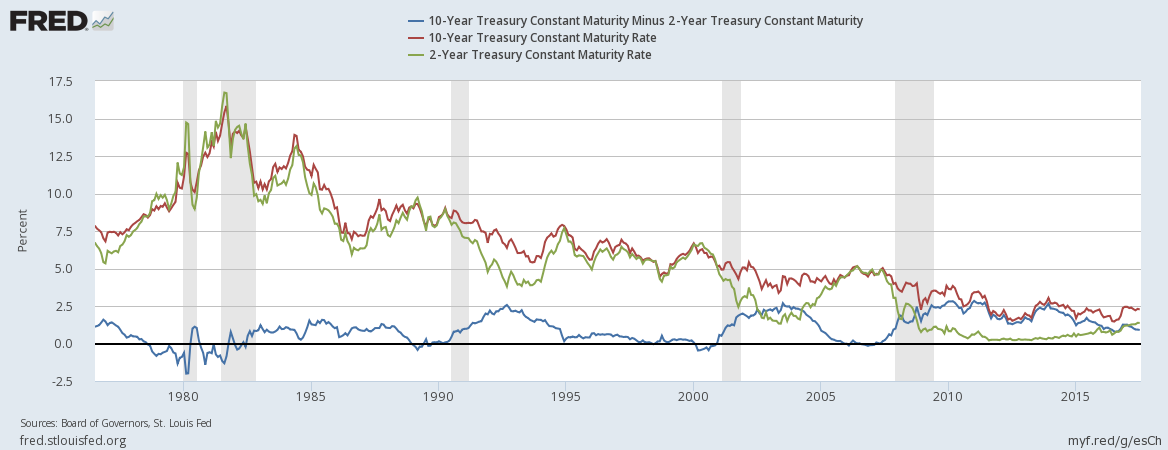

Investors have used the yield curve of U.S. Treasuries (2s10s Curve) as a reliable recession indicator for several decades. An economic expansion is usually accompanied by a slowly flattening (NASDAQ:FLAT) yield curve. The U.S. yield curve usually flattens so much at the end of an economic cycle that it eventually inverts (goes negative). After inversion, the U.S. yield curve quickly steepens (NASDAQ:STPP) and a recession ensues. You can see from the chart below that the U.S. yield curve has inverted before each of the last five recessions.

The inversion occurs right before a recession as bond traders indicate that short-term risk exceeds long-term risk. If we look at the two elements of the yield curve separately, we see that before a recession occurs, short-term yields rise and eventually surpass longer-term yields.

Once the recession hits, both short-term and long-term yields plummet as investors pile into "safe-haven" assets like U.S. Treasuries. Two-year Treasury yields fall faster than 10-year yields causing the yield curve to sharply steepen.

It would be nice if we could use this indicator for predicting all future recessions as it has been extremely accurate in the past. Unfortunately, I see major issues with the reliability of this indicator moving forward.

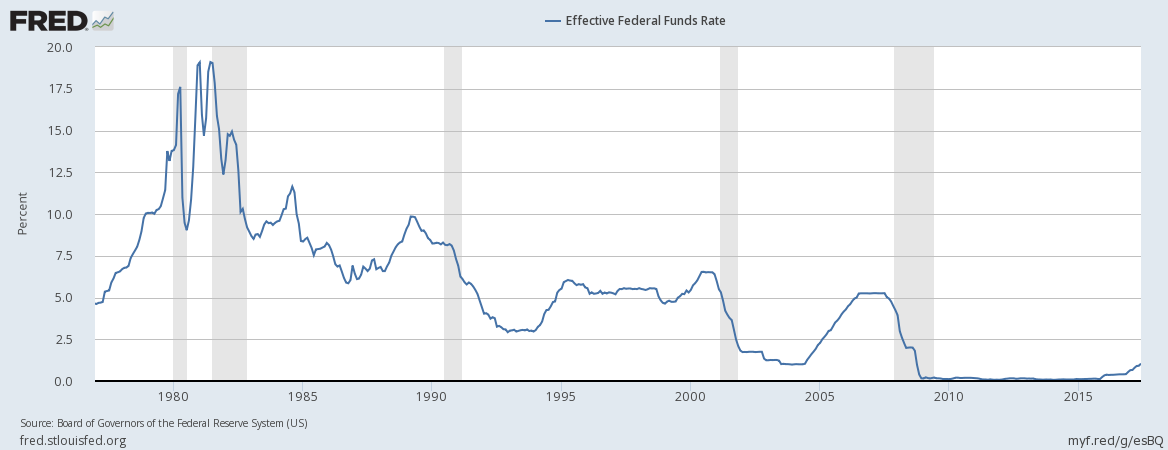

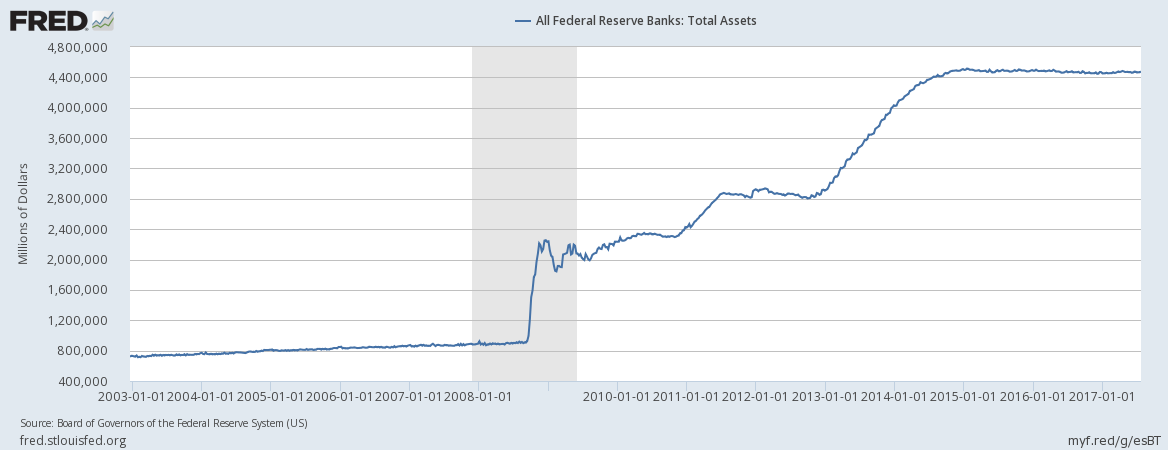

I'm sure many of you have heard the famous song "Turning Japanese" by The Vapors. Well, U.S. monetary policy has turned Japanese after the Federal Reserve pursued an aggressively loose policy to combat the fallout from the Great Recession of 08-09. The Effective Federal Funds Rate was dropped to zero to encourage borrowing, and trillions of dollars worth of 2-year Treasuries were purchased by the Federal Reserve to inject liquidity into the banking system.

.

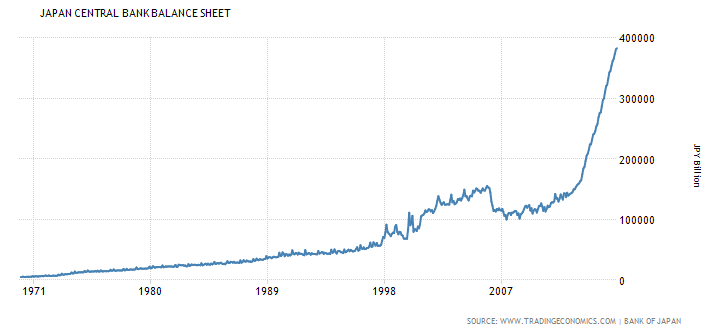

Both of these Federal Reserve tactics were considered by many to be a form of highly experimental monetary policy. However, the Japanese were employing these tactics long before the U.S. The Bank of Japan sunk their interest rate to near zero in the early 90's, and their balance sheet began to swell up with bond purchases near the turn of the century.

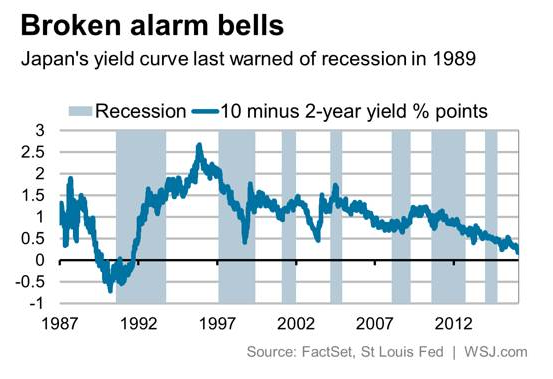

So, what does this tell us about the reliability of the yield curve as a recession indicator? It tells us that the indicator could very well be broken. Since Japan has begun employing this type of monetary policy, its yield curve has failed to predict recessions as it once did. The last time Japan's yield curve was able to successfully predict a recession was 1989, before it began its incredibly loose monetary policy. Now, Japan's yield curve does not invert and sometimes acts randomly before or during a recession.

Japan's yield curve does not invert because the central bank's 0% interest rate and mass purchases of Japanese bonds have put immense downward pressure on short-term bond yields.

Remember, in past U.S. economic cycles, 2-year yields would rise above 10-year yields to cause the inversion. With such great downward pressure on short-term yields, the 2-year U.S. Treasury may never be able to rise enough to catch up to longer-term yields. Therefore, there is a good chance that the U.S. yield curve doesn't flash the warning signal this time. Based on the Federal Reserve's mimicry of the Bank of Japan, it should not be inconceivable that the U.S. yield curve is now broken as a recession indicator.

If that is truly the case, the next recession may catch many investors completely off guard.

People who have used the U.S. yield curve to predict recessions in the past may be waiting on an inversion that never comes. When the U.S. yield curve bottoms, it usually takes several months to over a year for a recession to occur. In my honest opinion, the U.S. yield curve bottomed in mid 2016, just below the 1% mark. That would put the recession months away instead of years away.

In anticipation of the next recession, my portfolio is approximately 50% in longer-term bonds. I am also considering replacing some of the iShares 20+ Year Treasury Bond ETF (NYSEARCA:TLT) with the Direxion Daily 30-Year Treasury Bull 3x Shares ETF (NYSEARCA:TMF) to have less of my portfolio tied up. If you are looking for a less volatile approach, you can go with the iShares Core Total U.S. Bond Market ETF (NYSEARCA:AGG).

When the yield curve steepens -- which I believe has already begun -- bond yields drop and prices go up.

When the yield curve steepens -- which I believe has already begun -- bond yields drop and prices go up.

The U.S. yield curve may not always predict recessions with inversion. Japan is a great example of this fact, and U.S. monetary policy now closely resembles that of Japan. I urge you all to be extra cautious when anticipating the next recession. Relying too much on past data sometimes has severe consequences.

0 comments:

Publicar un comentario