When Trillions Of Dollars Go Blind: ETFs As The Biggest Danger To Markets

by: The Heisenberg

- Howard Marks is out with a fantastic new note on the dangers of passive investing and ETFs.

- It echoes quite a bit of what I've written over the past 13 months.

- Here are the main points along with my analysis.

- It echoes quite a bit of what I've written over the past 13 months.

- Here are the main points along with my analysis.

I've spilled so much digital ink writing about the inherent dangers of ETFs and the risk that we've gone too far down the passive investing rabbit hole, that it would be next to impossible for me to catalogue every post.

What I've tried to do, over the past 13 months or so, is build a good case for my contention that while low-cost, passive investing is certainly a positive development, one can always have too much of a good thing.

And indeed, recent "innovations" in exchange-traded products have created an environment where it's no longer entirely clear what the "thing" we're talking about even is.

No one that I'm aware of is going to argue that investors shouldn't have access to passive investment vehicles that, for just a handful of basis points in what amount to token fees, allow regular folks to replicate the returns of benchmark US equity indices (SPY). Buy the index, sit on it, and enjoy the benefits of sharing in the continued, long-term prosperity of the US corporate sector.

That's great. But even at that very basic level, there are some problems.

The reason I'm bringing this up again on Wednesday evening is because Howard Marks is out with a new note and it echoes virtually every concern I have raised both on this platform and over at HR about ETFs. In fact, Marks even cites some of the very same ETFs I've complained about and decries some of the very same dynamics I have written at length about here.

I'm going to take you on a quick tour of Marks' critique and along the way, I'll reference my previous work and commentary just so you can see that I am by no means alone in raising these issues.

Let's start at the above-mentioned "very basic level." Common sense tells you that the indiscriminate funneling of money into indices leads to the misallocation of capital. I talked about this in "If You Own An S&P ETF, You Won't Like This." Recall this from Goldman (GS):

With the runaway growth of these products we ask if following an index is the optimal allocation for capital. Namely we run an analysis juxtaposing the ROIC v WACC of the S&P 500 by weights of the underlying stocks. We find that it is not.

There appears to be no direct relationship between a company's ROIC/WACC and its weight in the S&P 500. ROIC / WACC for the top 10 companies in the S&P 500 (20% of the index), on average, is lower than that of the next 70 companies.

Again, this is common sense and it conjures memories of a now infamous client letter out earlier this year in which Arik Ahitov and Dennis Bryan, who run the $789-million FPA Capital Fund, called ETF's "WMDs." Here's an excerpt:

The consequence of unrelenting inflows into passive funds is that stocks that are included in a major index receive ongoing support by the indiscriminate purchases made by these funds regardless of a company’s fundamentals. Unfortunately, these buy and sell decisions are entirely disconnected from a company’s fundamentals.

It doesn't take a leap of logic to get from there to the argument about how passive flows create a self-feeding loop for certain companies. Here's Howard Marks from today's note:

The large positions occupied by the top recent performers – with their swollen market caps – mean that as ETFs attract capital, they have to buy large amounts of these stocks, further fueling their rise. Thus, in the current up-cycle, over-weighted, liquid, large-cap stocks have benefitted from forced buying on the part of passive vehicles, which don’t have the option to refrain from buying a stock just because its overpriced.

Like the tech stocks in 2000, this seeming perpetual motion machine is unlikely to work forever.

Now, connect the dots (PeeWee style) to a piece I wrote several weeks ago called "The Beginning Of 'Factormageddon'? A Black Swan Volatility Event."

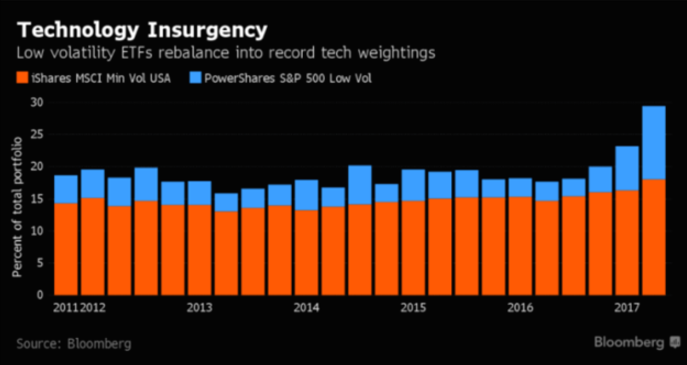

This dynamic (Marks' "perpetual motion machine") ends up making the high-flyers (so, in the current environment, "FAANG" and "FAAMG") synonymous with things like momentum and, more worryingly, low volatility.

Well, guess what? "Momentum" and "low volatility" are two of the themes for factor-based ETFs and "smart" beta products like the $14 billion PowerShares S&P 500 Low Volatility Portfolio ETF (SPLV) and the $6.9-billion iShares Edge MSCI Minimum Volatility USA ETF (USMV).

So now, those funds are buying the very same names, perpetuating the very same dynamic that made those names synonymous with the "factors" in the first place:

(Bloomberg)

This leads us directly to another problem. Here's Marks again:

The low fees and expenses that make passive investments attractive mean their organizers have to emphasize scale. To earn higher fees than index funds and achieve profitable scale, ETF sponsors have been turning to “smarter,” not-exactly-passive vehicles. Thus ETFs have been organized to meet (or create) demand for funds in specialized areas such as various stock categories (value or growth), stock characteristics (low volatility or high quality), types of companies, or geographies. There are passive ETFs for people who want growth, value, high quality, low volatility and momentum.

Going to the extreme, investors now can choose from funds that invest passively in companies that have gender-diverse senior management, practice “biblically responsible investing,” or focus on medical marijuana, solutions to obesity, serving millennials, and whiskey and spirits.

But what does “passive” mean when a vehicle’s focus is so narrowly defined? Each deviation from the broad indices introduces definitional issues and non-passive, discretionary decisions.

Of course with "discretionary decisions" comes higher fees and that effectively negates one of the main advantages of passive investing (the low-cost advantage). This was the subject of a post I wrote over at HR about the "New Tech and Media ETF" (FNG) which charges investors a whopping 0.85% to basically buy tech stocks on the rather flimsy justification that (and this is a quote from the sponsor's official webpage):

The actively managed aspect of FNG allows for evolution and relevance.

As if all of that doesn't create a precarious enough setup, do recall that one of my main points of contention with the ETF industry is the extent to which HY bond funds (HYG) and also emerging market bond funds (EMB) promise intraday liquidity against underlying assets that are not just illiquid, but are in fact highly illiquid.

This only works as long as flows are diversifiable (i.e. as long as one manager is seeing inflows when another is seeing outflows) or when the APs are willing to step in and arb away NAV disconnects. If one or both of those circumstances change in a pinch, the assets underlying the ETF units will have to be sold into an illiquid market that will be rendered even more illiquid than it already was by virtue of the fact that it will be, by definition, falling when the redemptions come in. I've written mountains on this (see here on HY and here on EM, for instance).

Here's Marks on this:

As a product of the last several years, ETFs’ promise of liquidity has yet to be tested in a major bear market, particularly in less-liquid fields like high yield bonds.

And all of the above doesn't even begin to touch on exactly what it was that happened on the morning of August 24, 2015. I don't care what you read, no one - I repeat no one - knows exactly what went wrong, but what we do know is that liquidity provision was an issue.

With that in mind, consider this out earlier this week from Reuters:

Goldman Sachs Group Inc is pulling back substantially from trading that helps backstop the fast-growing use of U.S. exchange-traded funds, giving smaller firms an opportunity to grab market share.

Goldman has told fund providers it is scaling back its role as a top lead market maker (LMM) for ETFs and has already slashed the number of funds it supports in that capacity, according to disclosures, fund managers and other trading firms this month

Of course, everyone is trying to spin this idea of "lesser-known" companies getting a shot as a generally positive development, but count me skeptical.

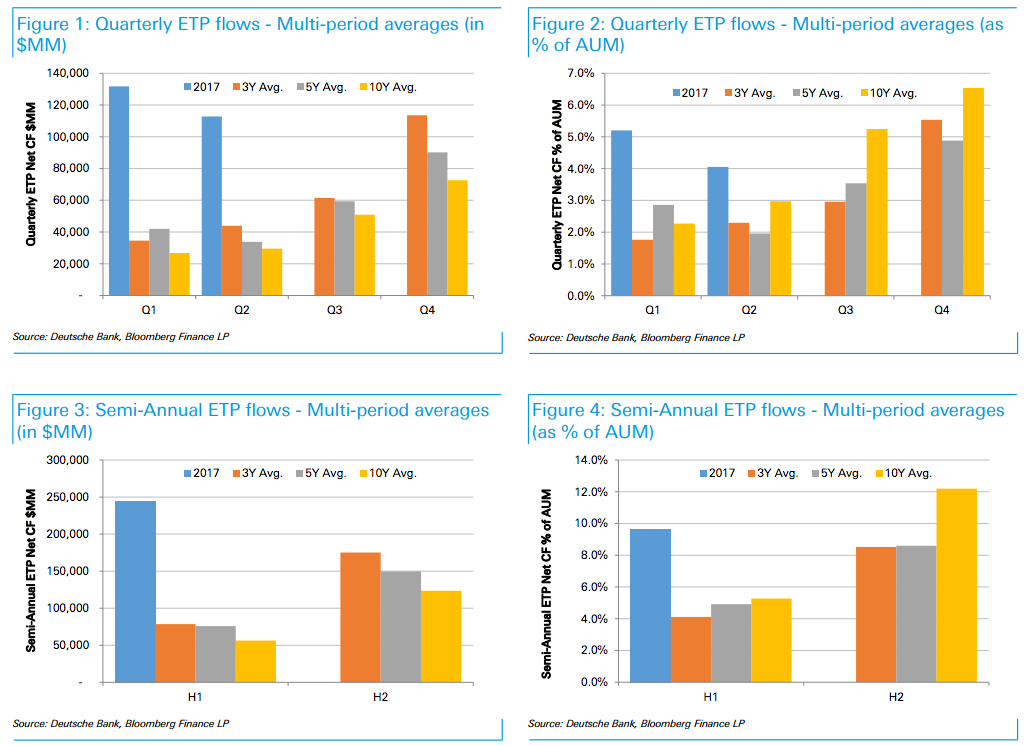

More to the point, I'm not terribly excited about the prospect of a bunch of small-ish HFT firms taking over ETF market making from Goldman at a time when inflows into ETFs very nearly surpassed an all-time high for any full year in just the first six months of 2017:

.

(Deutsche Bank)

(Deutsche Bank)

It's up to you to do with all of this as you see fit, and maybe you don't think it has any relevance for your particular set of circumstances.

But I would encourage you to consider whether it's possible that a critical part of this market's microstructure (and one that everyone thinks is the greatest invention since sliced-bread), is actually rickety, untested, and potentially dangerous. Here's one more quote from Marks:

What should we think about the willingness of investors to turn over their capital to a process in which neither individual holdings nor portfolio construction is the subject of thoughtful analysis and decision-making, and in which buying takes place regardless of price?

I think I've made a pretty compelling case above, but for those interested to read Marks' full letter along with some exceedingly amusing anecdotes from me (including my brief interaction with the CEO of AdvisorShares), you can check it out here.

0 comments:

Publicar un comentario