The Slowdown Is Happening

by: Eric Basmajian

- The impact of negative wage growth is beginning to rip through the economy as the economic data shows serious warning signs.

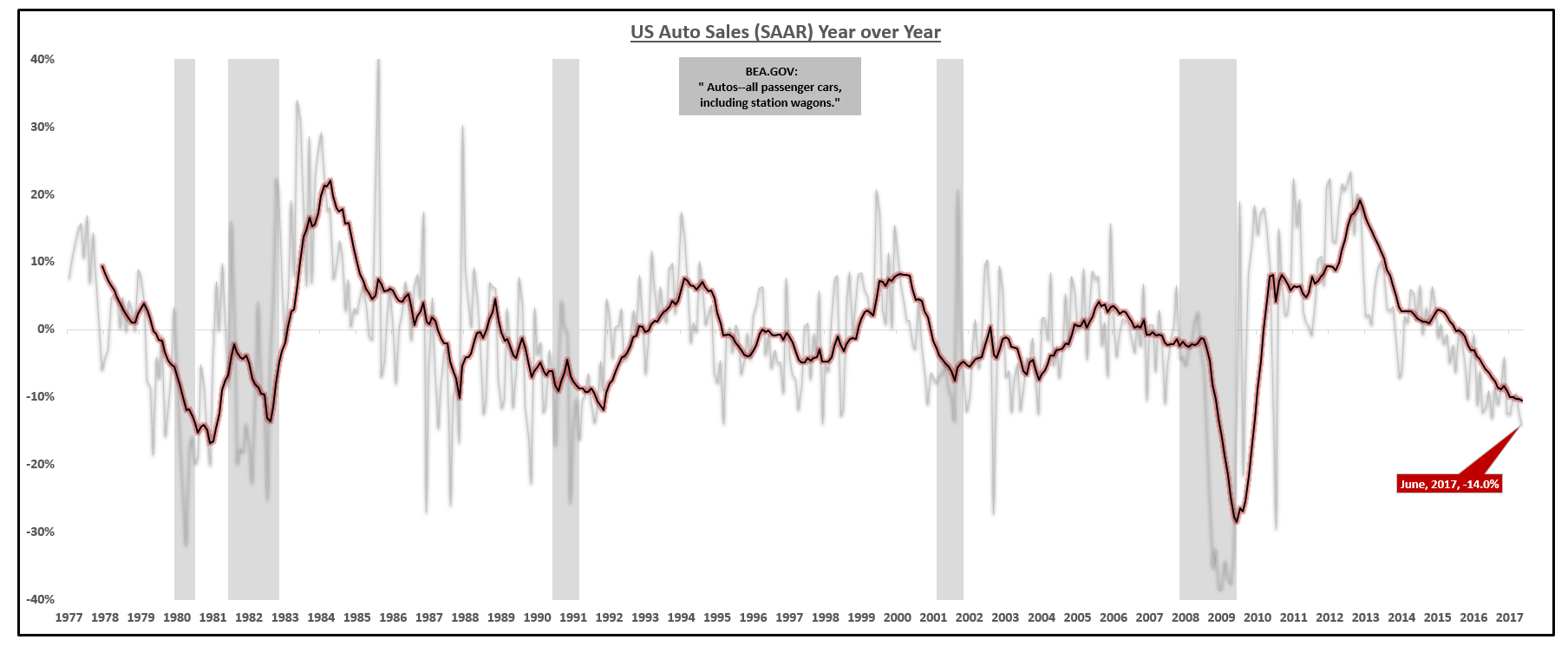

- Auto Sales are down 14% vs. last year and the problem is getting worse.

- With a slowing economy and record high valuations, it's time to 'bullet-proof' your portfolio to withstand a turbulent market ahead.

- Added high yield bonds as a short on the JNK ETF in this month's asset allocation changes.

Overview of July

- Auto Sales are down 14% vs. last year and the problem is getting worse.

- With a slowing economy and record high valuations, it's time to 'bullet-proof' your portfolio to withstand a turbulent market ahead.

- Added high yield bonds as a short on the JNK ETF in this month's asset allocation changes.

Overview of July

On balance, the economy slowed in July relative to the previous month with only 41% of the data improving from June. The most notable and troubling declines are in the wages and income categories. Wage growth is negative which is putting pressure on the consumer in the face of soaring home prices.

The biggest market theme that is ultimately causing the slow down in the economy, and soon the stock market, is the inability of wage growth to outpace shelter inflation. For the past several years wage growth has been muted and the consumer was able to eek out 1.5%-2% growth in wages after adjusting for rent or shelter inflation. This is why the economy has grown in that same range of 1.5%-2% for the past several years as well.

As of the past year or so, that trend has become decidedly worse as the consumer is now underwater.

Wage growth - rent inflation has been negative or just above zero for many months signaling that there is no marginal growth coming in the near future from the consumer. Many have brushed this off, foolishly in my opinion, but now the adverse effects of negative wage growth are starting to appear.

I will run through the following categories of data, bulleted below, and outline the changes from last month and the trends of each sector moving forward.

Macro Data Summary

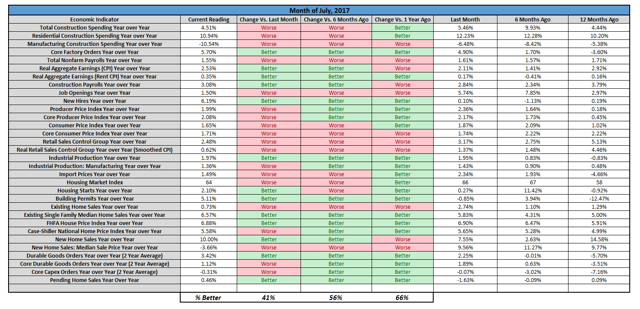

Below is a running macroeconomic data table I track and regularly publish.

The data table contains roughly the 30 important macro data points that are released each month. The table shows the current growth rate as well as the growth rate last month, six months ago, and one year ago.

Aggregate Economic Table for July 2017:

The reason for this is to indicate clearly if growth is getting better or getting worse and as the table clearly shows, on balance, the data is getting worse.

I will start with labor and wages and work through the other segments of the economy.

Labor & Wages:

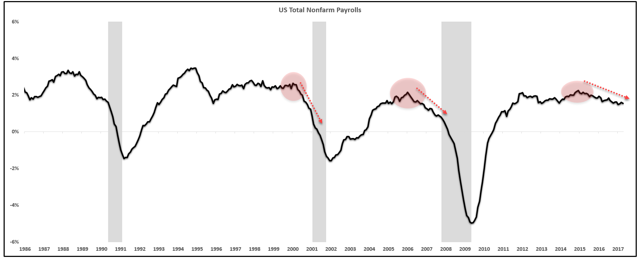

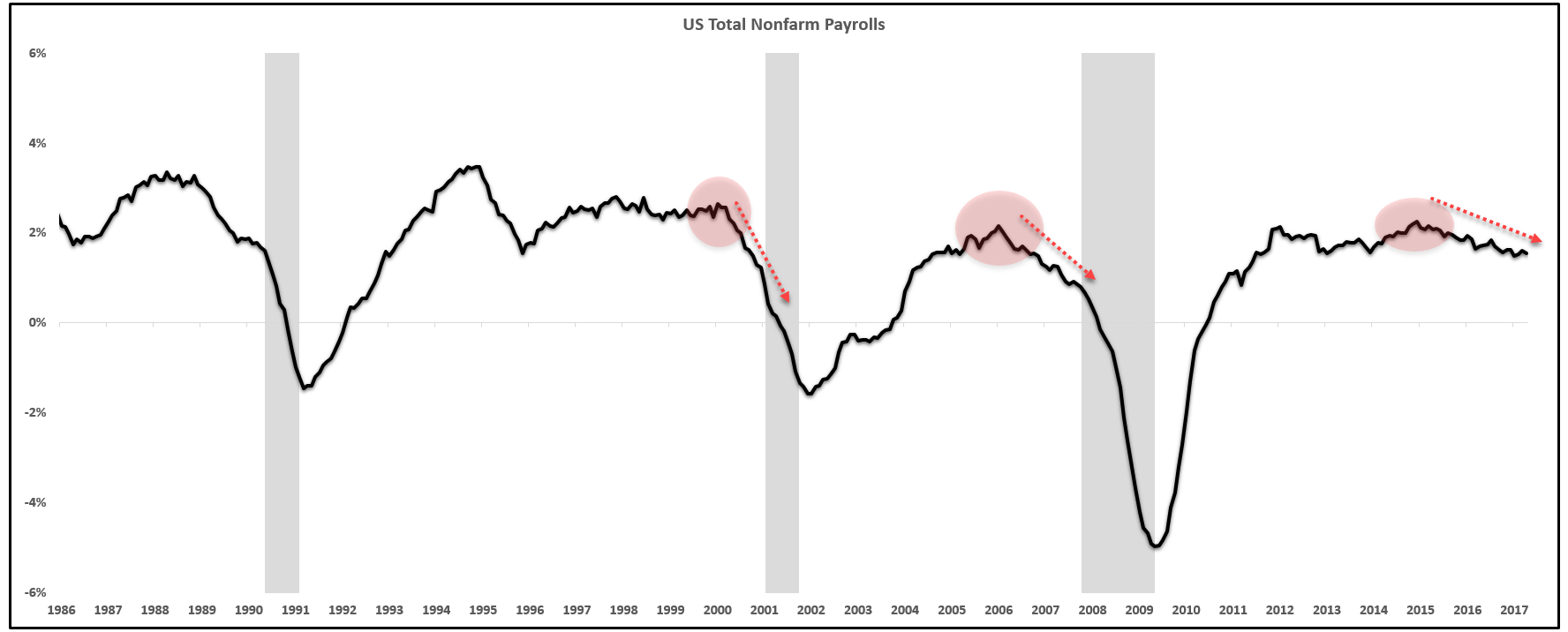

Nonfarm payrolls growth continues to trend downward after the peak in 2015 with some month to month volatility. The trending direction of the year over year growth in nonfarm payrolls is still overwhelmingly lower.

Nonfarm Payrolls Year over Year:

(Source: BLS)

(Source: BLS)

This past month showed another deceleration in the rate of growth in nonfarm payrolls declining to 1.55% from 1.61% a month prior. This is a fairly significant month to month decline.

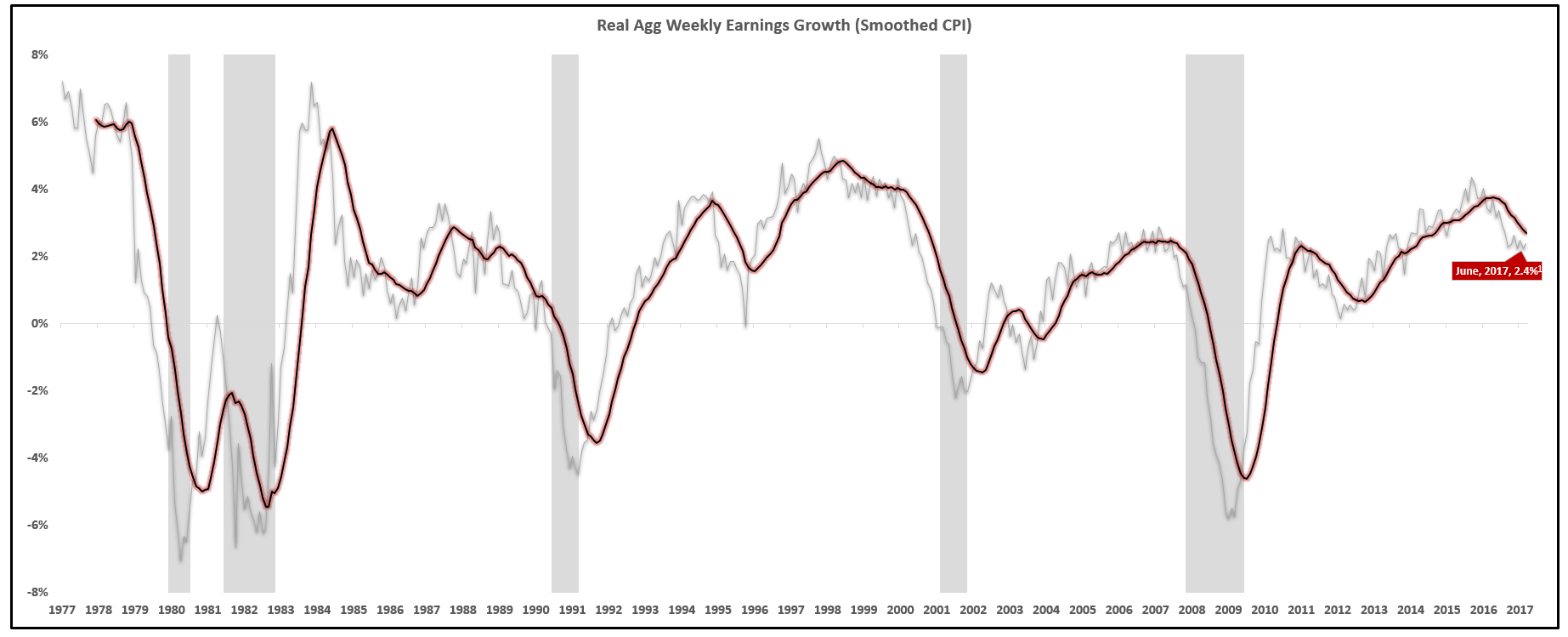

Growth in employment has been slowing for over two years. As employment growth slows, the growth in total wages earned slows as well. Wages are the driving factor behind all consumption.

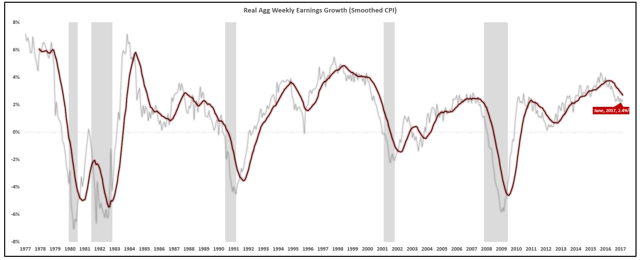

Real Aggregate Wages (12 Month Average Inflation) Year over Year:

(Source: BLS)

(Source: BLS)

Real aggregate earnings is the most important metric to follow as it measures the growth in real dollars earned for the entire economy. The measure of real aggregate earnings is very closely tied to the growth rate of the economy.

Currently, the 12-month average of real aggregate wage growth is 2.4% and falling, right in line with the growth rate of the economy of about 2%.

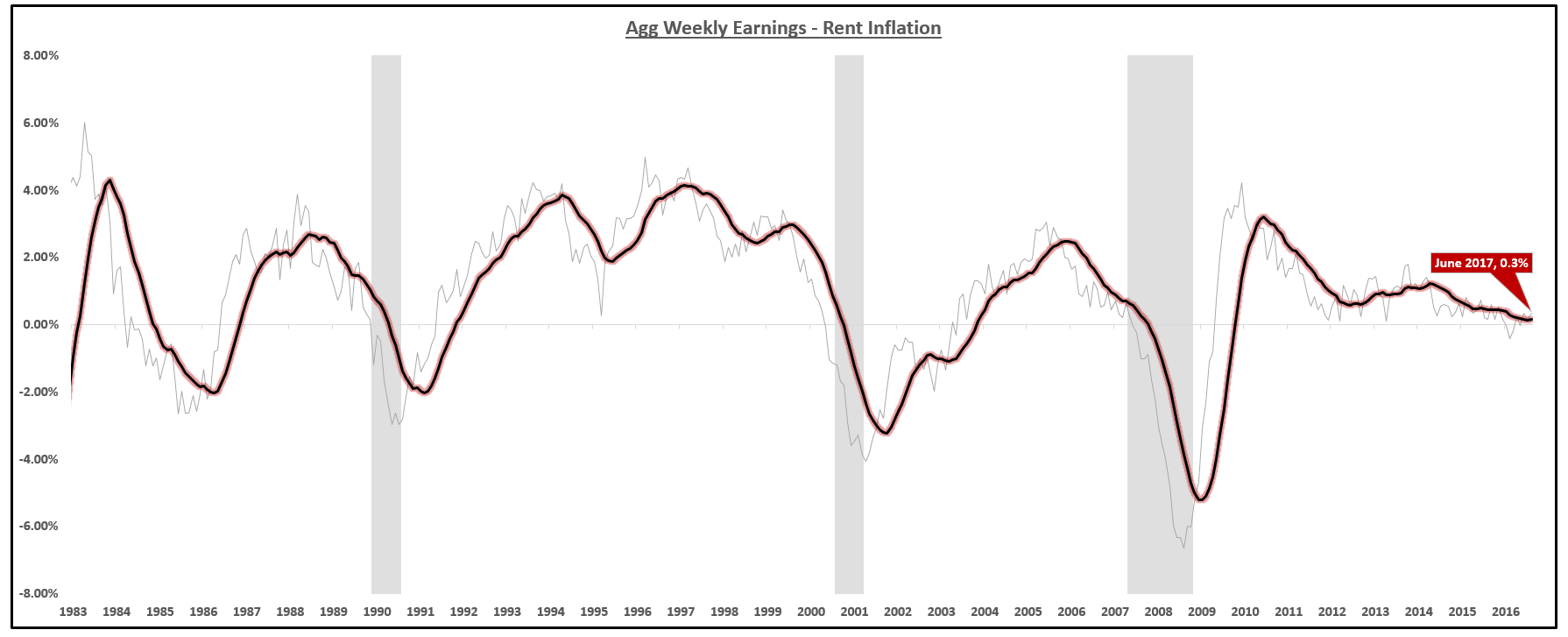

Real Aggregate Wages (Minus Rent Inflation) Year over Year:

(Source: BLS)

(Source: BLS)

The inflation in rent and housing has been squeezing consumers, and the past 12 months, consumers have barely been able to break-even and show growth above 0% after housing costs.

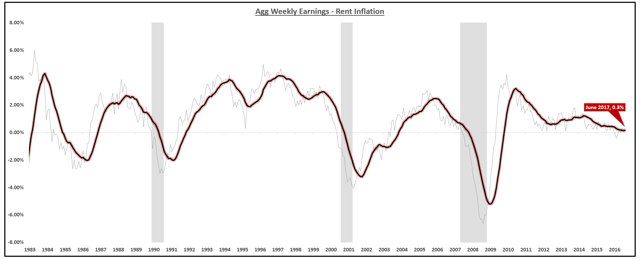

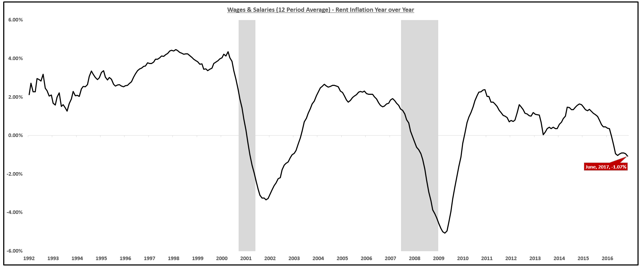

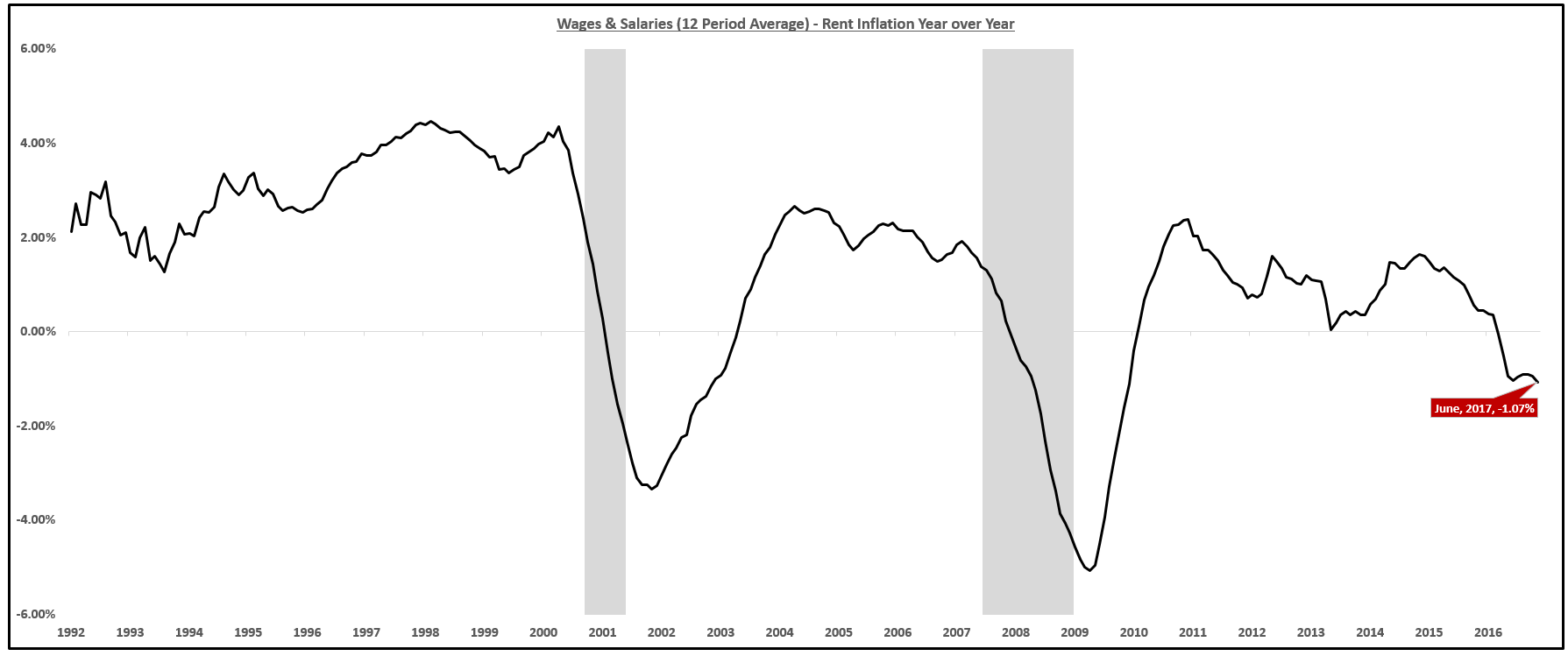

Wages & Salaries - Rent Inflation Year over Year:

(Source: BEA)

(Source: BEA)

Wages and salaries - rent inflation is severely negative which is signaling immediate distress to the consumer. In fact, the only time this metric was negative during the past 30 years was in recessions so it's current standing at -1.1% is very alarming.

This negative growth in wages cannot be shrugged off anymore because the adverse effects are bleeding into headlines left and right.

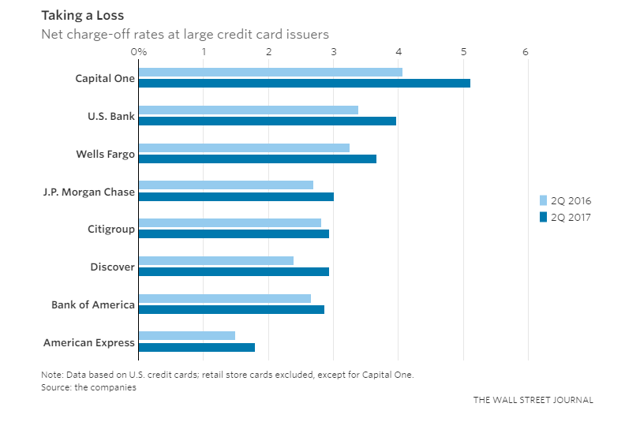

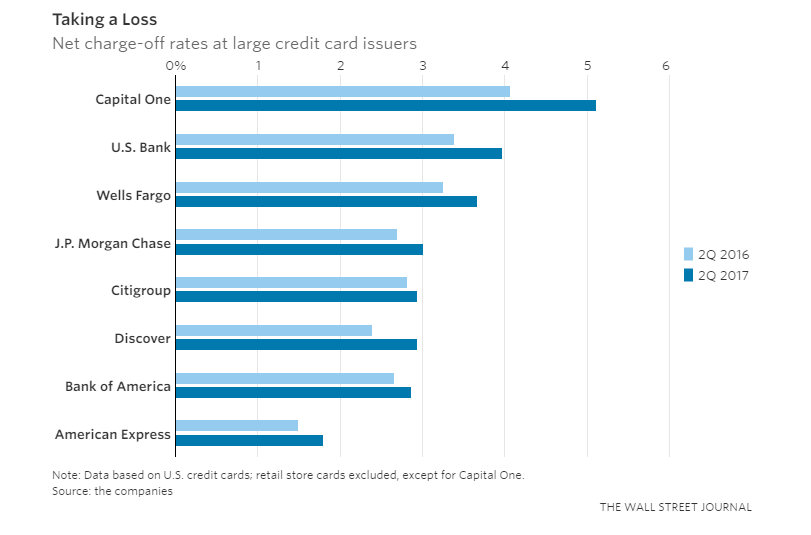

Credit card charge offs are rising at most credit providers as seen in the chart below.

Charge Offs:

(Source: WSJ)

(Source: WSJ)

All of this is happening while the economy is supposedly at 'full employment'. If the economic data is deteriorating this rapidly under full employment, a slow down in the labor market has the potential to amplify these trends.

Autos is another area that the stressed consumer is appearing.

Auto Sales:

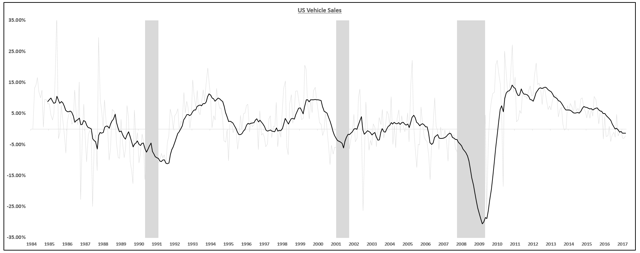

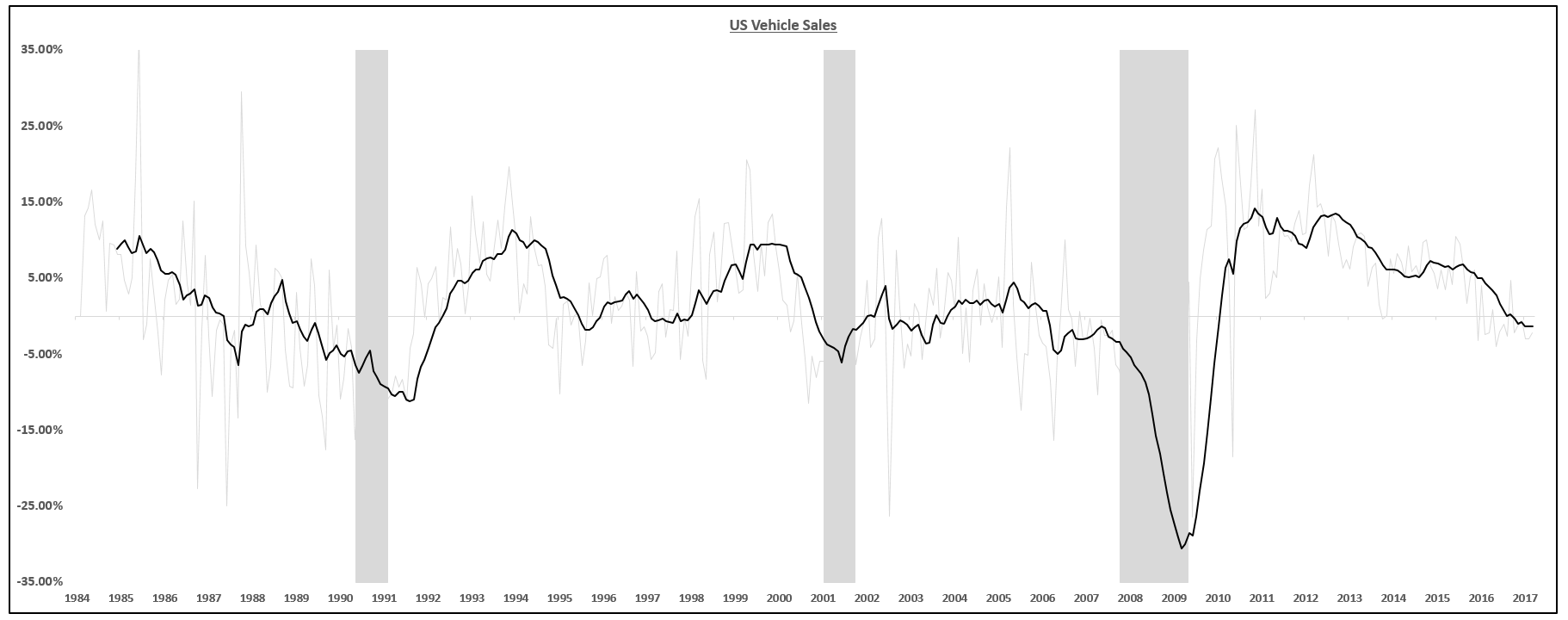

Total vehicle sales (autos, light trucks, heavy trucks etc.) marked another quarter of negative growth at -2.16% year over year. This sector should be sounding alarms for everyone.

Total Vehicle Sales Year over Year:

(Source: BEA)

(Source: BEA)

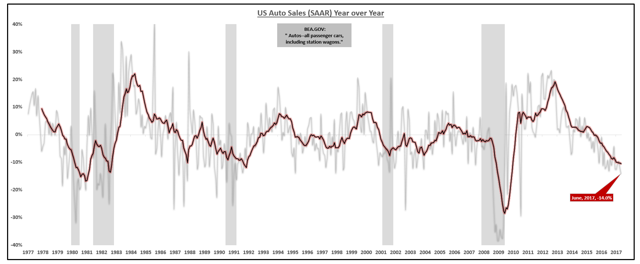

Auto sales are collapsing at -14% year over year.

Auto Sales Year over Year:

(Source: BEA)

(Source: BEA)

You can expect this trend to continue. If wage growth is negative after housing costs, there is no money left to purchase new vehicles. This could be a problem area for the market in the near future. I would avoid stocks related to the auto sector at all costs.

Real Estate:

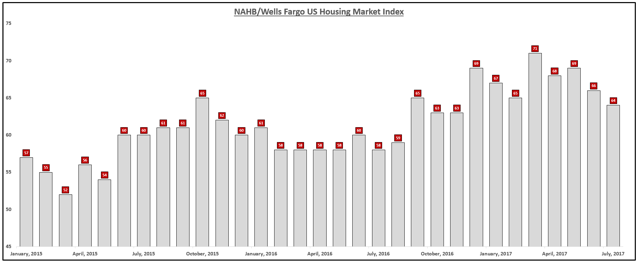

The National Association of Home Builders publishes the 'Housing Market Index' each month which gauges the sentiment of a panel of homebuilders who sit on the board of the NAHB.

Respondents are asked to measure their feeling on the housing market as "good", "fair", or "poor".

If all panelist respond "good", then the index is 100. If all answer "poor", then the index is 0.

For July, the Housing Market Index declined to 64 from 66 a month ago and 67 six months ago.

Housing Market Index:

(Source: NAHB)

(Source: NAHB)

There was a large jump after the election in all confidence based surveys due to increased hopes for reduced regulations, tax cuts and more. The longer these policies are delayed and the more they look unlikely, the more the real weakness in the economy is in focus and that is not a tailwind for housing.

July's Housing Market Index was very weak across the board which signals that the change in sentiment is not regional but broad based.

Here are all the components of the report.

Housing Market Index Breakdown:

(Source: NAHB)

(Source: NAHB)

You can easily see that all but two categories were worse than last month and every category was worse than 6 months ago. The Trump fueled enthusiasm is fading.

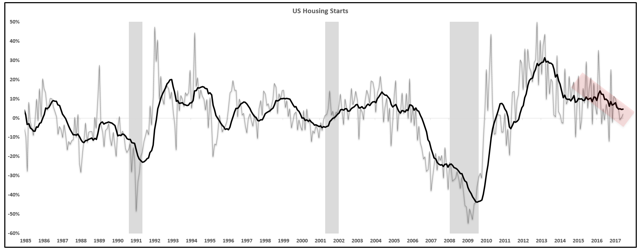

Housing starts are the number of new residential construction projects that have begun during any particular month. The New Residential Construction Report, commonly referred to as "housing starts," is considered to be a critical indicator of economic strength.

Housing starts had a massive rate of growth in 2013. That growth rate fell off but rebounded from 2015-2016. That growth rate is now rolling over and resuming the longer run down trend from the 2013 peak.

Housing Starts:

(Source: Census Bureau)

(Source: Census Bureau)

The growth in Housing starts is at a multi-year low while home prices are at a multi-year high...

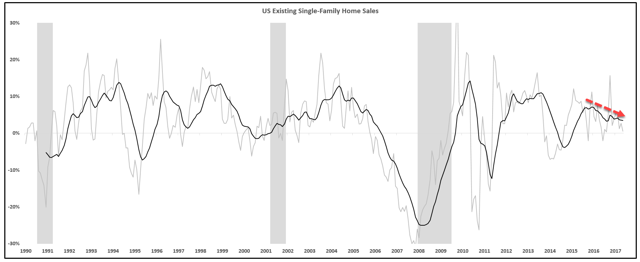

The Existing-Home Sales data measures sales and prices of existing single-family homes for the nation overall, and gives breakdowns for the West, Midwest, South, and Northeast regions of the country. These figures include condos and co-ops, in addition to single-family homes.

This past month's report on Existing Home Sales showed a decline in the growth rate to just 0.73%. The volume of transactions is really drying up based on the data.

A growth rate of 0.73% is lower than last month, six months ago, and a year ago making the downward trend clear.

Existing Home Sales:

(Source: NAR)

(Source: NAR)

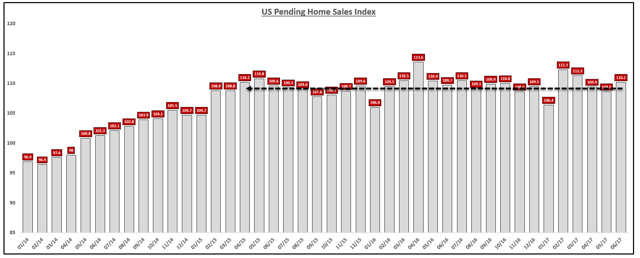

Pending Home Sales (PHS), published by the National Association of Realtors (NAR), represent signed contracts for new homes, not closes. PHS typically leads Existing Home Sales (90% of the housing market) by about two months.

Pending home sales have been unchanged for two years.

Pending Home Sales Unchanged:

(Source: NAR)

(Source: NAR)

I continue to be perplexed by the mainstream bullishness on housing despite truly lack luster data.

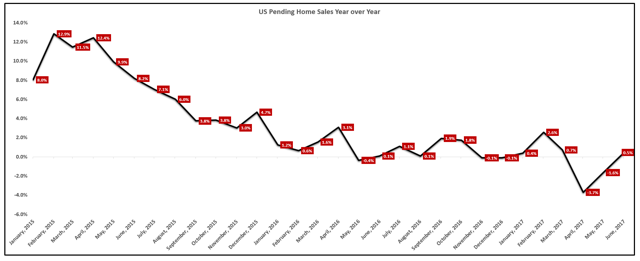

When looking at Pending Home sales growth, the trend is falling as well.

Pending Home Sales:

(Source: NAR)

(Source: NAR)

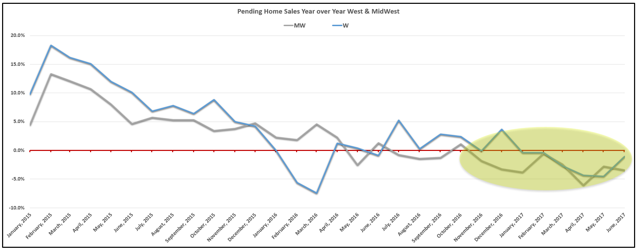

The two notable areas are the Midwest and West markets where Pending Home sales growth has been negative for several months in a row. Due to the lead in Pending Home sales vs. Existing Home Sales, I expect there to be a rough patch ahead in these two markets in the next few Existing Home sales reports.

Pending Home Sales West & Midwest:

(Source: NAR)

(Source: NAR)

In the housing market, there are two types of homes; Existing Homes and Newly Constructed homes.

Existing Home sales make up roughly 90% of the housing sale volume while New Home sales is about 10%.

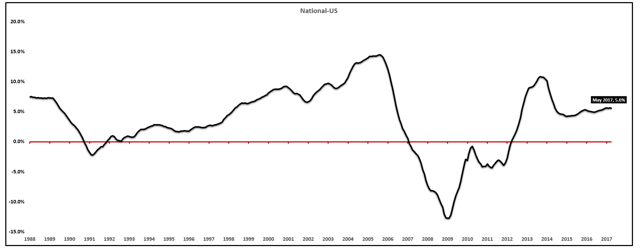

Lately, there has been a divergence in the price growth of these two markets. The price of newly built homes is falling at -3.4% year over year as of the last report while the price of EHS is soaring, up nearly 6% year over year.

How do you explain this divergence in the market?

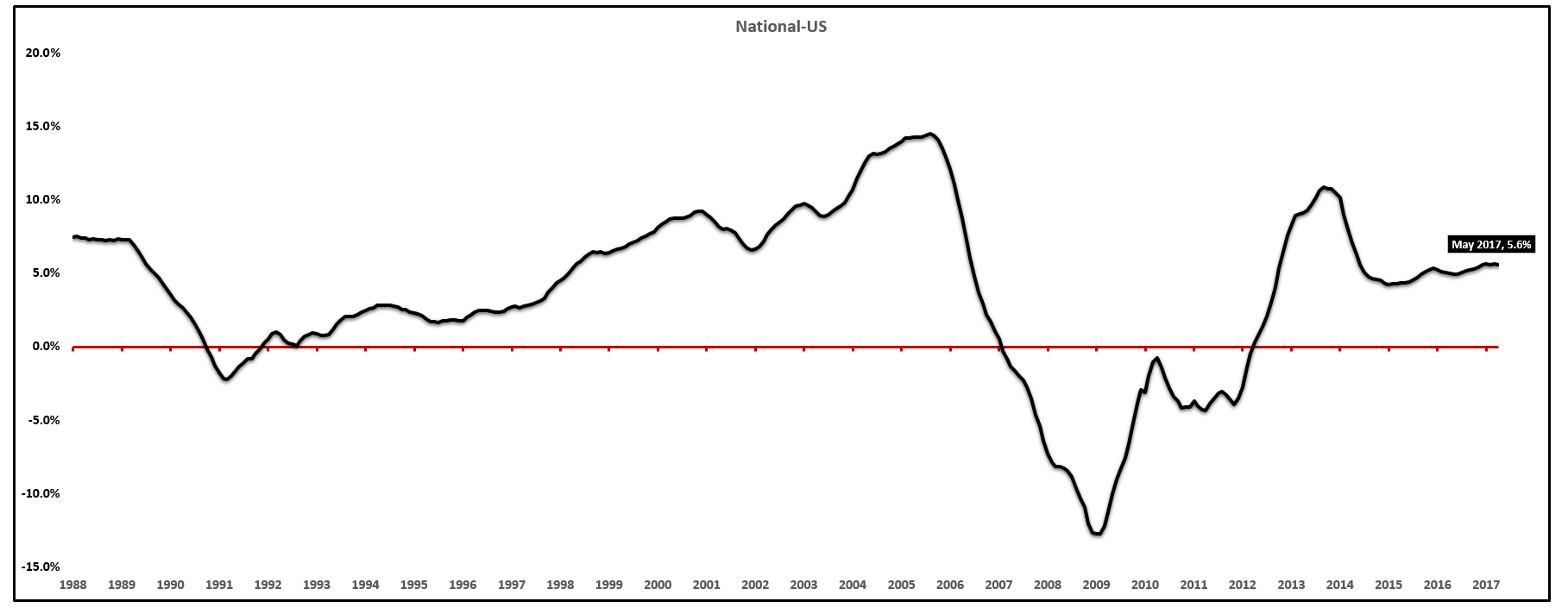

National Home Price Index Year over Year:

(Source: Dow Jones, S&P)

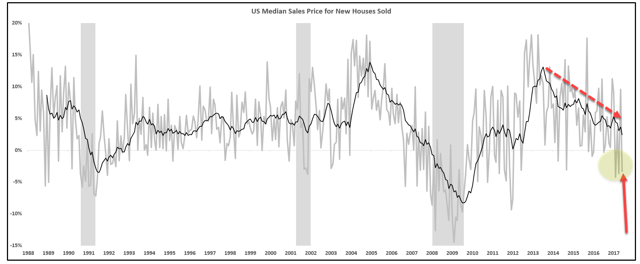

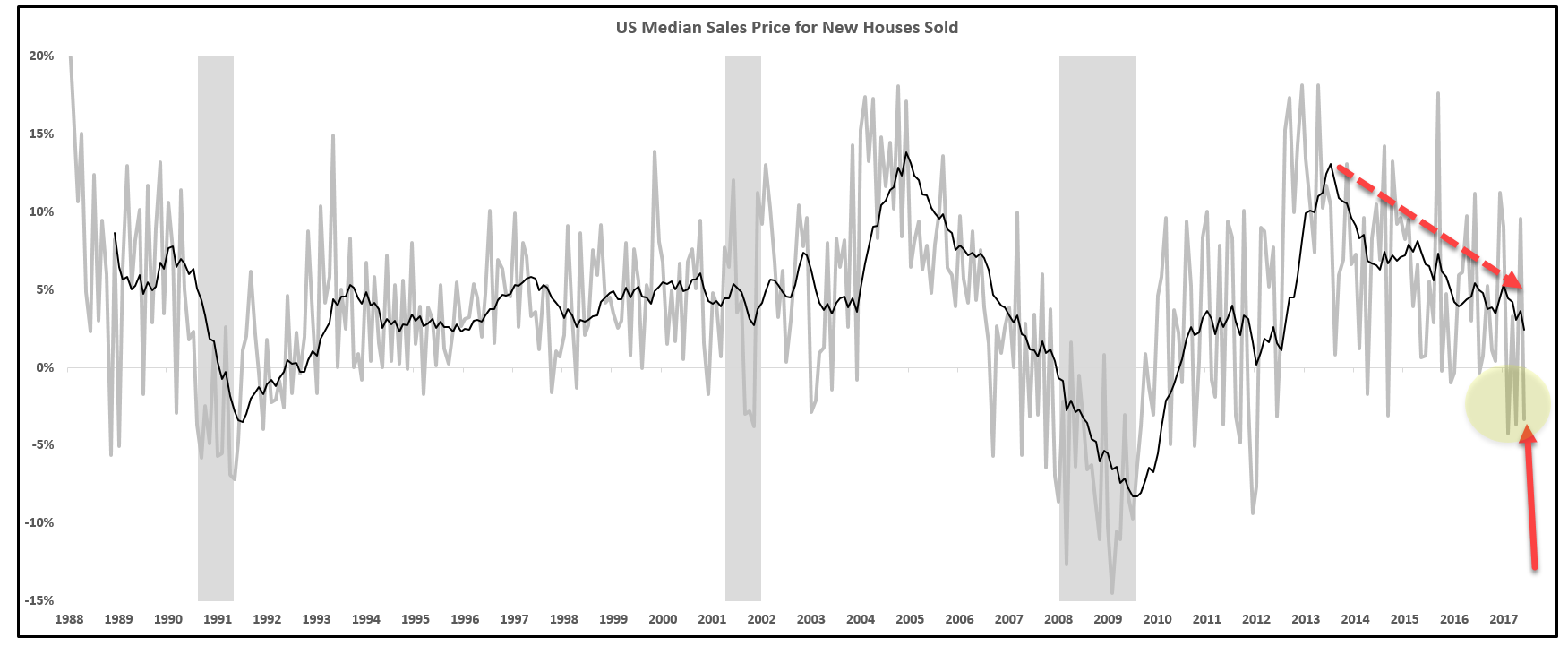

Below is a chart showing the year over year growth in the median sales price for new homes. You can see the trend (black line) is sharply lower and the last data point (grey line/yellow circle) was negative.

Median Price of New Homes Year over Year:

Many talk about rising prices in the housing market but actually when you look at the details and all the reports, only the price of Existing Home sales is rising, New Home sales prices are falling and falling quite rapidly...

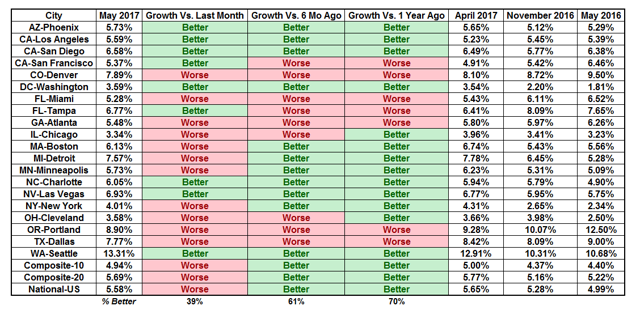

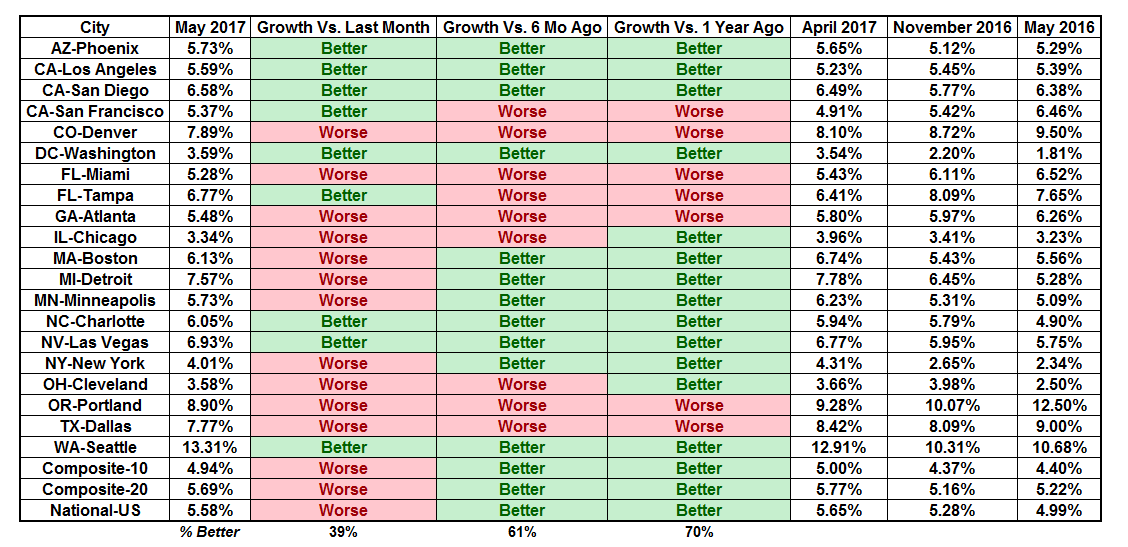

The chart below is a quick reference on existing home price growth. It shows the current year over year growth rate by city as well as the growth rate last month, 6 months ago, and 1 year ago. This is an easy way to see the current growth rate and if that growth rate is accelerating or decelerating.

Home Price Table:

(Source: Dow Jones, S&P)

(Source: Dow Jones, S&P)

Many of the cities that showed slower growth have now posted two or three consecutive months of deceleration.

Two or three months of home price growth deceleration is not enough to change the trend. For now, the trend of home price growth is still clearly higher.

I have outlined how home prices growing faster than wages is unsustainable and how wage growth has to increase or home price growth has to fall (this article, here, outlines that dynamic in detail).

When looking at the weakness in wages, the multi month deceleration in the national home price growth and the broad month to month deceleration in the majority of cities, the picture on home prices becomes something to keep a close eye on.

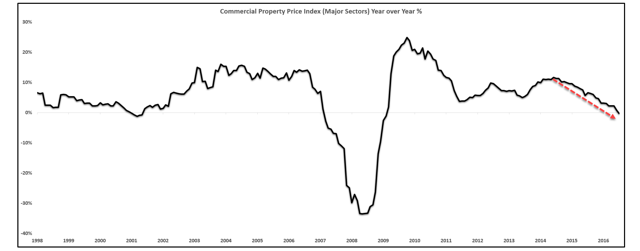

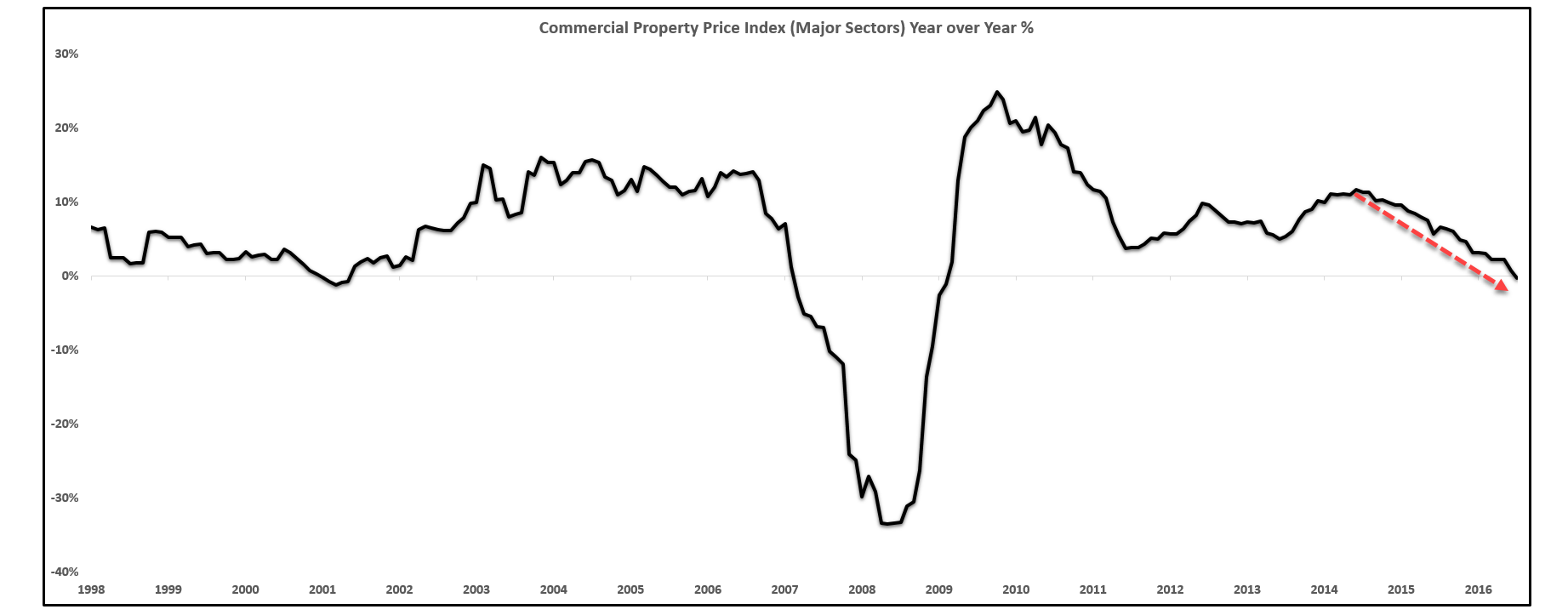

Commercial Real Estate prices are on the verge of posting the first year over year decline since 2007 and only the third time in nearly 30 years.

Commercial Real Estate Prices:

(Source: GreenStreetAdvisors)

(Source: GreenStreetAdvisors)

This is an area of the market to keep a close eye on as it poses a significant risk to the market.

Consumption:

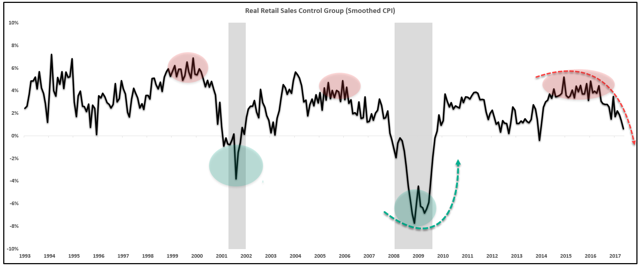

Retail sales for the June reporting period were very weak and caused even the most optimistic analysts to question the prospects for high economic growth. I have consistently been on the opposite side of this, forecasting growth would continue to come in below estimates and that so far is what has been happening.

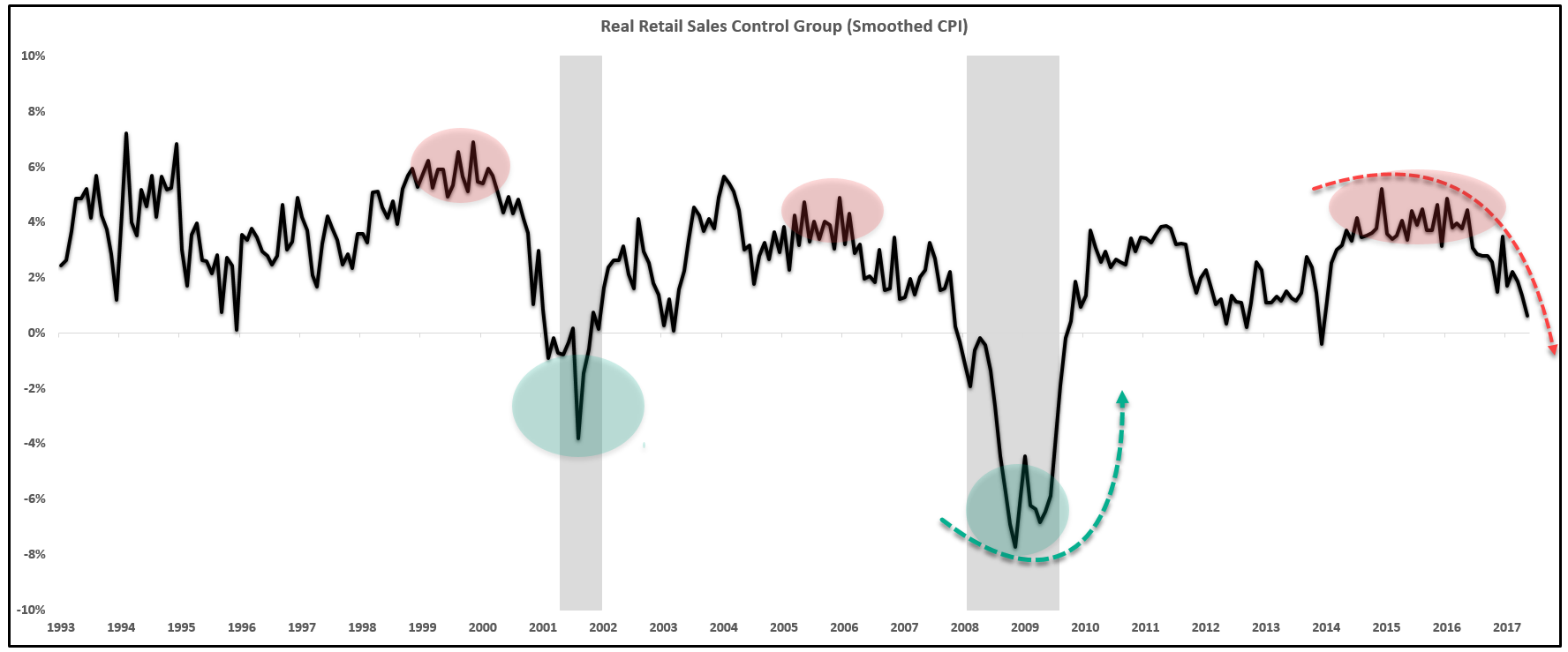

The retail sales control group, the number that feeds into GDP, declined to 2.48% year over year growth from 3.71% last month and down from 5.43% in January of this year.

Real Retail Sales:

(Source: Census Bureau)

(Source: Census Bureau)

Real retail sales is falling precipitously and approaching a dangerous level near the zero bound in growth. The last two times that this measure crossed into negative territory, a recession occurred. Based on the current data and the trending direction, it is very likely that retail sales will cross into negative territory over the next few months. This, of course, does not guarantee a recession but it clearly illustrates a very weak and worsening picture of the consumer and the economy.

Current Forecast:

My current forecast, mainly due to the severe weakness in wage growth, is for the economy to surprise investors to the downside and continue to slow over the second half of the year. Growth will be under 1.5% for the second half of the year.

Now is the time, especially with stock valuations near the highest level in history, to position as defensively as possible.

The asset allocation that I will update below outlines the defensive allocation I recommend for the current macro environment.

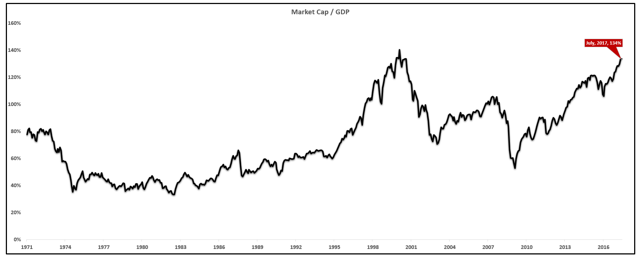

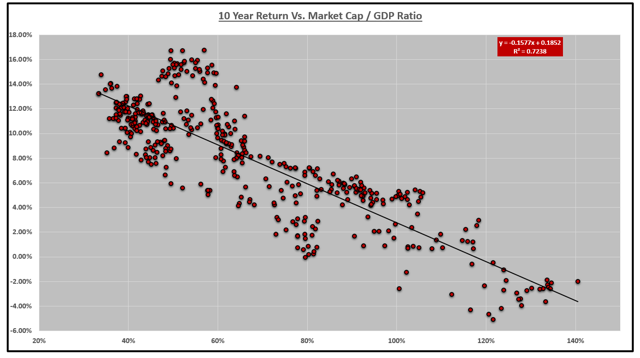

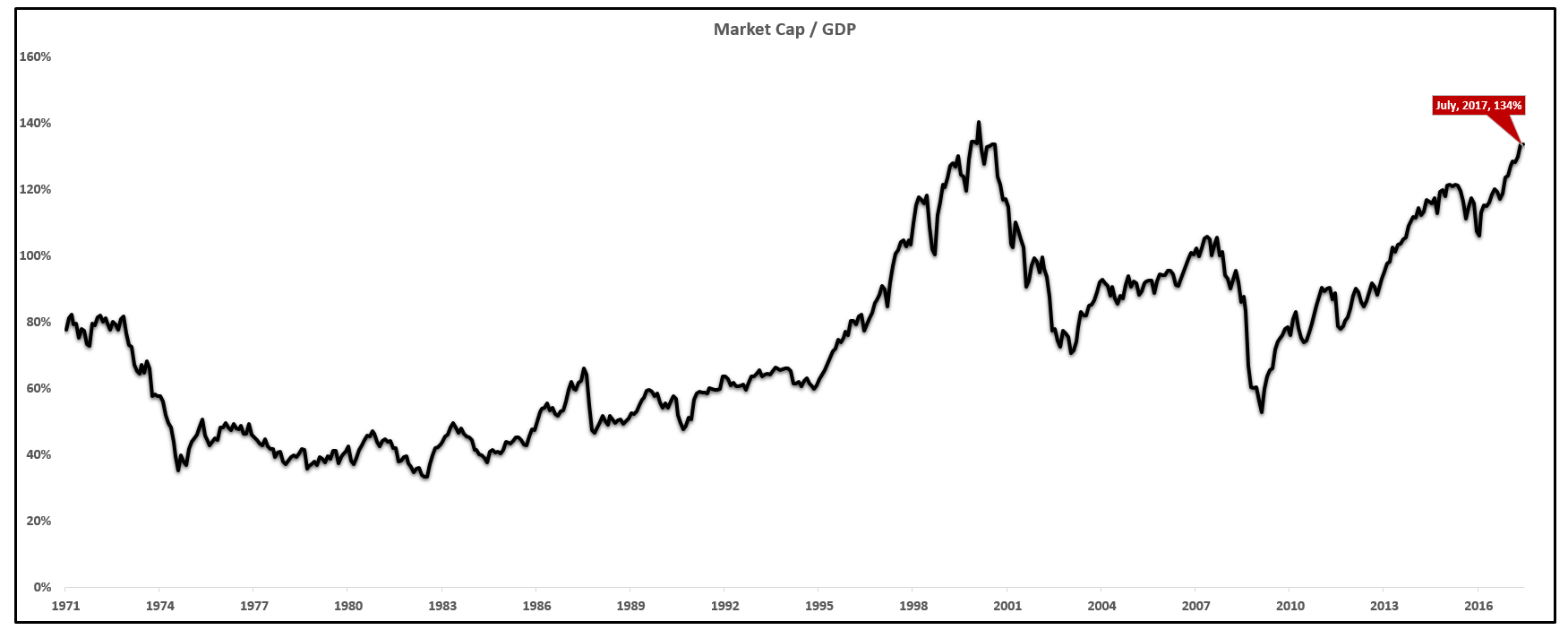

MarketCap to GDP Ratio:

(Source: Ycharts)

(Source: Ycharts)

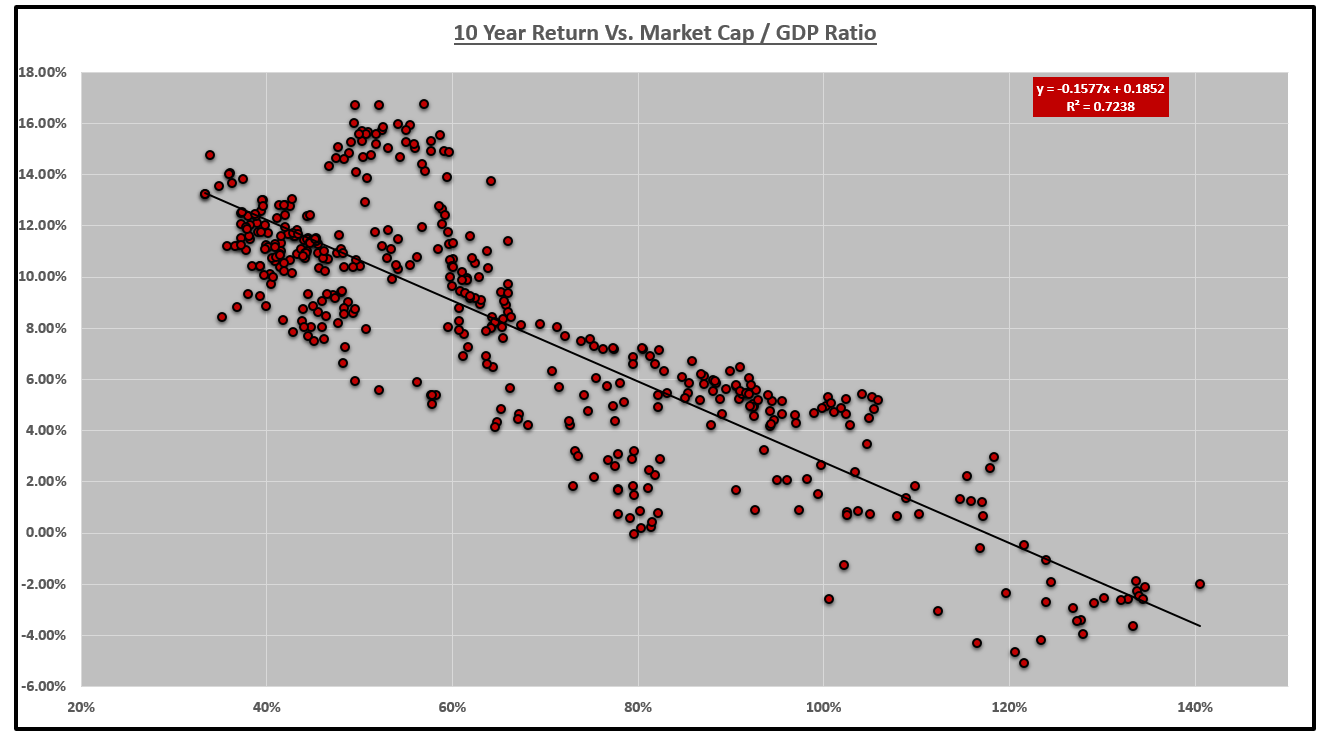

You can see we are near the highest level of valuations for stocks. Starting in 1970, if you run a regression between the value of this ratio and the future 10-year annualized return for stocks, the negative correlation between this ratio and stocks is clear with an R2 of over 0.73, a strong reading.

Regression:

(Source: Ycharts)

(Source: Ycharts)

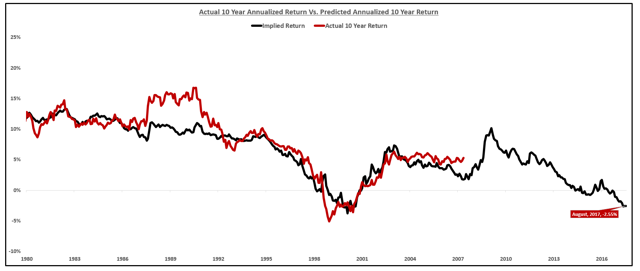

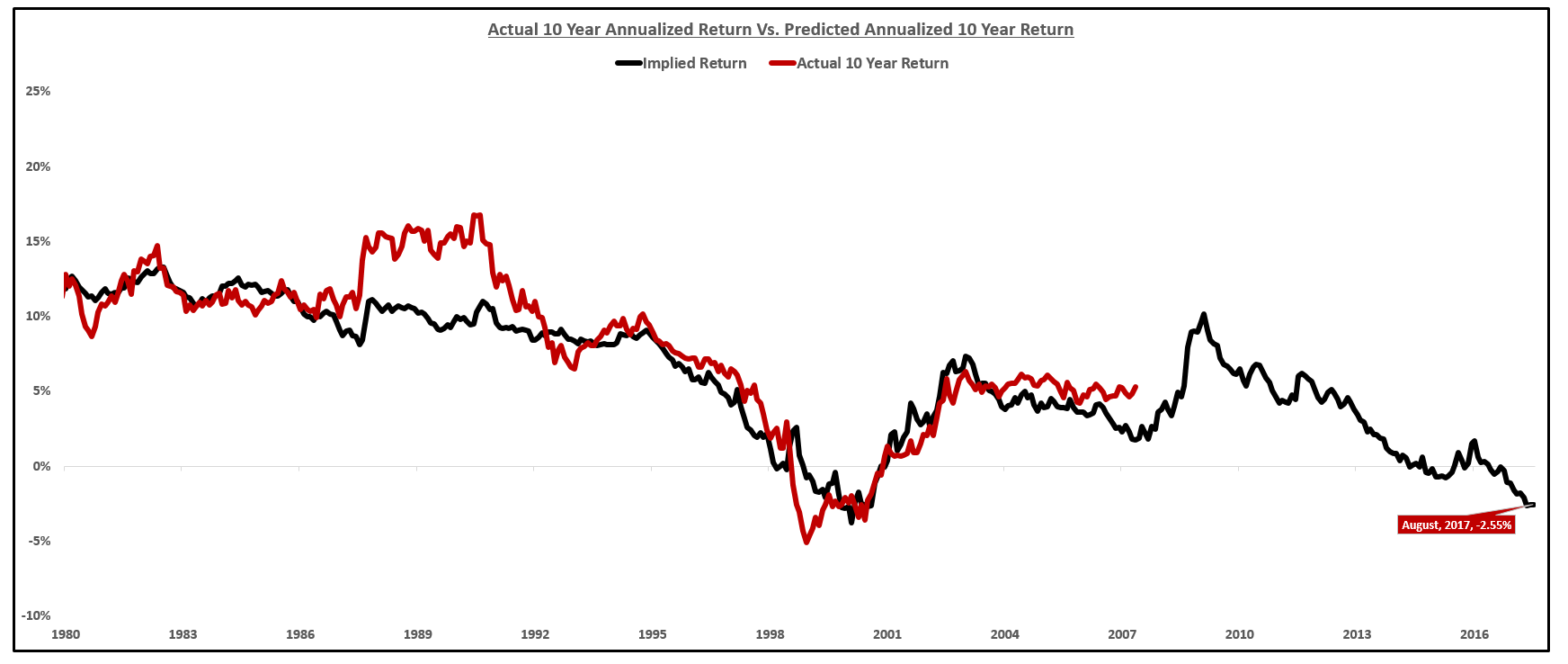

You can then take the " Y = " formula in the chart above to imply future 10-year annualized stock returns based on today's market cap to GDP. I plotted the implied returns (calculated with the y= formula above) and the actual 10 year annualized returns that have materialized below:

Implied 10 Year Annualized Return Vs. Actual Return:

This chart shows what return you can expect over the next 10 years based on the valuation at which you bought stocks. For example, the chart implies your return will be over 12% annualized if you bought stocks in 2009. (We won't know until 2019 if this held true.) Also, this shows that buying stocks today does not offer a promising return over the next 10 years. The only time a lower return was implied was when this metric properly warned of the future returns for stocks during the dot-com bubble.

From 1997-2001, this was implying negative returns for stocks. It ultimately came true, but for the first 3 years, you certainly looked foolish for being out of stocks. After the mean reversion, you looked quite smart to be out of stocks.

Before moving on, I also want to make it clear that using this metric will ensure you are not fully invested at market peaks and will give you a reasonable shot at diving in during market bottoms.

However, you will likely underperform during the last 1-2 years of a bull market. If you believe you can ride the market until the end, get out at the top and get back in, more power to you. If you don't think you can do that, let me offer an idea for a portfolio that backtests with great results, outperforming the market over the last ~40 years with less volatility and lower draw-downs.

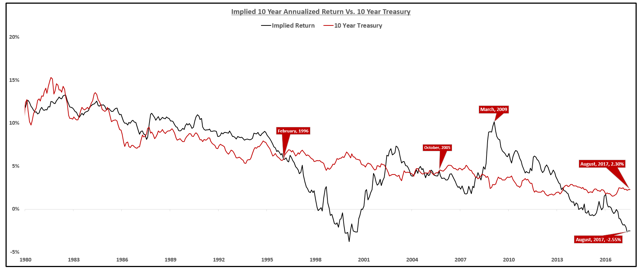

As many followers are aware, the premise for the portfolio is fairly straight forward. If the expected return for stocks is greater than the 10-year interest rate, be overweight stocks. If the expected return for stocks is below the 10-year treasury rate, be overweight bonds. Always keep roughly a 5%-10% allocation to gold to protect against inflation.

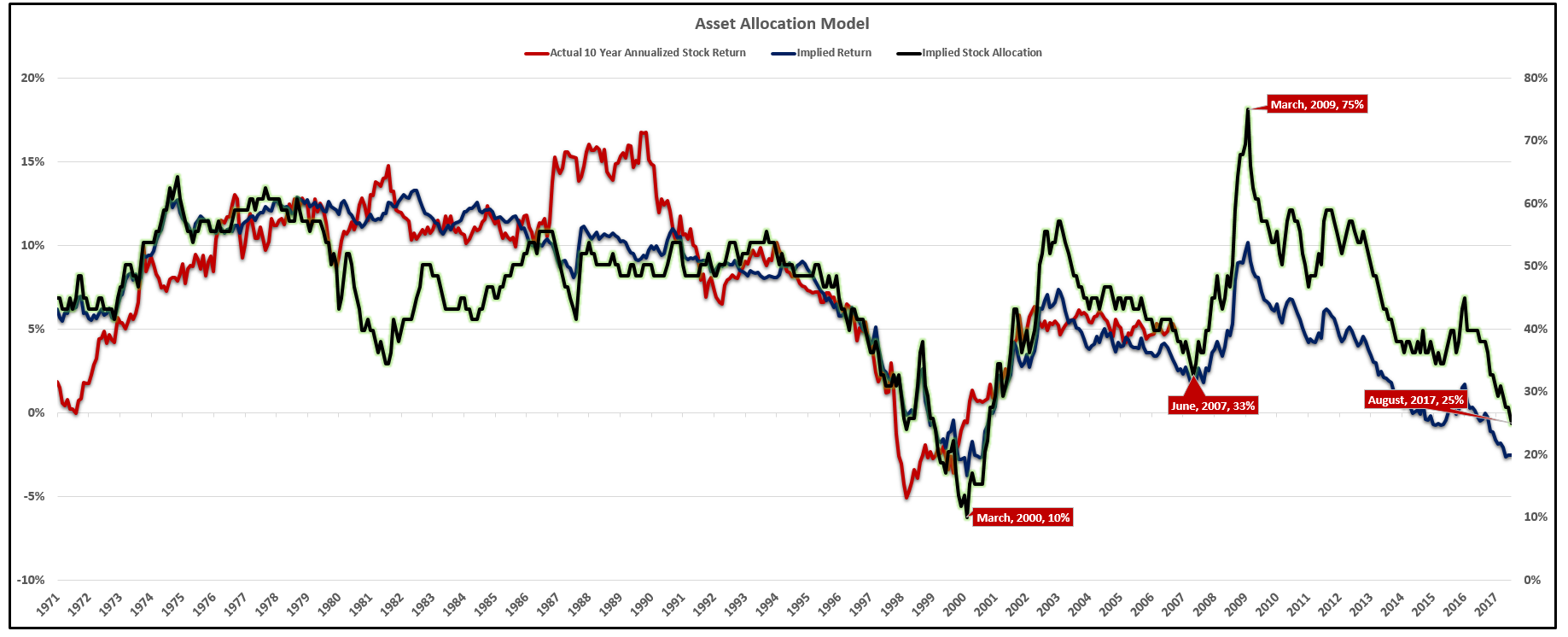

I mapped the 10-year expected return for stocks against the 10-year interest rate. You can see the years that you would have been overweight bonds (when the red line is above the black line). I noted key years and transition periods in the market.

Implied Return Vs. 10 Year Treasury Rate:

(Source: Ycharts)

(Source: Ycharts)

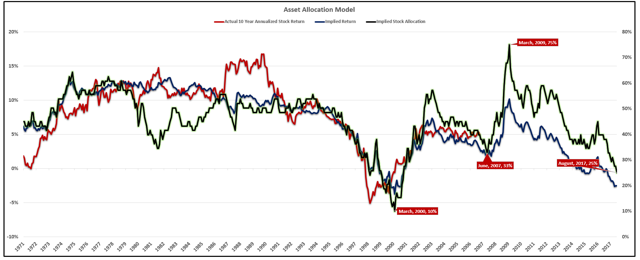

I take the above chart one step farther on overlay what my model suggests the proper equity exposure to be at different periods of valuations.

The chart below shows the lowest exposure to equities in March 2000 and the highest exposure to equities in March 2009.

Implied Stock Allocation:

Currently, the model is suggesting only a 25% allocation to stocks due to the low expected return over the next 10 years and also the relative expected return on stocks compared to the 10-year interest rate.

Although it can be hard to be underweight stocks while the market continues to run higher, the data shows it is likely your best bet.

My Asset Allocation for August 2017 is disclosed on my Marketplace Service.

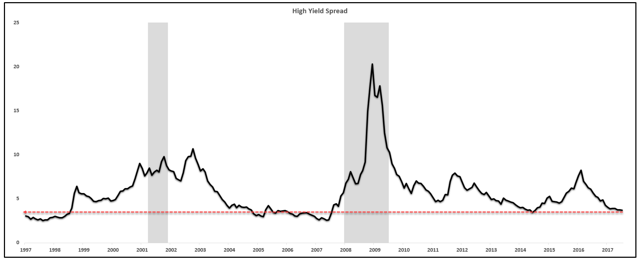

Adding Short High Yield Bonds:

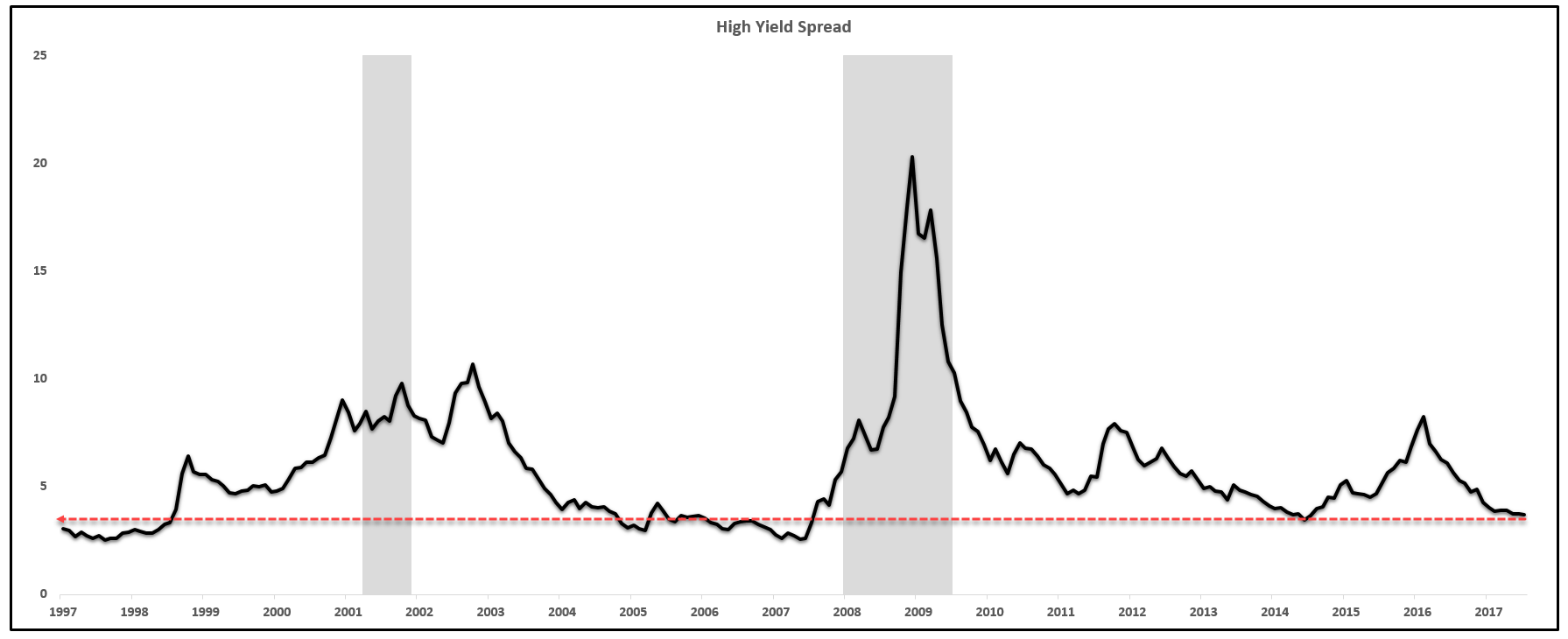

The spread between the interest rate on the treasury bonds on high yield bonds offers good insight into the markets feeling towards the safety of junk grade credit.

Right now, credit spreads are near the tightest levels ever indicating the market sees little risk in owning high yield bonds over treasury bonds.

The Spread Is Too Tight:

(Source: Bank of America)

(Source: Bank of America)

The biggest market theme that is ultimately causing the slow down in the economy, and soon the stock market, is the inability of wage growth to outpace shelter inflation. For the past several years wage growth has been muted and the consumer was able to eek out 1.5%-2% growth in wages after adjusting for rent or shelter inflation. This is why the economy has grown in that same range of 1.5%-2% for the past several years as well.

As of the past year or so, that trend has become decidedly worse as the consumer is now underwater.

Wage growth - rent inflation has been negative or just above zero for many months signaling that there is no marginal growth coming in the near future from the consumer. Many have brushed this off, foolishly in my opinion, but now the adverse effects of negative wage growth are starting to appear.

I will run through the following categories of data, bulleted below, and outline the changes from last month and the trends of each sector moving forward.

- Labor & Wages

- Auto Sales

- Housing & Real Estate

- Consumption

- Current Forecast

Macro Data Summary

Below is a running macroeconomic data table I track and regularly publish.

The data table contains roughly the 30 important macro data points that are released each month. The table shows the current growth rate as well as the growth rate last month, six months ago, and one year ago.

Aggregate Economic Table for July 2017:

The reason for this is to indicate clearly if growth is getting better or getting worse and as the table clearly shows, on balance, the data is getting worse.

I will start with labor and wages and work through the other segments of the economy.

Labor & Wages:

Nonfarm payrolls growth continues to trend downward after the peak in 2015 with some month to month volatility. The trending direction of the year over year growth in nonfarm payrolls is still overwhelmingly lower.

Nonfarm Payrolls Year over Year:

(Source: BLS)

(Source: BLS)This past month showed another deceleration in the rate of growth in nonfarm payrolls declining to 1.55% from 1.61% a month prior. This is a fairly significant month to month decline.

Growth in employment has been slowing for over two years. As employment growth slows, the growth in total wages earned slows as well. Wages are the driving factor behind all consumption.

Real Aggregate Wages (12 Month Average Inflation) Year over Year:

(Source: BLS)

(Source: BLS)Real aggregate earnings is the most important metric to follow as it measures the growth in real dollars earned for the entire economy. The measure of real aggregate earnings is very closely tied to the growth rate of the economy.

Currently, the 12-month average of real aggregate wage growth is 2.4% and falling, right in line with the growth rate of the economy of about 2%.

Real Aggregate Wages (Minus Rent Inflation) Year over Year:

(Source: BLS)

(Source: BLS)The inflation in rent and housing has been squeezing consumers, and the past 12 months, consumers have barely been able to break-even and show growth above 0% after housing costs.

Wages & Salaries - Rent Inflation Year over Year:

(Source: BEA)

(Source: BEA)Wages and salaries - rent inflation is severely negative which is signaling immediate distress to the consumer. In fact, the only time this metric was negative during the past 30 years was in recessions so it's current standing at -1.1% is very alarming.

This negative growth in wages cannot be shrugged off anymore because the adverse effects are bleeding into headlines left and right.

Credit card charge offs are rising at most credit providers as seen in the chart below.

Charge Offs:

(Source: WSJ)

(Source: WSJ)All of this is happening while the economy is supposedly at 'full employment'. If the economic data is deteriorating this rapidly under full employment, a slow down in the labor market has the potential to amplify these trends.

Autos is another area that the stressed consumer is appearing.

Auto Sales:

Total vehicle sales (autos, light trucks, heavy trucks etc.) marked another quarter of negative growth at -2.16% year over year. This sector should be sounding alarms for everyone.

Total Vehicle Sales Year over Year:

(Source: BEA)

(Source: BEA)Auto sales are collapsing at -14% year over year.

Auto Sales Year over Year:

(Source: BEA)

(Source: BEA)You can expect this trend to continue. If wage growth is negative after housing costs, there is no money left to purchase new vehicles. This could be a problem area for the market in the near future. I would avoid stocks related to the auto sector at all costs.

Real Estate:

The National Association of Home Builders publishes the 'Housing Market Index' each month which gauges the sentiment of a panel of homebuilders who sit on the board of the NAHB.

Respondents are asked to measure their feeling on the housing market as "good", "fair", or "poor".

If all panelist respond "good", then the index is 100. If all answer "poor", then the index is 0.

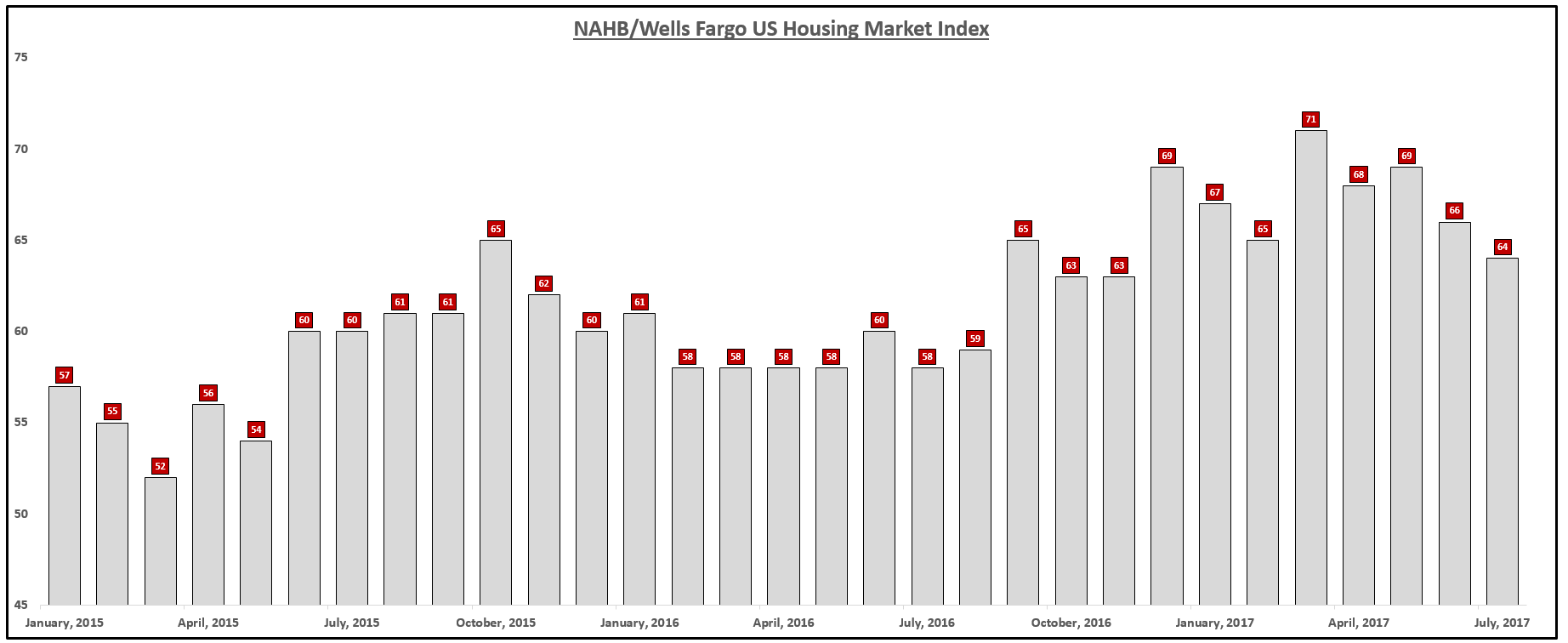

For July, the Housing Market Index declined to 64 from 66 a month ago and 67 six months ago.

Housing Market Index:

(Source: NAHB)

(Source: NAHB)There was a large jump after the election in all confidence based surveys due to increased hopes for reduced regulations, tax cuts and more. The longer these policies are delayed and the more they look unlikely, the more the real weakness in the economy is in focus and that is not a tailwind for housing.

July's Housing Market Index was very weak across the board which signals that the change in sentiment is not regional but broad based.

Here are all the components of the report.

Housing Market Index Breakdown:

(Source: NAHB)

(Source: NAHB)You can easily see that all but two categories were worse than last month and every category was worse than 6 months ago. The Trump fueled enthusiasm is fading.

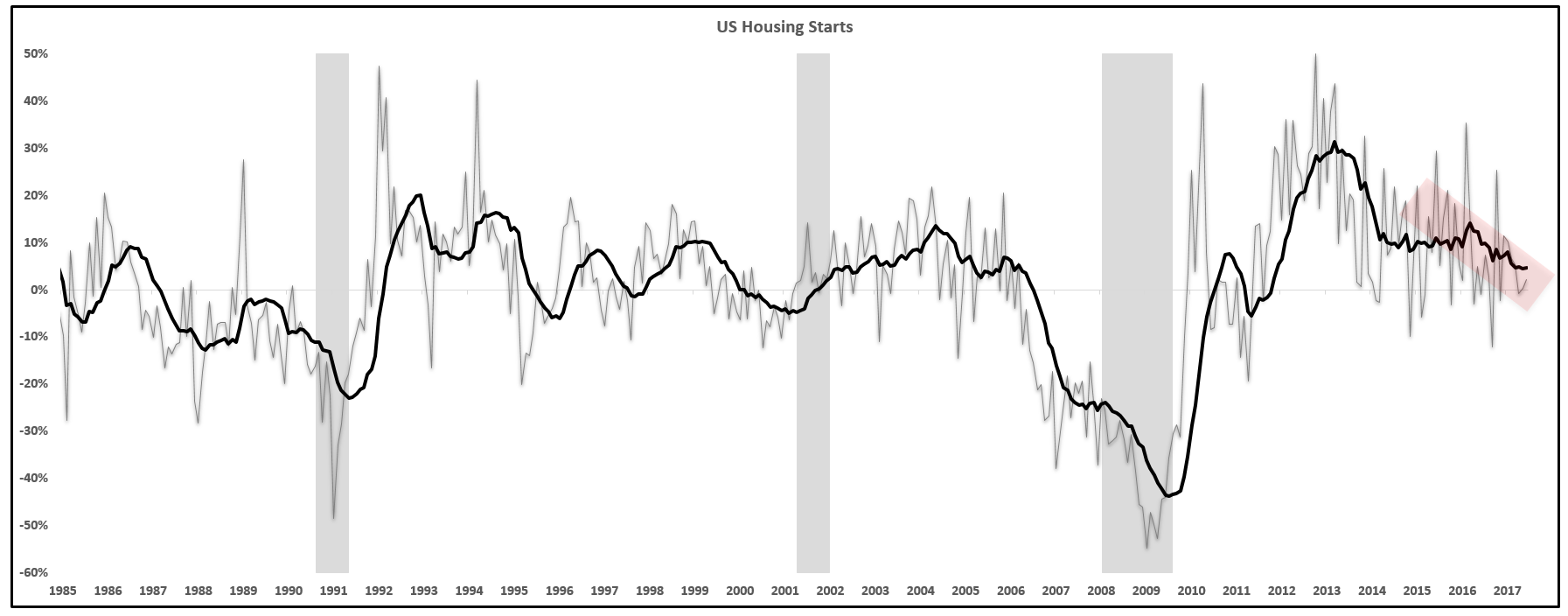

Housing starts are the number of new residential construction projects that have begun during any particular month. The New Residential Construction Report, commonly referred to as "housing starts," is considered to be a critical indicator of economic strength.

Housing starts had a massive rate of growth in 2013. That growth rate fell off but rebounded from 2015-2016. That growth rate is now rolling over and resuming the longer run down trend from the 2013 peak.

Housing Starts:

(Source: Census Bureau)

(Source: Census Bureau)The growth in Housing starts is at a multi-year low while home prices are at a multi-year high...

The Existing-Home Sales data measures sales and prices of existing single-family homes for the nation overall, and gives breakdowns for the West, Midwest, South, and Northeast regions of the country. These figures include condos and co-ops, in addition to single-family homes.

This past month's report on Existing Home Sales showed a decline in the growth rate to just 0.73%. The volume of transactions is really drying up based on the data.

A growth rate of 0.73% is lower than last month, six months ago, and a year ago making the downward trend clear.

Existing Home Sales:

(Source: NAR)

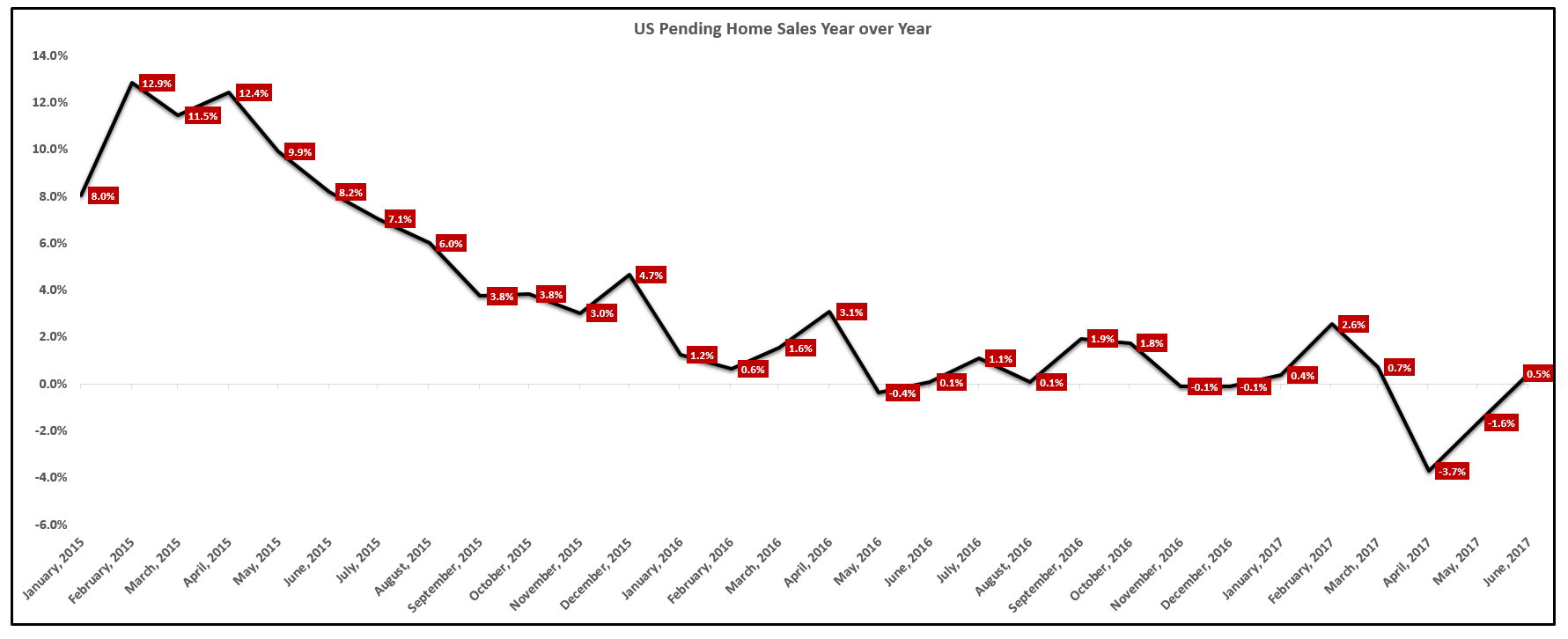

(Source: NAR)Pending Home Sales (PHS), published by the National Association of Realtors (NAR), represent signed contracts for new homes, not closes. PHS typically leads Existing Home Sales (90% of the housing market) by about two months.

Pending home sales have been unchanged for two years.

Pending Home Sales Unchanged:

(Source: NAR)

(Source: NAR)I continue to be perplexed by the mainstream bullishness on housing despite truly lack luster data.

When looking at Pending Home sales growth, the trend is falling as well.

Pending Home Sales:

(Source: NAR)

(Source: NAR)The two notable areas are the Midwest and West markets where Pending Home sales growth has been negative for several months in a row. Due to the lead in Pending Home sales vs. Existing Home Sales, I expect there to be a rough patch ahead in these two markets in the next few Existing Home sales reports.

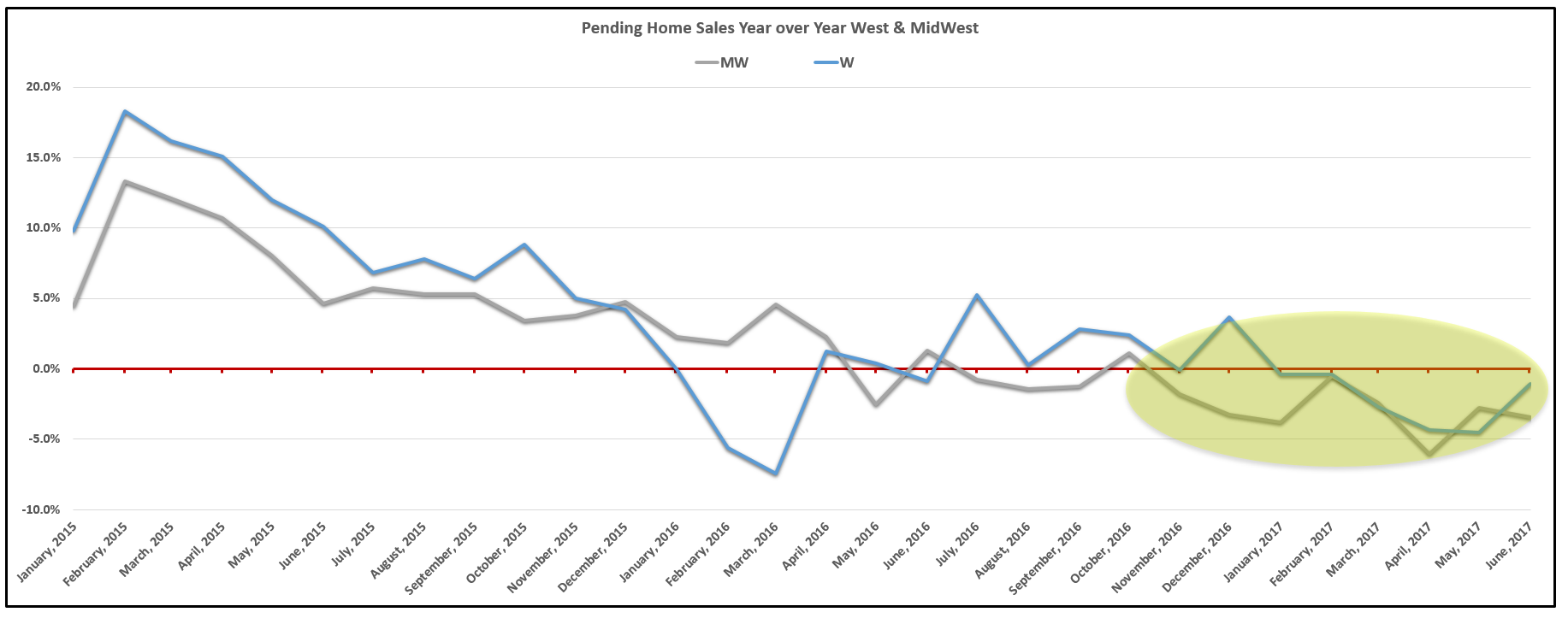

Pending Home Sales West & Midwest:

(Source: NAR)

(Source: NAR)In the housing market, there are two types of homes; Existing Homes and Newly Constructed homes.

Existing Home sales make up roughly 90% of the housing sale volume while New Home sales is about 10%.

Lately, there has been a divergence in the price growth of these two markets. The price of newly built homes is falling at -3.4% year over year as of the last report while the price of EHS is soaring, up nearly 6% year over year.

How do you explain this divergence in the market?

National Home Price Index Year over Year:

(Source: Dow Jones, S&P)

Below is a chart showing the year over year growth in the median sales price for new homes. You can see the trend (black line) is sharply lower and the last data point (grey line/yellow circle) was negative.

Median Price of New Homes Year over Year:

Many talk about rising prices in the housing market but actually when you look at the details and all the reports, only the price of Existing Home sales is rising, New Home sales prices are falling and falling quite rapidly...

The chart below is a quick reference on existing home price growth. It shows the current year over year growth rate by city as well as the growth rate last month, 6 months ago, and 1 year ago. This is an easy way to see the current growth rate and if that growth rate is accelerating or decelerating.

Home Price Table:

(Source: Dow Jones, S&P)

(Source: Dow Jones, S&P)Many of the cities that showed slower growth have now posted two or three consecutive months of deceleration.

Two or three months of home price growth deceleration is not enough to change the trend. For now, the trend of home price growth is still clearly higher.

I have outlined how home prices growing faster than wages is unsustainable and how wage growth has to increase or home price growth has to fall (this article, here, outlines that dynamic in detail).

When looking at the weakness in wages, the multi month deceleration in the national home price growth and the broad month to month deceleration in the majority of cities, the picture on home prices becomes something to keep a close eye on.

Commercial Real Estate prices are on the verge of posting the first year over year decline since 2007 and only the third time in nearly 30 years.

Commercial Real Estate Prices:

(Source: GreenStreetAdvisors)

(Source: GreenStreetAdvisors)This is an area of the market to keep a close eye on as it poses a significant risk to the market.

Consumption:

Retail sales for the June reporting period were very weak and caused even the most optimistic analysts to question the prospects for high economic growth. I have consistently been on the opposite side of this, forecasting growth would continue to come in below estimates and that so far is what has been happening.

The retail sales control group, the number that feeds into GDP, declined to 2.48% year over year growth from 3.71% last month and down from 5.43% in January of this year.

Real Retail Sales:

(Source: Census Bureau)

(Source: Census Bureau)Real retail sales is falling precipitously and approaching a dangerous level near the zero bound in growth. The last two times that this measure crossed into negative territory, a recession occurred. Based on the current data and the trending direction, it is very likely that retail sales will cross into negative territory over the next few months. This, of course, does not guarantee a recession but it clearly illustrates a very weak and worsening picture of the consumer and the economy.

Current Forecast:

My current forecast, mainly due to the severe weakness in wage growth, is for the economy to surprise investors to the downside and continue to slow over the second half of the year. Growth will be under 1.5% for the second half of the year.

Now is the time, especially with stock valuations near the highest level in history, to position as defensively as possible.

The asset allocation that I will update below outlines the defensive allocation I recommend for the current macro environment.

Updates to the Asset Allocation Model

Often called "Warren Buffett's favorite valuation metric," the market cap to GDP ratio takes the cumulative market cap of the Wilshire 5000 stock index divided by the current GDP. This ratio gives you an idea of how the valuation of stocks is growing relative to the overall economy. Higher ratios indicate higher valuations for stock prices.MarketCap to GDP Ratio:

(Source: Ycharts)

(Source: Ycharts)You can see we are near the highest level of valuations for stocks. Starting in 1970, if you run a regression between the value of this ratio and the future 10-year annualized return for stocks, the negative correlation between this ratio and stocks is clear with an R2 of over 0.73, a strong reading.

Regression:

(Source: Ycharts)

(Source: Ycharts)You can then take the " Y = " formula in the chart above to imply future 10-year annualized stock returns based on today's market cap to GDP. I plotted the implied returns (calculated with the y= formula above) and the actual 10 year annualized returns that have materialized below:

Implied 10 Year Annualized Return Vs. Actual Return:

This chart shows what return you can expect over the next 10 years based on the valuation at which you bought stocks. For example, the chart implies your return will be over 12% annualized if you bought stocks in 2009. (We won't know until 2019 if this held true.) Also, this shows that buying stocks today does not offer a promising return over the next 10 years. The only time a lower return was implied was when this metric properly warned of the future returns for stocks during the dot-com bubble.

From 1997-2001, this was implying negative returns for stocks. It ultimately came true, but for the first 3 years, you certainly looked foolish for being out of stocks. After the mean reversion, you looked quite smart to be out of stocks.

Before moving on, I also want to make it clear that using this metric will ensure you are not fully invested at market peaks and will give you a reasonable shot at diving in during market bottoms.

However, you will likely underperform during the last 1-2 years of a bull market. If you believe you can ride the market until the end, get out at the top and get back in, more power to you. If you don't think you can do that, let me offer an idea for a portfolio that backtests with great results, outperforming the market over the last ~40 years with less volatility and lower draw-downs.

As many followers are aware, the premise for the portfolio is fairly straight forward. If the expected return for stocks is greater than the 10-year interest rate, be overweight stocks. If the expected return for stocks is below the 10-year treasury rate, be overweight bonds. Always keep roughly a 5%-10% allocation to gold to protect against inflation.

I mapped the 10-year expected return for stocks against the 10-year interest rate. You can see the years that you would have been overweight bonds (when the red line is above the black line). I noted key years and transition periods in the market.

Implied Return Vs. 10 Year Treasury Rate:

(Source: Ycharts)

(Source: Ycharts)I take the above chart one step farther on overlay what my model suggests the proper equity exposure to be at different periods of valuations.

The chart below shows the lowest exposure to equities in March 2000 and the highest exposure to equities in March 2009.

Implied Stock Allocation:

Currently, the model is suggesting only a 25% allocation to stocks due to the low expected return over the next 10 years and also the relative expected return on stocks compared to the 10-year interest rate.

Although it can be hard to be underweight stocks while the market continues to run higher, the data shows it is likely your best bet.

My Asset Allocation for August 2017 is disclosed on my Marketplace Service.

Adding Short High Yield Bonds:

The spread between the interest rate on the treasury bonds on high yield bonds offers good insight into the markets feeling towards the safety of junk grade credit.

Right now, credit spreads are near the tightest levels ever indicating the market sees little risk in owning high yield bonds over treasury bonds.

The Spread Is Too Tight:

(Source: Bank of America)

(Source: Bank of America)Due to the slowdowns, I outlined in the economic data above, that the market has clearly not priced in, I expect credit spreads to widen. Even if spreads widen just to historically average levels, high yield bonds will fall in price which makes JNK an attractive opportunity on the short side.

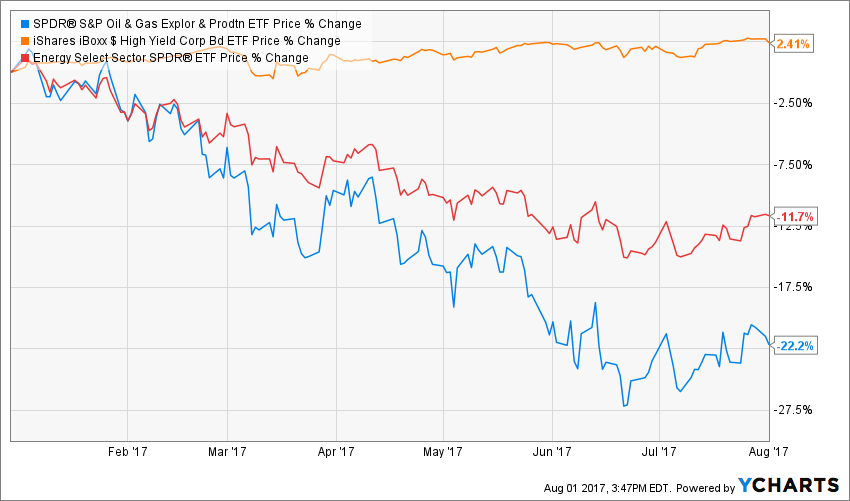

Another reason to believe that credit spreads will widen is due to the price action in energy stocks.

High yield bonds have a heavy weighting in the energy space.

What is interesting is that the energy related stocks have been tumbling, some down over 20% just this year, and high yield credit has seemingly ignored this.

Why Isn't Credit Reacting?:

This will not last if oil continues its trend lower.

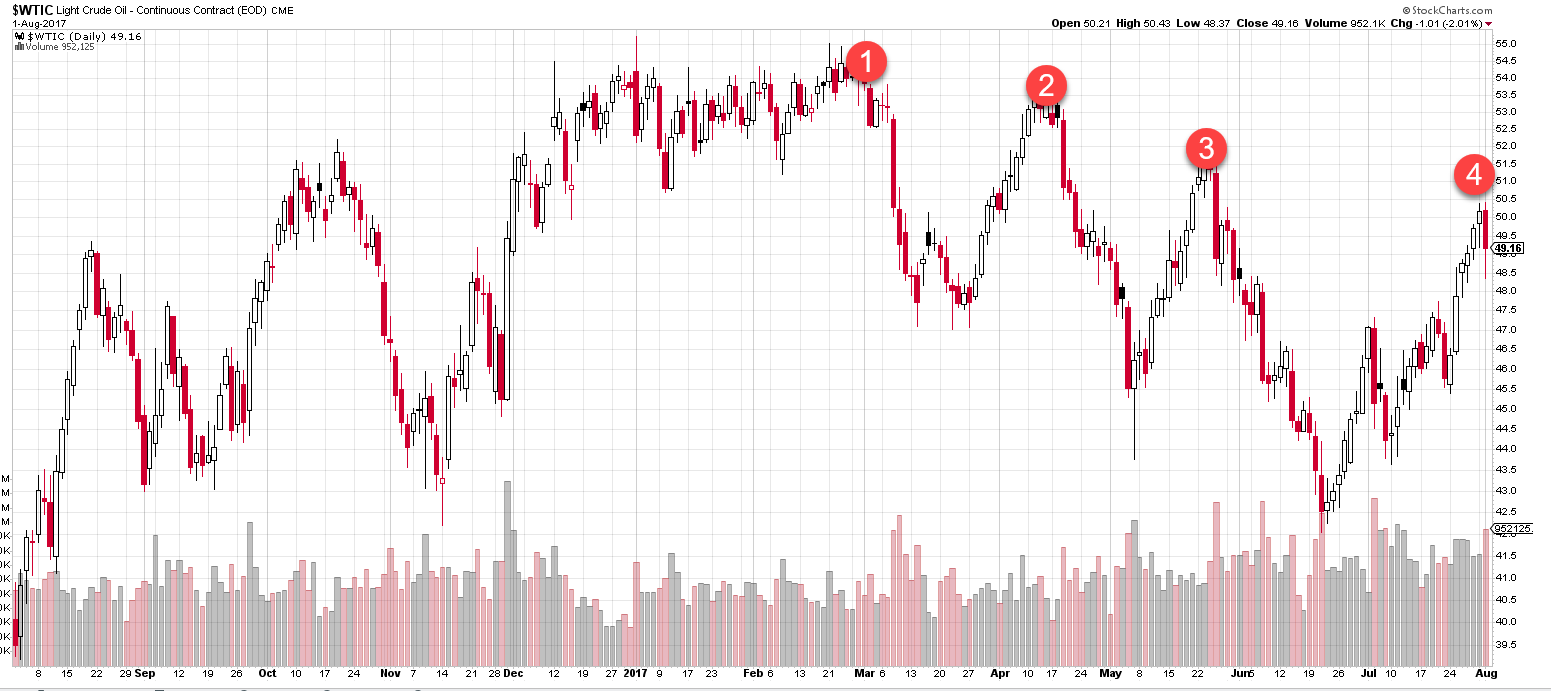

I believe that falling oil price, down to the $40 dollar level is the catalyst needed to cause high yield spreads to widen making JNK a profitable short.

The set up for oil appears to be making another top and heading down to the $40 level which is why I chose to add the short JNK position this month.

Oil Next Leg Lower?:

(Source: StockCharts)

(Source: StockCharts)I expect to hold this JNK position for as long as needed for the adverse effects of the slowing economic data to flow into the market which should cause high yield bonds to re-price to a more historically average spread above treasury rates.

0 comments:

Publicar un comentario