Buttonwood

Tech stocks have regained their dotcom-era highs

But the sector has changed a lot since the last peak

.

CAST your mind back to when Bill Clinton was president, Tony Blair and Vladimir Putin were fresh-faced new leaders and tweeting was strictly for the birds. That was when technology stocks, as measured by the S&P 500 tech index, last traded at their current levels.

The horrendous decline in share prices that followed the peak in 2000 was the first financial calamity of this millennium. The dotcom crash had much less impact on the broader economy than the mortgage and banking crisis of 2007-08. Nevertheless, the tech revival has caused some twitchiness among investors. Might history be repeating itself?

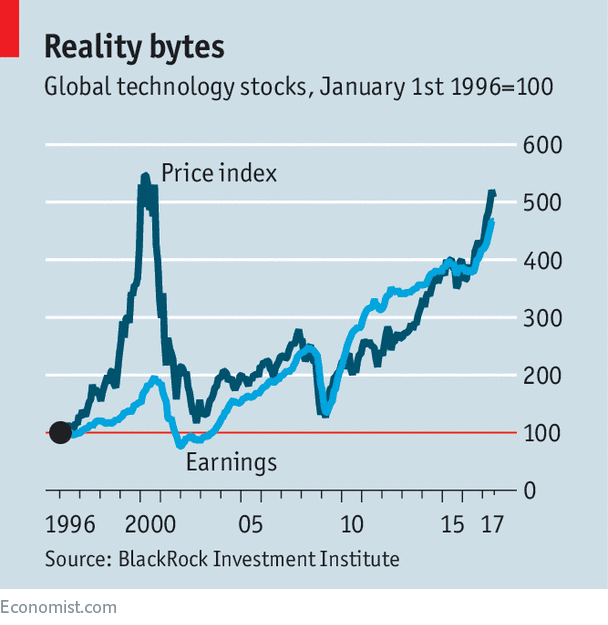

In the intervening years the world, and the tech industry, have changed a lot. In the late 1990s enthusiasm for tech shares was so great that the sector’s market value rose far faster than its earnings. The gap is nothing like as great today (see chart). Back then, leading firms like Microsoft and Oracle were valued at more than 20 times their annual revenues, let alone earnings. This time around, with the exception of Facebook, price-to-revenue ratios are much less stretched.

What boosted tech businesses in the late 1990s was that everyone was discovering the internet at the same time. Both companies and consumers were buying computers and associated items like modems. That led to rapid revenue growth. But the sudden enthusiasm for tech was also its greatest weakness; every college graduate seemed to have a plan to start a dotcom company. The market became overcrowded. Investors struggled to tell the long-term winners from the losers.

Since then, investors have focused their enthusiasm on companies that can exploit “network effects” and become dominant in their sector—Google in internet search, for example. The latest rally has been led by a small number of stocks, sometimes dubbed the FAANGs (Facebook, Amazon, Apple, Netflix and Google’s parent, Alphabet) and sometimes FAAMG (replacing Netflix with Microsoft). In June Goldman Sachs said this latter group had been responsible for 40% of the S&P 500 index’s gains in the year to that point. The tech industry was Wall Street’s best performer in the first half of the year.

Eddie Perkin of Eaton Vance, a fund-management company, says that investors started the year with too much enthusiasm for the “Trump trade”, the idea of owning stocks that might benefit from the new president’s policies. Companies with high tax bills, and those exposed to infrastructure spending, were two examples. As hopes for action from the new administration faded, enthusiasm for tech stocks surged; this industry can generate profits growth regardless of the economic outlook. Tech companies in the S&P 500 are likely to record double-digit year-on-year profits growth in the second quarter.

Earnings expansion on that scale means that few investors can afford to ignore tech stocks. Since 2009 the industry has been the most favoured by global fund managers for 80% of the time, according to a regular survey by Bank of America Merrill Lynch. But the latest survey reflected fears that the enthusiasm may have gone too far: 38% of managers thought that betting on tech stocks was the “most crowded trade”; a net 9% had cut their exposure in the previous month.

The risks facing the tech industry now are rather different from those that surfaced in 2000.

Then, it became clear that many companies would burn through their cash long before they made a profit. This time, the industry is more mature; Apple’s fastest growth is surely behind it, for example. Whereas the sector was generally held in high regard in 2000, it is now the object of more suspicion, whether it is public concern about individuals’ privacy, Donald Trump’s anti-Amazon tweets or EU fines against American tech giants. Regulation may yet prove a barrier to tech’s long-term growth.

So, history isn’t repeating itself exactly. There is nothing like the same stockmarket euphoria as there was at the turn of the century. Few people are trying to day-trade their way to riches or setting up a dotcom franchise to sell dog food. And tech stocks are not as much of an outlier as they were (along with media and telecoms firms) in 2000, when many investors abandoned “old economy” companies in retailing and heavy industry.

But there is still plenty that can go wrong. The overall market is on a cyclically adjusted price-earnings ratio of 30—a level surpassed only in 1929 and the late 1990s. If the Federal Reserve tightens policy too aggressively, or the American economy slips into recession (or both), tech investors will get that sinking feeling again.

0 comments:

Publicar un comentario