A Correction Is Already Under Way

by: Eric Parnell, CFA

- The headline U.S. stock market remains within striking distance of new all-time highs.

- Yet a correction is already underway under the market surface.

- Stocks currently have a "big" problem.

- Yet a correction is already underway under the market surface.

- Stocks currently have a "big" problem.

Many investors have been contemplating the potential for a U.S. stock market correction starting some time over the next couple of months after what has been a remarkable year to date. Whether such a pullback on the headline benchmarks actually comes to pass remains to be seen. But in many respects, a correction in U.S. stocks has already been underway for nearly a month now.

A “Big” Problem Across Markets

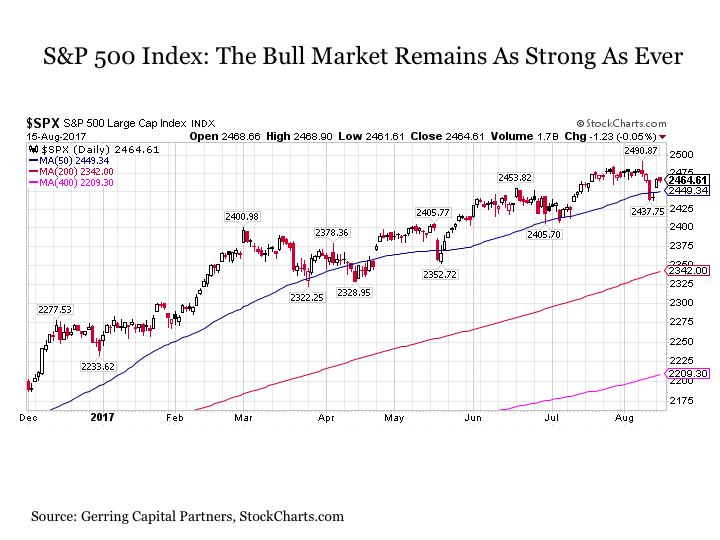

The U.S. stock market has a “big” problem. The S&P 500 Index (SPY) continues to perform exceptionally well. Through mid-August, the headline U.S. stock market benchmark continues to set fresh new all-time highs with each passing week. And the trend remains definitively higher even despite some moments of notable weakness in recent trading days. On the surface, the U.S. stock market looks as bulletproof as ever.

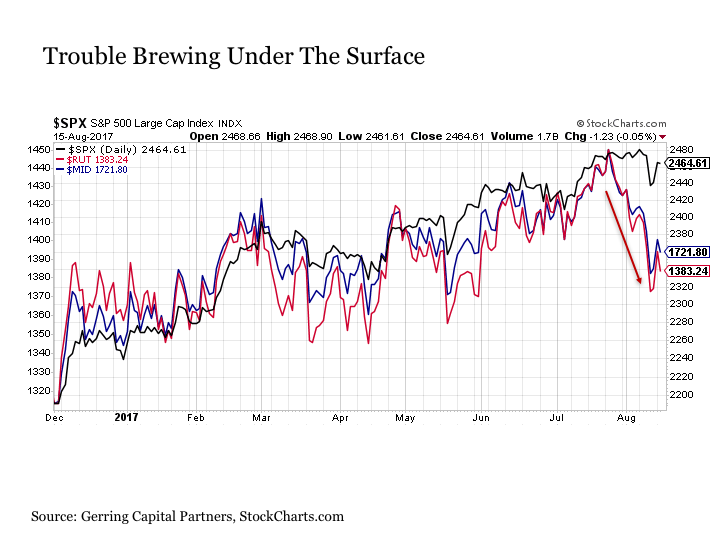

But a closer look under the market surface reveals that trouble for stocks has been brewing for several weeks now. Consider the following chart of the large cap S&P 500 Index (IVV) versus two of its closely related U.S. counterparts – the mid-cap S&P 400 Index (IJH) and the small cap Russell 2000 Index (IWM) dating back to December of last year.

Each U.S. market segment has moved with a very high correlation with one another. That is up until just a few weeks ago. For while the headline S&P 500 Index (VOO) continues to make its way to the upside, both mid-cap and small-cap stocks have turned definitively lower. This is a notable deviation across the size spectrum in the U.S. stock market.

Zooming in on the recent weeks reveals the magnitude of the situation over the last few weeks.

While the S&P 500 Index has held roughly flat dating back to July 25, both the mid-cap S&P 400 and the small-cap Russell 2000 have declined by as much as -5%. Moreover, despite a solid bounce early Monday morning to start the week, the short-term trend remains definitively lower for both mid-caps and small caps.

Of course, a -5% pullback over the course of fifteen trading days is hardly anything that could be deemed as problematic. After all, prior to the financial crisis, a -5% correction in stocks along the way during a calendar year would be considered a part of normally functioning markets at any given point in time.

But in a broader market that has felt virtually no pain for so long, a comparable pullback in the S&P 500 Index from today’s high 2,400s range to the low to mid-2,300s over the course of a few weeks with little signs of relenting would likely be jarring for many, particularly given the complacency as implied by the historically low volatility (VXX) that continues to define today’s market backdrop.

What is also notable for U.S. stock investors is that while the S&P 500 Index is higher by as much as +4% since the start of March 2017, both the mid-cap S&P 400 and the small-cap Russell 2000 Index are now lower by nearly -1.5% over this same nearly six-month time period on a total returns basis. Hardly anything that could be described as resoundingly bullish.

Thus, it stands to wonder how much longer before the problems that have been plaguing the mid-cap and small-cap segments of the U.S. stock market finally start to make their way up through the large-cap ranks.

A “Big” Problem Within The S&P 500 Index

Evidence exists that this downside pressure is already making its way through the large-cap index itself.

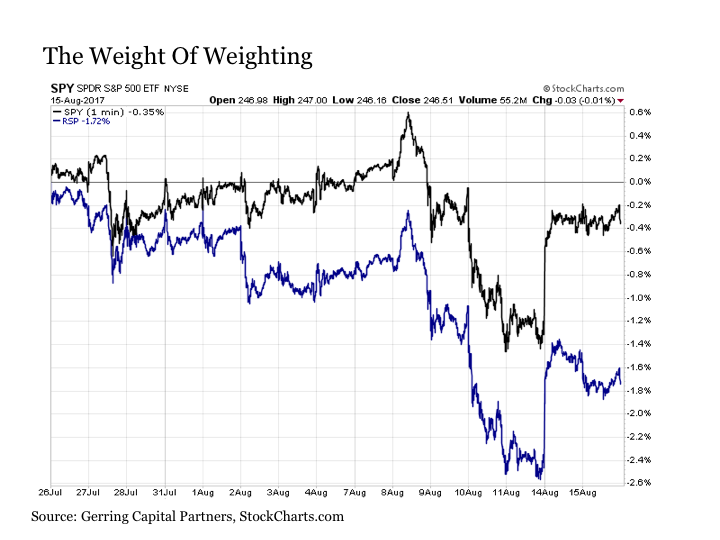

First, consider the performance of the market cap weighted S&P 500 Index where the top ten mega caps like Apple (AAPL), Microsoft (MSFT), Facebook (FB) and Amazon (AMZN) alone make up roughly 20% of the entire benchmark versus its equal weighted counterpart (RSP) where each of the 500 stocks has roughly the same 0.2% weighting.

Viewing this same market benchmark through these two different lenses reveals the following.

While the headline benchmark that is so heavily driven by its selected handful of largest stocks continues to hold its ground, the same index on an equal weight basis has been down by as much as -2.6% in recent days. Moreover, while the equal weighted market also bounced strongly at Monday’s open, the broader trend remains to the downside much like its mid-cap and small-cap counterparts.

Big Is Best, All Else Are The Rest

Let’s take this size assessment one step further. Consider the performance of the S&P 500 Index versus its even “bigger” stock counterpart in the Dow Jones Industrial Average (DIA) and its relatively smaller list of 30 mega cap components. While both had been moving closely together through late July, the Dow has been surging to the upside by as much as +2.6% over the last couple of weeks while the broader market as measured by the S&P 500 Index has turned flat and the rest of the market outside of the mega caps has turned definitely lower.

So What?

So, why does this all matter? So what that the largest stocks are carrying the entire weight of the market to the upside?

To begin, the fact that the headline benchmark continues to set new highs is obscuring the fact that problems have been festering over the last few weeks now that is causing the rest of the stock market to falter outside of a select group of very large companies. A market that is reliant on a small handful of names to pull it higher is not a healthy one. Big should not be best for a healthy market. Instead, breadth is typically best. For if these big names start to falter in their own right, the market is already lacking the many other names that can step in to help pick up the slack.

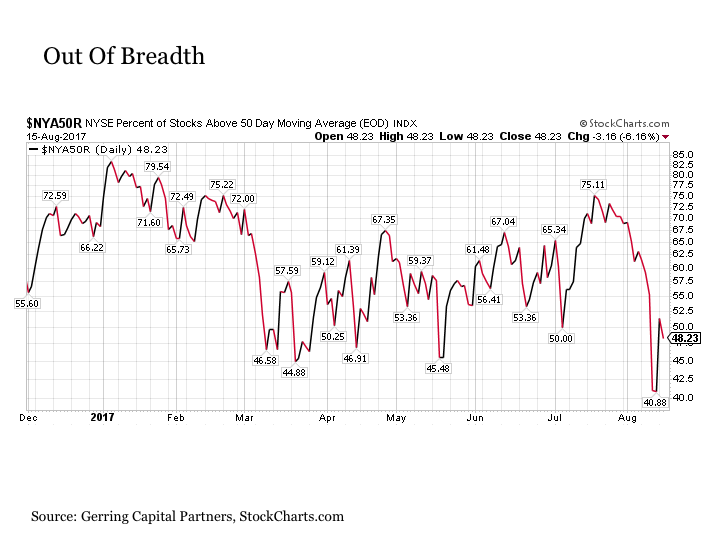

In regard to the breadth of market performance, it is as weak as it has been in some time despite the fact that the S&P 500 Index remains so close to new all-time highs. Today, less than 50% of stocks in the headline benchmark are trading above their 50-day moving average. This reading reached as low as 40% in recent trading days.

In addition, while the S&P 500 Index itself is within less than 1% from a new all-time closing high, it is notable that 17% of the stocks that make up the index, or 85 stocks, are officially in bear market territory in being down more than -20% from their recent highs, 38% (190) are in correction territory at down more than -10% from recent peaks and nearly two-thirds (65%, or 319 stocks) are more than -5% lower from recent highs.

None of these readings are signs of a market enjoying widespread health. Instead, they are indicative of a market that appears strong on the surface but is showing signs of sickness and deterioration underneath. How this manifests itself as we continue into what has historically been the most difficult two-month stretch for the U.S. stock market in September and October remains to be seen.

If nothing else, the challenges brewing under the surface of the market suggest that now is not the time for complacency when it comes to managing the risk in your U.S. stock portfolio, as investors should be prepared for a potential bout of increased volatility in the headline S&P 500 Index if the correction that has already been underway for several weeks across the rest of the market is any indication.

0 comments:

Publicar un comentario