The Ultimate Debt Bubble Is Upon Us

by: Zoltan Ba

- Since the last economic crisis, the Western World consumer's debt deleveraging has been the only major exception to broad debt accumulation.

- The only reason we were able to cope in the US and globally is because of the lower interest rates. That trend has now come to an end.

- While the broad nature of this debt bubble can give it more longevity as the burden is spread out, it can also make the next crash more painful.

- The only reason we were able to cope in the US and globally is because of the lower interest rates. That trend has now come to an end.

- While the broad nature of this debt bubble can give it more longevity as the burden is spread out, it can also make the next crash more painful.

According to the US debt clock, the country pays about $2.5 trillion annually in interest expenses, within the context of an economy that has a GDP of about $19 trillion. What this means is that about 13% of the economy goes to servicing debt expenses. This of course also means that on the other side of the equation, somebody else gains an income from those interest expenses, so it is seemingly not all bad. Nevertheless, it is a problem when the interest/GDP ratio tends to grow, because the interest collecting institutions or individuals are not necessarily the ones who will contribute to consumer demand. A bank will take those interest revenues and put them towards creating lending capacity for consumers, but it will not go out and purchase houses, cars, or furniture for itself. It means that in the end, most consuming entities are paying more and more on interest, which means that we can afford less of everything else. And, when most people, companies, and governments have to settle for less of everything else, we end up experiencing an economic contraction, unless we substitute with even more debt, which leads to more interest on debt. Within this context, the burning question of our time has to be how much of an interest payment load we can bare, in the US, and globally, given that there are signs of central banks looking to tighten in order to prevent asset bubbles. Unfortunately, there is no way of knowing what that answer is until we will see this latest debt bubble burst.

Based on the debt clock data, total US debt outstanding at all levels of the economy, including governments, mortgages, corporate, business, and consumer debt stands at about $67.5 trillion.

The interest rate we therefore pay on the economy as a whole is somewhere in the 3.7% range, based on the $2.5 trillion in total interest figure. Based on the fact that back in 2007, 10-year bond yields were around 4.5%, mortgage rates were around 6.5%, we can assume that the average interest yield on the economy as a whole may have been about 6-7%, given other high-yield debts, such as credit cards. Going on this assumption, total interest on debt throughout the economy may have reached as high as 20% of GDP, just before the crash, according to data on total debt from that period, which can be found on Economics Help.

The total debt/GDP ratio reached over 300% by the time the crisis reached full-blown status and the economic contraction became severe in 2009. In the run-up to the crisis, it was about the same as it is now, or about 270-280%. Therefore, it is important to highlight the fact that the current decline in interest on the economy to about 13%/GDP from the high of as much as 20% before the crisis hit is mostly due to the years we had of people, businesses, and governments refinancing old debts at lower rates for the past seven years or so, as well as taking out new debt at much lower rates. After years of re-financing at the recent, historically very low costs, the trend is now coming to an end. In effect, there is no realistic way to take interest rates significantly lower from current levels, and as we can see lately, central banks are increasingly looking at moving rates up, even if it is not going to get back to average levels seen in the previous economic cycle.

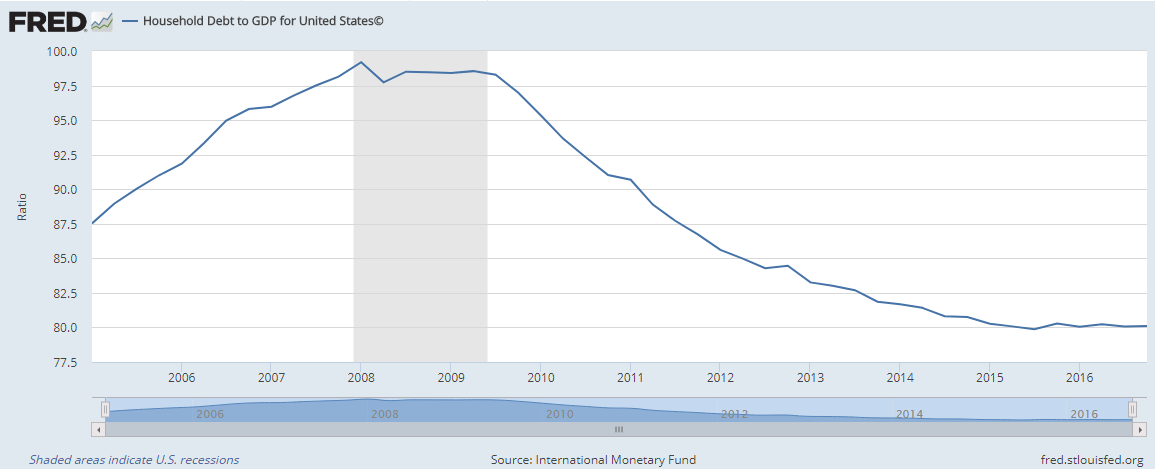

Government and corporate business debt/GDP increasing sharply since beginning of economic recovery, while consumer debt holding stable after years of deleveraging

After the dramatic run-up in consumer debt, which drove the last economic recovery, consumers seem increasingly content to just keep pace with nominal economic growth in terms of debt accumulation, after half a decade of deleveraging.

Source: FRED

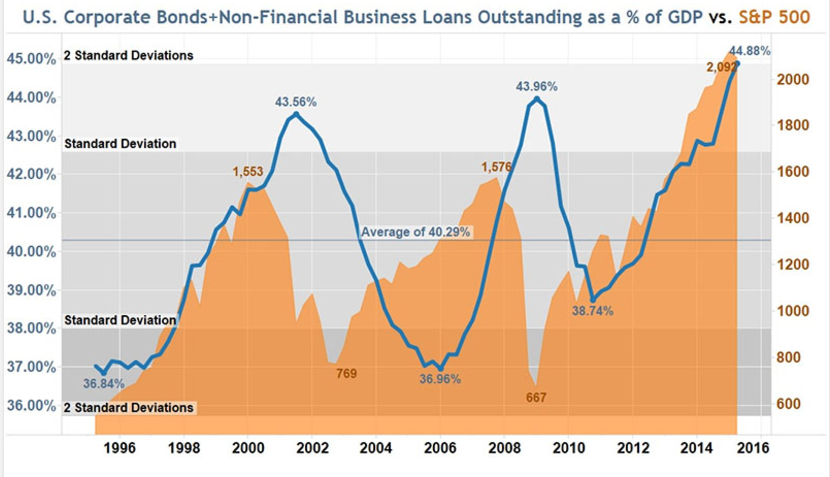

Corporate and business debt also entered a period of deleveraging during the last economic downturn, but it did not take long to get back to the business of feasting on the cheap money made available through central bank policies.

Source: National Inflation Association

Source: National Inflation Association

As we can see, between the end of 2010 and the beginning of 2016, the corporate and business debt level as a percentage of the size of the overall economy increased from 38.4% to 44.88%.

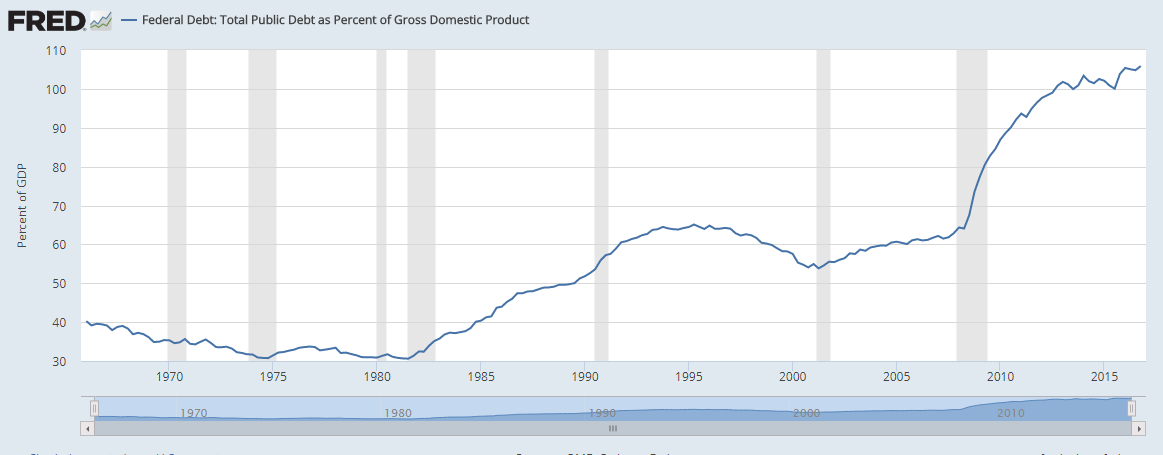

Government debt increased at a much faster pace when measured against the size of the economy. It went from 64% of GDP at the beginning of 2008 to over 105% currently.

Source: FRED

Source: FRED

Looking at these separate debt/GDP numbers together and by sector, there are a number of conclusions that we can draw. The first and obvious is the fact that since the beginning of the last economic crisis, total debt/GDP is still on a growing path. The significant decline in consumer debt between 2008 and 2015 helped temper that growth, but that trend has now come to an end. At best, we can expect consumer debt/GDP to remain steady. Government and business debt are both increasing at a significant rate in proportion of the size of the economy, meaning that in the absence of interest rates somehow continuing to decline from current levels, interest on debt as a percentage of GDP is also most likely on a rising trend, given that we can no longer expect relief from declining interest rates.

If we look at the individual components of debt, we can also notice the fact that most of the decline in debt/GDP came from the debt category which generally carries a higher interest rate, namely consumer debt, while the main increase came within the category which can borrow at a lower interest rate. This trend has been one of the contributing factors which drove the interest/GDP burden in the economy down in past years. In effect, government spending has become a more effective way of stimulating the economy, because it carries a lower interest rate. Therefore, it expands the economy's total debt-carrying capacity. With interest rates not going significantly lower from current levels anytime soon, shifting debt to lower interest rate categories may be the only sustainable way forward. By sustainable, I of course mean that it is sustainable in the short to medium term. I don't think this can be sustained in the longer term, because eventually the US government, as well as other governments around the world will find it very hard to sustain their debt servicing obligations. Whether they will cut back on spending in order to pay for increasing debt servicing costs, or eventually resort to massive money printing, which can come with its own problems, including perhaps the first ever global hyper-inflation crisis, something will eventually have to give.

The global picture

One of the factors that allowed for a sustained, (even if weak) global economic recovery in the aftermath of the 2008 financial crisis was the shifting of debt accumulation to the developing world, with China in particular shouldering a very significant portion of it. It has just been reported recently that China's total debt surpassed 300% of GDP in the first quarter of 2017. It is thought that its total debt has quadrupled since 2007, far outpacing its increasingly sub-average economic growth when compared with its growth trajectory before the global crisis. A number of other developing countries have also seen quite a bit of debt accumulation, at a higher rate of growth compared with economic expansion rates.

Total global debt now stands at $217 trillion, which is 327% of global GDP. We should keep in mind that the world borrows at an average interest rate that is considerably higher than America's economy can secure on average. It's impossible to tell just how significant the interest burden is on this debt, but for the sake of mental visualization, if we assume a conservative 5% average, it is about $11 trillion per year. The reason why I say that it is a conservative estimate is because governments, consumers, and businesses pay a significantly higher interest on debt in the developing world. India's 10-year government notes yield is about 6.5% at the moment, while Brazil pays 10.5%. We should keep in mind that consumer and other debts carry a much higher average interest burden. The world's entire GDP is about $76 trillion, meaning that global interest on debt is at least 14.5%. It should be worth noting that a lot of the debt is accumulating in countries with higher interest rates, while in places like Europe, deleveraging still continues, with private sector debt declining from $103.4 trillion, to $97.7 trillion. Keeping this in mind, the total global interest burden is likely to rise at a faster pace than the total debt/GDP ratio, because the global interest rate on each net dollar borrowed, or old debt being re-financed, is likely to be higher than the current global average.

The ultimate debt bubble

The last financial crisis was in large part due to a particular sector of the economy, within a number of individual countries becoming overly saturated with debt, beyond the ability of many to cope with it. The main sector where over-indebtedness led to crisis was the consumer sector, with some sovereign issues such as was the case with Greece and other countries in Europe being exposed as a secondary effect. All data points since the recovery started suggest that we are in another debt bubble.

It is a global one, and it involves debt becoming unsustainable at government, business, and consumer levels, across much of the world. The Western consumer is the exception to this trend, and it is in large part due to the fact that we are already carrying a heavy debt load, even after the deleveraging since 2008. But even in the Western world, the consumer deleveraging story is not absolute. For instance, in Canada new record highs are being recorded pretty much every quarter when measuring household debt as a percentage of disposable income. That ratio is now at 167%, and there is no sign that there will be a trend reverse happening anytime soon.

Not to mention that Canada's new Liberal government abandoned the old goal of balanced budgets and is now running significant deficits instead.

Given the widespread aspect of this debt bubble, it is likely that the US and the global economy will prove to have significant stamina in continuing forward with this trend for a prolonged period, due to the fact that the debt accumulation is spread out, instead of concentrated to one sector, as was the case with the previous bubble. The previous bubble burst much faster, because it was concentrated disproportionally in the consumer sector of the economy, which also happens to have a lower threshold in terms of carrying capacity, compared with governments which have various tools at their disposal, including a central bank. Because debt accumulation is more widespread within the economy, it is less likely to become an immediate issue within any particular sector of the economy.

No one can possibly predict the timing of it, because there are just so many factors involved, but eventually, this trend will lead to a severe global financial crisis. And, when it does, the broad aspect of it will make it unlikely that we will be able to achieve a recovery as easily as we did the last time around, because pretty much every major sector of the global economy will be affected and will engage in a similar deleveraging trend to what we have been seeing from the US consumers in the last few years. Problem is that when everyone is forced into debt deleveraging, the deleveraging itself tends to become impossible, because it becomes a game of endlessly catching up to a constantly shrinking economy, and it may take a very long time to actually catch up. In this regard, the lesson of Greece's deleveraging experience, which led to endless rounds of austerity, due to its effect of inducing economic shrinkage, without having the desired effect of reducing the debt/GDP ratio.

While the perception that at some point, we can just hunker down and start paying down the mountains of debt we are accumulating collectively in order to get out of this vicious cycle is still relatively prominent among the general public, the reality is that a broad-based effort to deleverage throughout the local and global economy can only result in years or decades of seemingly endless misery, with any debt reduction being matched or perhaps even surpassed by economic contraction, leading to loss of resources such as income and taxes, leading to a need to cut spending even more, causing more economic contraction. While the next global economic slowdown may still be some years away, perhaps, whenever it will arrive, it is very likely that it will be the beginning of this painful process.

0 comments:

Publicar un comentario