As lives get longer, financial models will have to change

,

IN 1965 ANDRÉ-FRANÇOIS RAFFRAY, a 47-year-old lawyer in southern France, made the deal of a lifetime. Charmed by an apartment in Arles, he persuaded the widow living there that if he paid her 2,500 francs (then about $500) a month until she died, she would leave it to him in her will. Since she was already 90, it seemed like a safe bet. Thirty years later Mr Raffray was dead and the widow, Jeanne Louise Calment, was still going strong. When she eventually passed away at 122, having become the world’s oldest person, the Raffray family had paid her more than twice the value of the house.

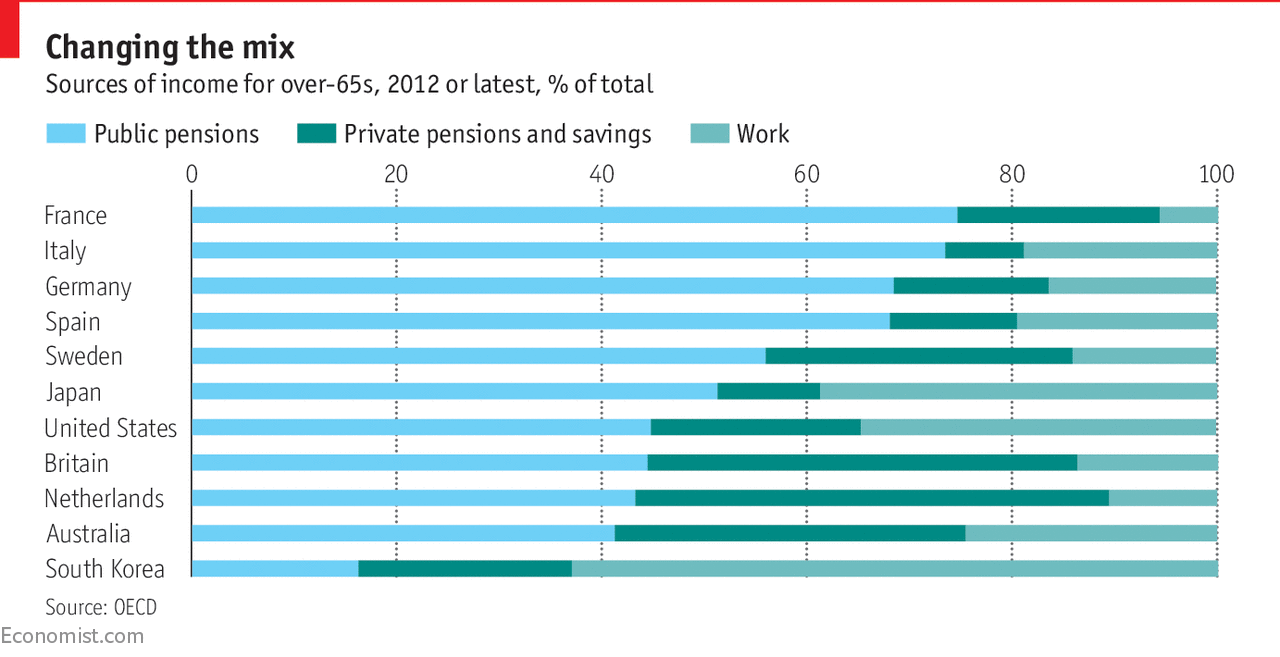

Underestimating how long someone will live can be costly, as overgenerous governments and indebted private pension schemes have been discovering. They are struggling to meet promises made in easier times. Public pensions are still the main source of income for the over-65s across the OECD, but there are big differences between countries (see chart). In both America and Britain public provision replaces around 40% of previous earnings, but in some European countries it can be 80% or more. Where it makes up a big share of total pension income, as in Italy, Portugal and Greece, a shrinking workforce will increasingly struggle to finance a bulging group of pensioners. . Private pension schemes, which supplement state provision, have been shifting from defined-benefit plans, where workers are promised a fixed amount of income in retirement, to defined-contribution plans, where workers themselves take on the risk. Such schemes are good for employers but tricky for individuals, who become personally responsible for ensuring they do not outlive their savings.

The new stage of life now emerging between work and old age adds a further complication. To accommodate these changes, the financial industry needs an overhaul.

First, it has to update the rigid three-stage life-cycle model on which most of its products are based. Second, it needs to resolve two opposite but equally troubling problems: undersaving during working life and oversaving during retirement. The first puts pressure on public provision, the second leads to underconsumption as cash is left under the mattress. Third, a more creative approach is needed to the range of assets that pensioners can draw on, including their homes, which have so far played little part in provision for old age.

“In a multi-stage life, the idea of hitting a cliff-edge retirement at 65 and then living off an annuity is outdated,” says Alistair Byrne, from State Street Global Advisors, a money manager.

His clients, many of whom intend to work past normal retirement age, are asking for more flexibility to get at their savings at a younger age. They also want a secure income for the last phase of life. “It’s not at all obvious that the traditional pension industry, which still sees life as a three-stage event, will survive this transition,” says Andrew Scott of the London Business School.

Nothing in the kitty

Many people simply do not save enough. Roughly 40% of Americans approach retirement with no savings at all in widely used retirement accounts such as IRAs or 401(k)s. In Britain 20% of women and 12% of men between 55 and 65 have no retirement savings, according to Aegon.

Yet with the demise of defined-benefit schemes, the increase in the retirement age and the steady rise in life expectancy, most of today’s workers will need to save more than their parents did. Some of them do not earn enough to put money aside, but for many the problem is in the mind: they consistently underestimate how long they will live and overestimate how long their money will last. As more people become self-employed, getting them to save for their old age becomes ever more important.

One solution is to allow retirement funds to be used more flexibly, which may encourage people to save more. But nudges are unlikely to be enough. “People need a push,” says Myungki Cho, from Samsung Life’s Retirement Research Centre in Seoul. Some countries, such as Denmark and the Netherlands, provide such a push by making enrolment in pension schemes more or less mandatory.

Short of that, auto-enrolment, recently introduced in Britain, and auto-escalation (increasing contributions over time) can also make a difference.

At the same time many pensioners spend less than they can afford, which creates its own problems. Ronald Lee and Andrew Mason have found that in most rich countries the elderly are net savers. Since they cannot be sure how long they will live and what their state of health will be, and have no way of predicting inflation, interest rates and markets, some caution is clearly in order. But Chip Castille, from BlackRock, an asset manager, thinks oversaving is often unintentional. “It would be an extraordinary coincidence if you saved exactly enough for retirement,” he says.

This gets to the heart of why some economists are pessimistic about greying societies. In a phase when older people should be spending freely, many are accumulating wealth, says David Sinclair, of the ILC UK. He thinks the greater pension freedoms granted in Britain in 2015 are more likely to lead to frugality rather than spending sprees.

Such “accidental” oversaving will increase in a world of defined-contribution plans, predicts Tony Webb, an economist at the New School, in New York City. Given a choice, people will assemble their own kitties rather than buy annuities that provide an agreed lifetime income in exchange for a lump sum. If they die young, the money will be a windfall for their heirs. Similarly, since money locked up in homes is difficult to get at during the owner’s lifetime, much of this too will be passed on, Mr Webb adds. Raising inheritance-tax rates could make a difference, but better insurance is equally important. This dormant wealth, which is often neither invested nor spent, is stopping many of the younger old from realising their full economic potential. “Often people just need the confidence that we’ve run the numbers and that they really can afford to make that donation to a charity, or spend a little more on themselves,” says Kai Stinchcombe, from True Link, a financial-advice firm for pensioners.

Advertisement:Replay Ad

Advertisement

3

Take care

Depending on where people live, how much they earn and whether they have family willing to care for them, one of the greatest financial risks of ageing can be end-of-life care expenditure. A 50-year-old American has a better-than-even chance of ending up in a nursing home, estimate Michael Hurd and colleagues from RAND, a research organisation in America. In Britain an official review in 2011 of long-term care reckoned that a quarter of older people in Britain needed very little care towards the end of life but 10% faced care costs in excess of £100,000.

Most countries will need to find a mix of public and private provision to pay for long-term care costs.

A well-functioning insurance market should be an important part of this, but care insurance has mostly failed to take off. American providers who piled in too enthusiastically in the 1990s got burnt when customers needed more care than expected, and are still haunted by the experience. Low rates of return on bonds have not helped.

Every country has its own peculiarities, but four common factors help explain the market failures.

First, the future of public care is uncertain. Second, despite or because of this, many people think they do not need insurance because the state or their family will look after them. Third, the market is subject to “adverse selection”—the likelihood that insurance will appeal only to those most at risk of needing care. And fourth, care costs are unpredictable and could spin out of control in the future. As a result, insurers either avoid the care market altogether, or charge exorbitant premiums and add lots of restrictions.

As with any big risk, pools need to be large to make protection products work. The easiest way to achieve this is to make insurance compulsory, as in Germany. One alternative is auto-enrolment in a public-private scheme with an opt-out, a method with which Singapore is experimenting. At a minimum, some government intervention—such as providing a backstop for the most catastrophic risks—seems to be required for the market to establish itself. But perhaps the biggest problem is that government policies chop and change far too often.

Insurers could help, not least by offering more hybrid products such as life insurance with the option of an advance on the payout if customers need care, or annuities that pay a lower-than-usual income but convert to a higher-than-usual rate if pre-agreed care levels become necessary. And there is a need for clearer guarantees against unexpected premium hikes. Most importantly, though, insurers will need to persuade people to enroll long before they are likely to require any care.

By far the most common reason for someone needing long-term care is that they are suffering from Alzheimer’s or some other form of dementia. Globally around 47m people have dementia.

Without a medical breakthrough this number could grow to 132m by 2050, according to the World Alzheimer’s Report. One study found that people suffering from dementia accounted for four-fifths of all those in care homes worldwide.

In the absence of other options, for many people the ultimate insurance is their home, though few homeowners see it that way. In the rich world much of the wealth of lower and middle-income households is tucked away in bricks and mortar. With house prices soaring in many countries, releasing some of this equity could greatly benefit asset-rich but cash-poor pensioners, as well as the wider economy.

The most obvious tool for this is a reverse mortgage, which lets homeowners exchange some of their home’s equity for a lump sum or a stream of income in retirement. But it is not widely used. In America fewer than 49,000 reverse mortgages were sold last year, most of them provided by only about ten banks. Mis-selling scandals in the early days now seem to have been resolved, says Jamie Hopkins, of the American College of Financial Services, but people find such mortgages scary and worry that they might lose their home. Because of the lack of competition, the products also remain expensive. Mainstream financiers could help expand the market.

In the meantime, entrepreneurial empty-nesters have found another way to sweat their assets: Airbnb.

The over-60s are the fastest-growing group of hosts on the home-sharing site and receive the highest ratings. Almost half of older hosts in Europe say the additional income helps them stay in their home.

The longer that people live, the more varied their life cycle will become. Workers will take breaks to look after children or go back to school; pensioners will take up a new job or start a business.

Financial providers need to recognise these changing needs and cater for them. That includes helping to fund technology that could vastly improve the final stage of life.

0 comments:

Publicar un comentario