Ageing populations could be a boon rather than a curse. But for that to happen, a lot needs to change first, argues Sacha Nauta

.

“NO AGE JOKES tonight, all right?” quipped Sir Mick Jagger, the 73-year-old front man of the Rolling Stones (pictured), as he welcomed the crowds to Desert Trip Music Festival in California last October. The performers’ average age was just one year below Sir Mick’s, justifying his description of the event as “the Palm Springs Retirement Home for British Musicians”. But these days mature rock musicians sell: the festival raked in an estimated $160m.

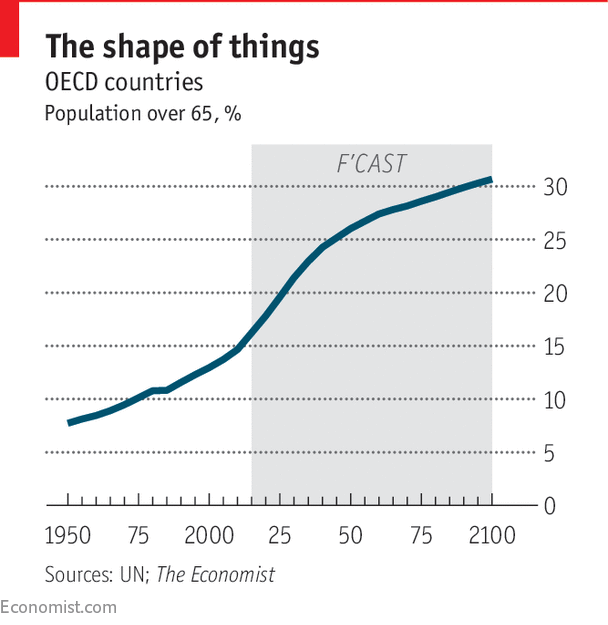

There are many more 70-somethings than there used to be, though most of them are less of a draw than the Stones. In America today a 70-year-old man has a 2% chance of dying within a year; in 1940 this milestone was passed at 56. In 1950 just 5% of the world’s population was over 65; in 2015 the share was 8%, and by 2050 it is expected to rise to 16%. Rich countries, on which this report is focused, are greying more than the developing world (except for China, which is already well on the way to getting old); the share of over-65s in the OECD is set to increase from 16% in 2015 to 25% by 2050. This has knock-on effects in older age groups too. Britain, which had just 24 centenarians in 1917, now has nearly 15,000.

Globally, a combination of falling birth rates and increasing lifespans will increase the “old-age dependency ratio” (the ratio of people aged 65 or over to those aged 15-64) from 13% in 2015 to 38% by the end of the century. To listen to the doomsayers, this could lead not just to labour shortages but to economic stagnation, asset-market meltdowns, huge fiscal strains and a dearth of innovation. Spending on pensions and health care, which already makes up over 16% of GDP in the rich world, will rise to 25% by the end of this century if nothing is done, predicts the IMF.

Much of the early increases in life expectancy were due not to people living longer but to lower death rates among infants and children, thanks to improvements in basic hygiene and public health. From the start of the 20th century survival rates in old age started to improve markedly, particularly in the rich world, a trend that continues today. More recently, life spans—the estimated upper limits of average life expectancy—have also been increasing. Until the 1960s they seemed fixed at 89, but since then they have risen by eight years, thanks in part to medical advances such as organ replacements and regenerative medicine. The UN estimates that between 2010 and 2050 the number of over-85s globally will grow twice as much as that of the over-65s, and 16 times as much as that of everyone else.

Warnings about a “silver time bomb” or “grey tsunami” have been sounding for the past couple of decades, and have often been couched in terms of impending financial disaster and intergenerational warfare. Barring a rise in productivity on a wholly unlikely scale, it is economically unsustainable to pay out generous pensions for 30 years or more to people who may have been contributing to such schemes only for a similar amount of time. But this special report will argue that the longer, healthier lives that people in the rich world now enjoy (and which in the medium term are in prospect in the developing world as well) can be a boon, not just for the individuals concerned but for the economies and societies they are part of. The key to unlocking this longevity dividend is to turn the over-65s into more active economic participants.

This starts with acknowledging that many of those older people today are not in fact “old” in the sense of being worn out, sick and inactive. Today’s 65-year-olds are in much better shape than their grandparents were at the same age. In most EU countries healthy life expectancy from age 50 is growing faster than life expectancy itself, suggesting that the period of diminished vigour and ill health towards the end of life is being compressed (though not all academics agree). Yet in most countries the age at which people retire has barely shifted over the past century. When Otto von Bismarck brought in the first formal pensions in the 1880s, payable from age 70 (later reduced to 65), life expectancy in Prussia was 45. Today in the rich world 90% of the population live to celebrate their 65th birthday, mostly in good health, yet that date is still seen as the starting point of old age.

This year the peak cohort of American baby-boomers turns 60. As they approach retirement in unprecedented numbers, small tweaks to retirement ages and pensions will no longer be enough. This special report will argue that a radically different approach to ageing and life after 65 is needed.

The problems already in evidence today, and the greater ones feared for tomorrow, largely arise from the failure of institutions and markets to keep up with longer and more productive lives. Inflexible labour markets and social-support systems all assume a sudden cliff-edge at 60 or 65. Yet in the rich world at least, a new stage of life is emerging, between the end of the conventional working age and the onset of old age as it used to be understood.

Advertisement: Replay Ad

Advertisement

3

Those new “young old” are in relatively good health, often still work, have money they spend on non-age-specific things, and will run a mile if you mention “silver”. They want financial security but are after something more flexible than the traditional retirement products on offer. They will remain productive for longer, not just because they need to but because they want to and because they can. They can add great economic value, both as workers and as consumers. But the old idea of a three-stage life cycle—education, work, retirement—is so deeply ingrained that employers shun this group and business and the financial industry underserve it.

What’s in a name?

History shows that identifying a new life stage can bring about deep institutional change. A new focus on childhood in the 19th century paved the way for child-protection laws, mandatory schooling and a host of new businesses, from toymaking to children’s books. And when teenagers were first singled out as a group in America in the 1940s, they turned out to be a great source of revenue, thanks to their willingness to work part-time and spend their income freely on new goods and services. Such life stages are social constructs, but they have real consequences.

This report will argue that making longer lives financially more viable, as well as productive and enjoyable, requires a fundamental rethink of life trajectories and a new look at the assumptions around ageing. Longevity is now widespread and needs to be planned for. The pessimism about ageing populations is based on the idea that the moment people turn 65, they move from being net contributors to the economy to net recipients of benefits. But if many more of them remain economically active, the process will become much more gradual and nuanced. And the market that serves these consumers will expand if businesses make a better job of meeting their needs.

The most important way of making retirement financially sustainable will be to postpone it by working longer, often part-time. But much can be gained, too, by improving retirement products. The financial industry needs to update the life-cycle model on which most of its products and advice are based. Longer lives require not just larger pots of money but more flexibility in the way they can be used.

As defined-benefit pension schemes become a thing of the past, people need to be encouraged to set aside enough money for their retirement, for example through auto-enrolment schemes. It would also help if some of the better-off pensioners spent more and saved less. They would be more likely to do that if the insurance industry were to improve its offerings to protect older people against some of the main risks, such as getting dementia or living to 120. Many people’s biggest asset, their home, could also play a larger part in funding longer lives.

And for the oldest group, increasingly there will be clever technology to help them make the most of the final stage of their lives, enabling them to age at home and retain as much autonomy as possible. Perhaps surprisingly, products and services developed mainly for the young, such as smartphones, social media, connected homes and autonomous cars, could also be of great benefit to the older old.

But the report will start with the most obvious thing that needs to change for the younger old: the workplace. Again, there are parallels with young people. Working in the gig economy, as so many of them do, may actually be a better fit for those heading for retirement.

0 comments:

Publicar un comentario