The splashing of taxpayers’ money is not pretty, but it is pragmatic

.

BANKS sicken slowly but die fast. For years Banca Popolare di Vicenza and Veneto Banca, in the prosperous Veneto, in north-east Italy, had been plagued by mismanagement. Even criminal investigations are under way. For months the Italian government had been wrangling with European authorities over the terms of a bail-out. For weeks it had seemed improbable that private investors would put in money alongside the state, as the European Commission insisted.

On June 23rd the European Central Bank (ECB) declared that the banks were “failing or likely to fail”. Two days later, after a frantic weekend, the Italian government pronounced them dead: their good assets were sold to Intesa Sanpaolo, Italy’s second-biggest lender, for a token €1 ($1.14), and their dud ones put into a “bad bank”. The operation may cost Italian taxpayers €17bn. This is the second call on Italy’s public purse this month. On June 1st the commission approved, in principle, the rescue of long-troubled Monte dei Paschi di Siena, the fourth-biggest bank, which is expected to cost the state €6.6bn.

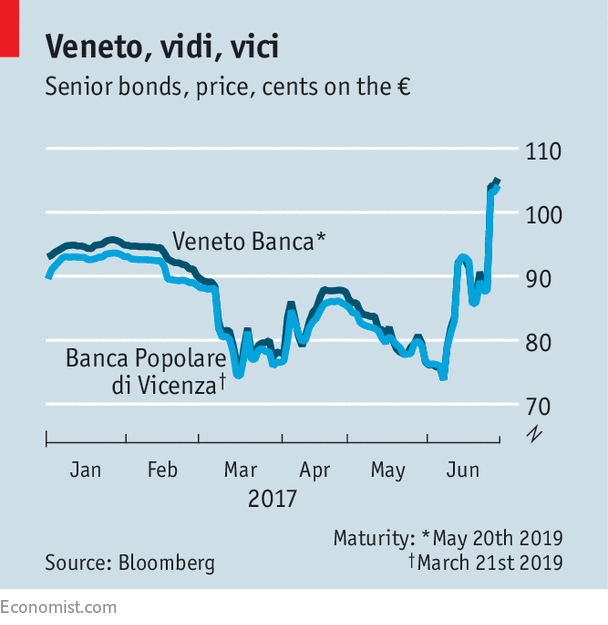

The Veneto banks’ clients breathed a sigh of relief when branches opened on June 26th. So did the stockmarket: bank shares rose. So did holders of the lenders’ senior bonds, which will be taken on by Intesa. In early June they had traded at below 74 cents on the euro. They jumped to above par (see chart). Yet the bail-out has sown confusion—and consternation—about the euro zone’s new, and scarcely tested, system of treating failing banks. After the ECB’s declaration, responsibility passed to the Single Resolution Board (SRB), a separate agency set up by the commission.

Only one other such case has reached the SRB. On June 6th the ECB deemed Banco Popular, Spain’s sixth-biggest bank, to be in its death throes. The SRB put Popular into “resolution”—the European procedure for winding up banks—and overnight it was sold to Santander, Spain’s biggest lender, also for €1. Under rules that came into force in January 2016, equity, bonds (both senior and junior) and deposits over €100,000 must take losses, to the value of 8% of total liabilities, before public money is injected into a bank. Shareholders and junior bondholders were wiped out, but senior creditors were spared. Taxpayers did not pay a cent; Santander will raise €7bn in equity.

The SRB dealt with the Italian pair differently. It judged that it was “not warranted in the public interest” to put them into resolution. Their demise would not have a “significant adverse impact on financial stability”, because of their limited interconnections with other banks. (At the end of 2016 they were Italy’s 10th- and 11th-biggest by assets.) The SRB instead decided that they should be dealt with under Italian insolvency law. Shareholders and holders of junior debt will suffer losses, though retail investors, who own €200m in junior bonds, will be compensated for “mis-selling”; Italian banks routinely sold such bonds to retail customers.

Senior creditors were untouched.

Advertisement: Replay Ad

Advertisement

3

Although the board saw no risk to stability, the government perceived a danger to the Veneto’s economy. Intesa will be paid €3.5bn to offset the effect of the extra assets on its capital ratios. It will also get €1.3bn to cover integration costs, including the closure of around 600 branches. Its market share in the region will rise to 30%. Mediobanca, an investment bank, estimates the acquisitions will yield profits of €250m by 2020. The government is also putting up €12bn in guarantees against potential losses, although it expects to spend only a small fraction of that; and some of the banks’ senior debt was state-guaranteed, so it may have saved money there.

The commission’s competition arm approved the aid.

Using national insolvency will also suit Italy’s banks as a whole. Resolution would have cost them €12.5bn under the country’s deposit-guarantee scheme, putting an unwelcome dent in their capital ratios. The deal also frees money in Atlante, a fund backed by Italian financial institutions, which had been earmarked for buying the Veneto banks’ bad loans. It may now be spent on Monte dei Paschi’s.

Critics—most vocally, some German MEPs—lament the splurge of public money: Europe’s new rules, after all, are supposed to discourage that. They argue that the bail-out has put paid to Europe’s proposed “banking union”, in which one set of rules should apply to all. That is overblown, says Nicolas Véron of Bruegel, a Brussels think-tank, and the Peterson Institute for International Economics in Washington, DC. Banking union is incomplete: this episode serves as a reminder. “The single resolution mechanism is not really single as long as you have different insolvency regimes for banks,” says Mr Véron.

Moreover, given the wretched state of the Veneto banks, their acquirer could demand a dowry; Santander was willing to raise money to absorb an essentially sound Popular. Arguably, Italy should have sorted out its mess sooner, before Europe’s stricter bail-out rules came into force; but it has spent a pittance compared with what other countries shelled out after the financial crisis.

Italy’s pile of non-performing loans is at last shrinking. But worries linger—notably about Carige, a Genoese bank. While the economy continues to crawl, many lenders will struggle for profit.

Although consolidation is taking place, Italy’s bank branches still outnumber its pizzerias; despite recent reform, recovery of bad debts is still slow. Bail-outs are forgivable—if they mean a fresh start.

Time for Italy, if it can, to prove the doubters wrong.

0 comments:

Publicar un comentario