Buttonwood

Markets worry about central Banks

Will there be a sudden tightening in policy?

Since 2009 central banks have been incredibly supportive of the financial markets—keeping short-term interest rates at historic lows and buying trillions of dollars worth of bonds. But in recent weeks, several of them have been hinting at reducing their largesse.

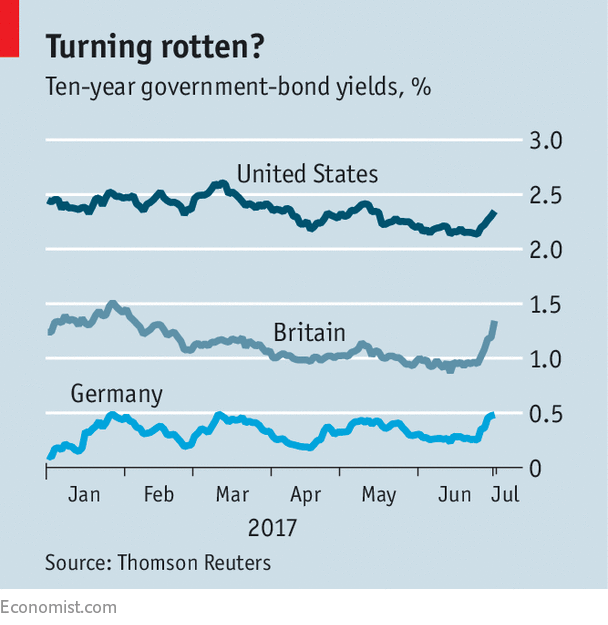

But the biggest shock to markets came on June 27th, when Mario Draghi, the head of the European Central Bank, remarked that “deflationary forces have been replaced by reflationary ones.” The result was a sudden rise in bond yields (see chart). “Super Mario” carries great weight with investors; he was widely credited with halting the euro crisis back in 2012 with his vow to do whatever it took to save the single currency.

The ECB tried to calm investor nerves in the aftermath of the statement. Mansoor Mohi-uddin, a strategist at Royal Bank of Scotland, thinks the markets overreacted to Mr Draghi’s words. The ECB is not about to stop its stimulus. He thinks that, in September, the bank will merely indicate that it will be reducing its monthly rate of purchases from €60bn ($68bn) to €40bn at the start of 2018. Mr Draghi is just preparing the ground.

There was some speculation that central banks had deliberately co-ordinated their comments. But the simpler explanation is that they were reacting to similar factors. First, global growth seems have picked up in the second half of 2016, allowing banks to withdraw some stimulus. Second, Fed tightening gives other central banks cover; any bank tightening on its own would probably see its currency strengthen strongly, risking overkill.

There are also signs that the global recovery may not be that robust. Commodity prices, an indicator of global demand, have fallen since the start of the year. China’s economy is showing signs of a loss of momentum, according to Capital Economics, a consultancy. David Owen of Jefferies, an investment bank, says that global trade and industrial production are both growing at an annualised rate of less than 2%, based on the past three months. “This is not consistent with a strong recovery in investment,” he adds.

Central banks will have to tread very carefully. Global debt is higher as a proportion of GDP than it was before the financial crisis started in 2007. Ultra-low interest rates have made borrowing sustainable but have also encouraged companies and consumers to take on more debt. The annual report of the Bank for International Settlements, released on June 25th, warned of elevated credit risks in a number of emerging economies and smaller developed economies. “Financial-cycle downturns could weaken demand and growth, not least by dampening consumption and investment,” the report said. The BIS also worries that a return of trade protectionism could sap the global economy’s strength.

It is a lot easier to begin monetary stimulus than to end it. More than a quarter of a century has passed since the Japanese bubble burst in 1990, and the Bank of Japan is still pumping money into the economy and trying to keep ten-year bond yields close to zero. By the end of the novel, Elinor (sense) and Marianne (sensibility) find contentment with a vicar and a retired colonel respectively. Unlike Austen, central banks cannot always arrange a happy ending.

0 comments:

Publicar un comentario