It's 1999 All Over Again

by: William Koldus, CFA, CAIA

- The U.S. equity market resembles the late 1990s.

- Growth has been prized over value since 2007.

- Value investments are set to outperform over a multi-year period.

- Growth has been prized over value since 2007.

- Value investments are set to outperform over a multi-year period.

"A 60:40 allocation to passive long-only equities and bonds has been a great proposition for the last 35 years ... We are profoundly worried that this could be a risky allocation over the next 10." - Sanford C. Bernstein & Company Analysts (January 2017)

“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.” - Sir John Templeton

"Life and investing are long ballgames.” - Julian Robertson

(Source: Author’s Photo, Vintage 1999 Hat)

Introduction

Time, which is our most valuable resource, has been flying by.

In August, I will turn 40, and I have been actively investing/speculating from the time I was 13, when I took my savings from a paper route that I had accumulated since I was 9, and put them into the stock market, with the help of my now deceased father.

Since 1990, there have been many cycles in the stock, bond, and commodity markets, yet as I firmly approach the hallowed threshold of middle age, with children that are approaching the age I was when I started investing, there is an eerie resemblance to the late 1990s.

Specifically, there is a dichotomy between growth and value that I never thought I would see again.

In summary, growth stocks have been prized for the past ten years, ironically ever since the 2007-2009 bear market, and today, they are at a historically overvalued level versus their value counterparts.

Thesis

Value stocks are relatively cheap versus growth stocks in a historically frothy market.

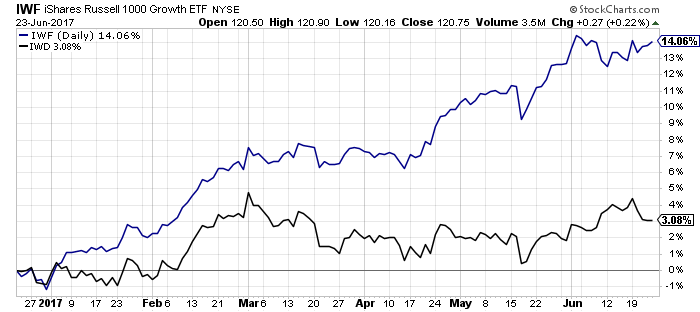

Growth Stocks Leading Value Stocks in 2017 and Since 2007

After a brief resurgence in 2016, value stocks have once again been lapped by their growth counterparts.

The iShares Russell 1000 Growth ETF (IWF) is up 14.1% in 2017, while the iShares Russell 1000 Value ETF (IWD) is up 3.1% year to date.

(Source: William Travis Koldus, StockCharts.com)

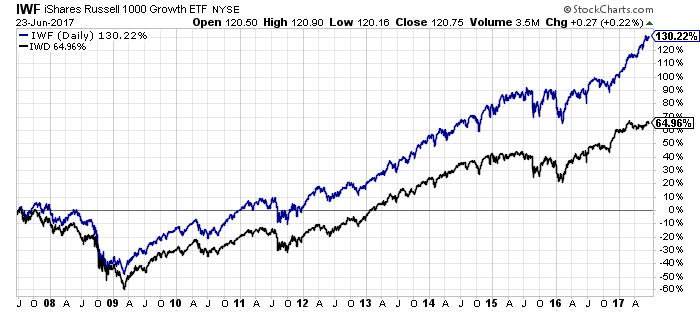

Over the past decade, the out-performance of growth versus value is even more delineated in the large-cap arena, with the iShares Russell 1000 Growth ETF posting a 130.2% return, while the iShares Russell 1000 Value ETF has only returned 65.0%.

(Source: WTK, StockCharts.com)

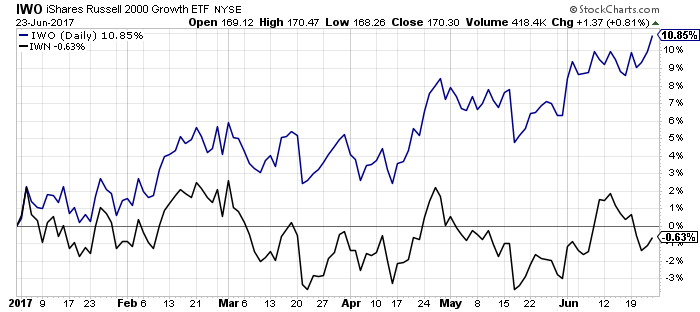

In the smaller capitalization stocks, the story is the same, as the iShares Russell 2000 Growth ETF (IWO) has outperformed the iShares Russell 2000 Value ETF (IWN), 10.9% to -0.6% in 2017.

(Source: WTK, StockCharts.com)

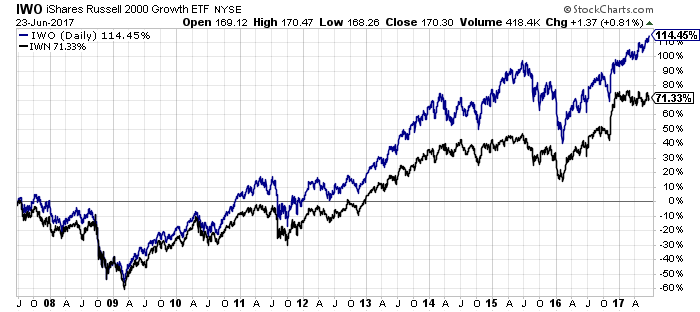

The story over the last decade is the same, as the iShares Russell 2000 Growth ETF has returned 114.5%, while the iShares Russell 2000 Value ETF has gained 71.3%.

(Source: WTK, StockCharts.com)

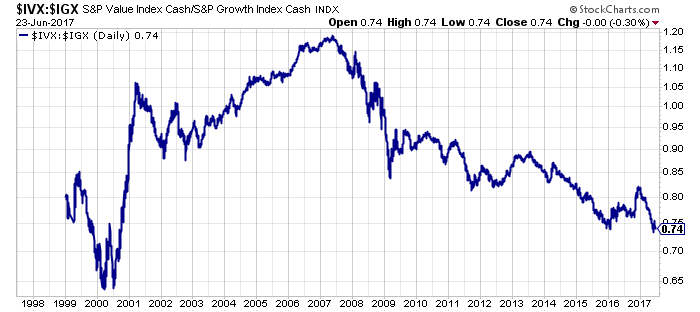

Growth stocks were the market darlings of the 1990s, and this pushed up their valuations, while value stocks were generally out-of-favor. Value stocks had their day in the sun from 2000-07, but since then, growth stocks have once again outperformed, in a world starved for growth as the chart below illustrates.

(Source: WTK, StockCharts.com)

The end result is that we are approaching the late 1990s relative valuation discount of value stocks versus their growth counterparts.

FAANG Stocks Lead

The S&P 500 Index, as measured by the SPDR S&P 500 ETF (SPY) has had a very strong year thus far, posting a gain of 9.8% with dividends included in this performance figure.

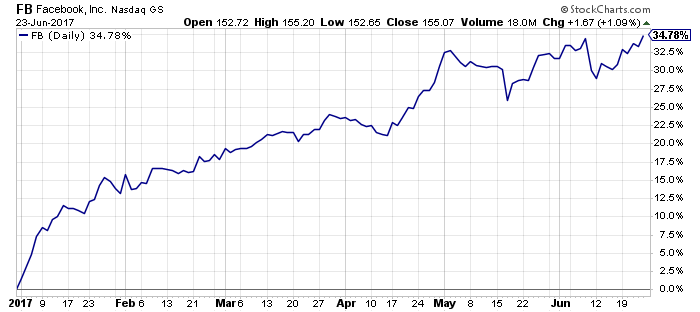

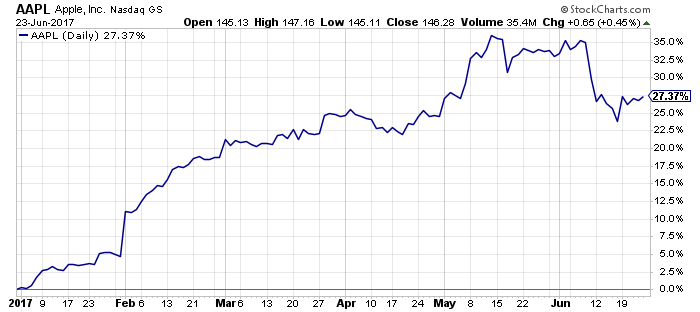

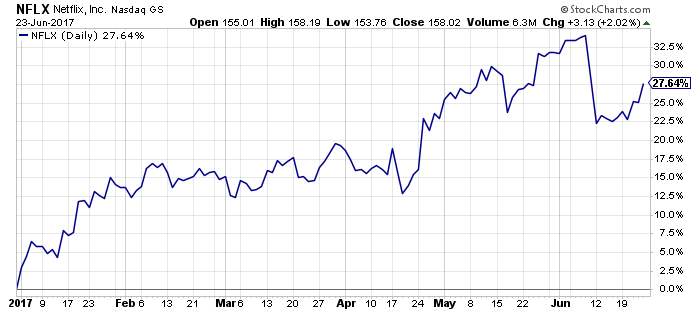

The largest capitalization growth stocks, however, have trounced this figure year-to-date.

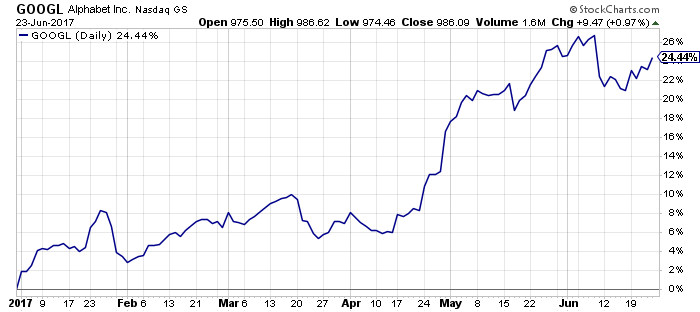

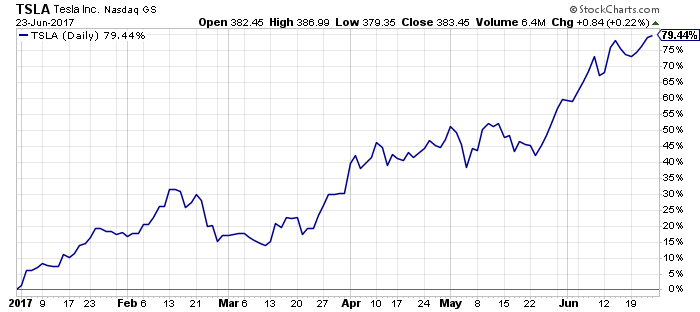

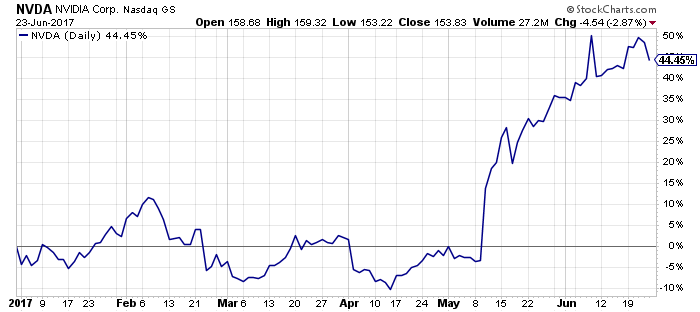

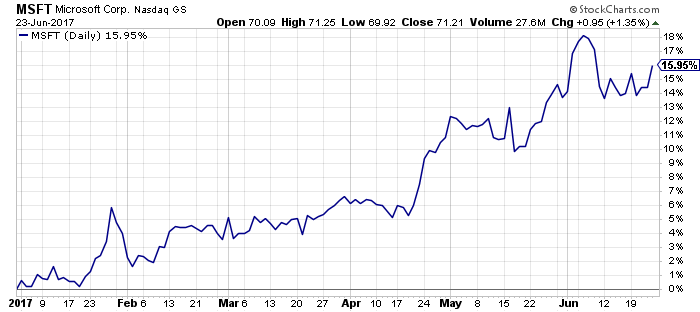

Facebook (FB) is up 34.8%, Apple (AAPL) is up 27.4%, Amazon (AMZN) is up 33.4%, Netflix (NFLX) is up 27.6%, Alphabet (GOOGL), (GOOG), is up 24.4%, Tesla (TSLA) is up 79.4%, NVIDIA (NVDA) is up 44.5%, and Microsoft (MSFT) is up 16.0% in 2017.

(Source: WTK, StockCharts.com)

Apple, Alphabet, Microsoft, Amazon, Johnson & Johnson (JNJ), Facebook, and Exxon Mobil (XOM), in the order they are listed, are the seven largest market capitalization companies in the S&P 500 Index as I pen this article.

With passive fund flows surging, the largest market capitalization companies are attracting a greater percentage of invested capital.

In 2016, according to Morningstar, passive strategies saw inflows of $428.7 billion, while active strategies saw outflows of $285.2 billion. This pattern of fund flows has accelerated in 2017, as fiduciary rules changes, and the outperformance of the largest equities alongside passive strategies, have combined to create an irresistible temptation for investors.

While active strategies still hold more overall assets than passive strategies, an increasing number of active strategies closely resemble index funds, so the amount of true actively managed money is very low historically, perhaps near an all-time low (in my opinion).

Building on this narrative, ETF fund flows, which are mostly allocated to passive strategies, are surging past $4 trillion in invested assets, and they are potentially on their way to $10 trillion.

Another Look at Growth Stocks Since 2007

We mentioned earlier that growth stocks have outperformed their value counterparts since 2007, and this can be seen in the following chart, which was shown in the first section that compared value and growth returns.

(Source: WTK, StockCharts.com)

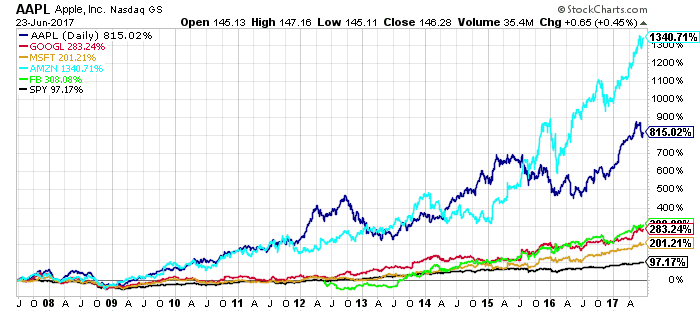

The outperformance by the largest five growth stocks over the past decade, specifically Apple, Alphabet, Microsoft, Amazon, and Facebook, which are also five of the six largest stocks in the S&P 500 Index (Facebook is neck-and-neck with JNJ), is staggering, as the following chart shows.

(Source: WTK, StockCharts.com)

Amazon shares lead the pack, with gains of 1341%, Apple shares have gained 815%, Facebook shares, in a more limited time frame due to their most recent IPO, have gained 308%, Alphabet shares have gained 283%, and Microsoft shares have gained 201%, all trouncing the gains of SPY, which has risen a still very strong 97% over the past ten years.

The Takeaway - a Circular Flow of Capital Creates Opportunities

As index and ETF strategies, which are often passive, gain prominence, more and more capital flows into the largest capitalization equities. Additionally, with a majority of individual and professional investors chasing performance, due to the strength and duration of the current bull market since March 2009, the concentration of capital into the best performing equities is further accelerated.

Does this sound like the late 1990s investing landscape?

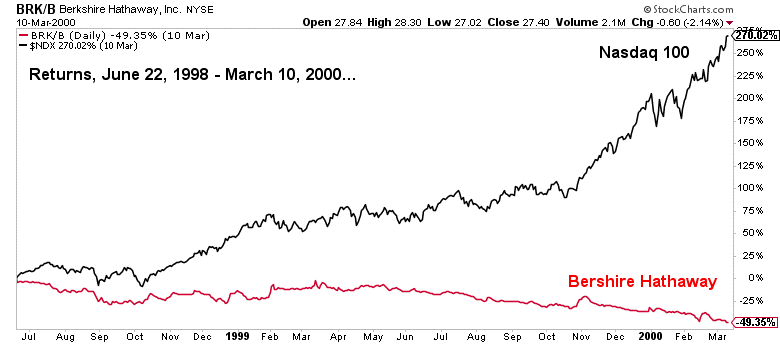

I will answer this for you, this is exactly what happened in the late 1990s, when legendary value investors like Warren Buffett of Berkshire Hathaway (BRK.B), (BRK.A), Julian Robertson, and Jeremy Grantham all materially trailed the performance of the broader market by a significant degree, and each of these acclaimed investors lost a significant number of clients and a significant number of client assets. Julian Robertson even famously closed his hedge fund.

In fact, at one point in March of 2000, Berkshire Hathaway was down roughly 50% while the NASDAQ 100 (QQQ) was up 270%.

(Source: WTK, StockCharts.com)

Building on the narrative above, due to the out-performance of the S&P 500 Index in 2017, and from 2009-2017, an increasing number of active managers have become "closet indexers," which essentially replicate the index assets while charging a higher fee.

This quote from a March 1st, 2011, article (think about how much more the situation has accelerated today), which was titled, "The Rise Of The Closet Indexers," highlights how fast active funds have re-purposed to mirror their benchmarks:

A couple of decades ago there were essentially no 'closet index' funds, says Martijn Cremers, a professor of finance at the Yale School of Management who worked with Petajisto on a previous study of this issue. But as index investing has become more popular, individual investors have become 'more benchmark aware,' he says.

'Your performance relative to the benchmark has become more salient.' As a result, investors are now quicker to bail out of funds if they fall short of their benchmark indexes, creating an incentive for managers to at least match their benchmarks -- and a disincentive to make big bets that could go wrong, Cremers says…

In summary, the end result of this circular flow of capital is that the amount of "true" actively managed money today, is much less than it has been historically. Simply put, there is real career risk in being an active manager, and being significantly different than indexes. And, when everyone is crowded in the same trades, in the same stocks, perhaps that is the time to be different?

To close, I know my answer to this open-ended question, and I will let readers follow the logic and their brains to get to their answer.

The investment landscape is changing, and if you are interested in joining a unique community of contrarian, value investors, and would like to see all of the historical trades and current positioning of the "Bet The Farm" and the "Best Ideas" Portfolios, please consider signing up for my premium research service, "The Contrarian." This service has been well reviewed by its members, and I believe we are once again at a unique inflection point in the financial markets, for the third time in the past two decades.

The wide dispersion of returns in 2017 has created a second chance opportunity, in my opinion, and I am discussing this potential opportunity at the upcoming DIY Investor Summit. If you are interested in hearing a portion of my thoughts alongside eight other respected market analysts, please explore the DIY Investor Summit.

0 comments:

Publicar un comentario