Is It Time To Buy Platinum?

by: Hebba Investments

- Platinum is the worst-performing precious metal in the complex and has been down four of the last five years.

- At current prices, mine production is unsustainable and as we approach platinum's cash costs of production, supply will inevitably decrease.

- Negativity based on its role in the auto industry is driving investor sentiment.

- Implementation of tougher emissions standards in China for diesel are scheduled to go into effect in January 2018, which will use more platinum.

- Speculative sentiment is the most bearish it has been since the CFTC has published records in 2006.

- At current prices, mine production is unsustainable and as we approach platinum's cash costs of production, supply will inevitably decrease.

- Negativity based on its role in the auto industry is driving investor sentiment.

- Implementation of tougher emissions standards in China for diesel are scheduled to go into effect in January 2018, which will use more platinum.

- Speculative sentiment is the most bearish it has been since the CFTC has published records in 2006.

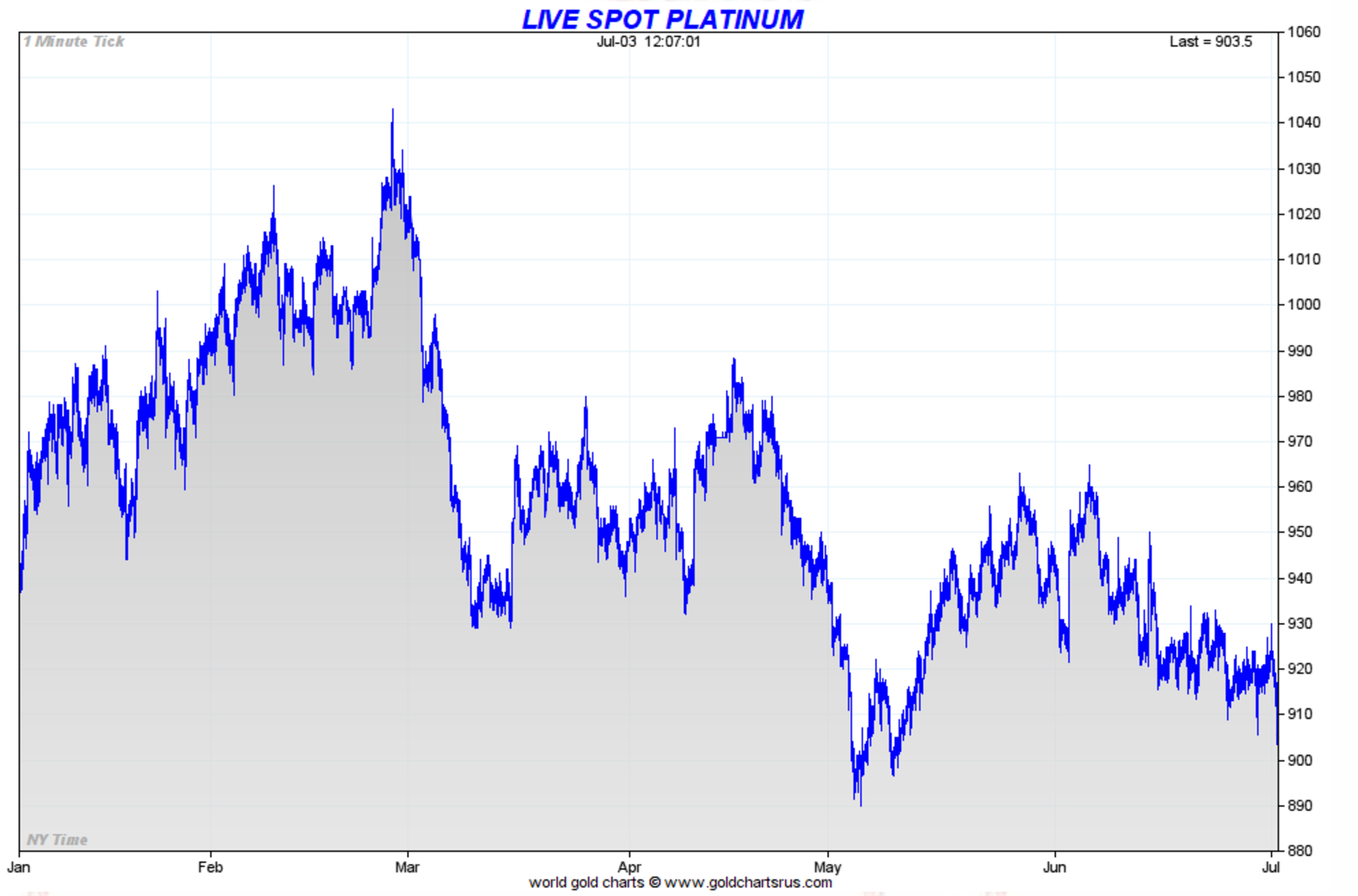

While we have put a heavy focus in covering gold and silver, the hammering that platinum has received has piqued our interest. We believe that in platinum investors might have the best opportunity of all precious metals. Of course, looking at the YTD chart of platinum doesn't inspire much confidence:

Source: GoldchartsRUs

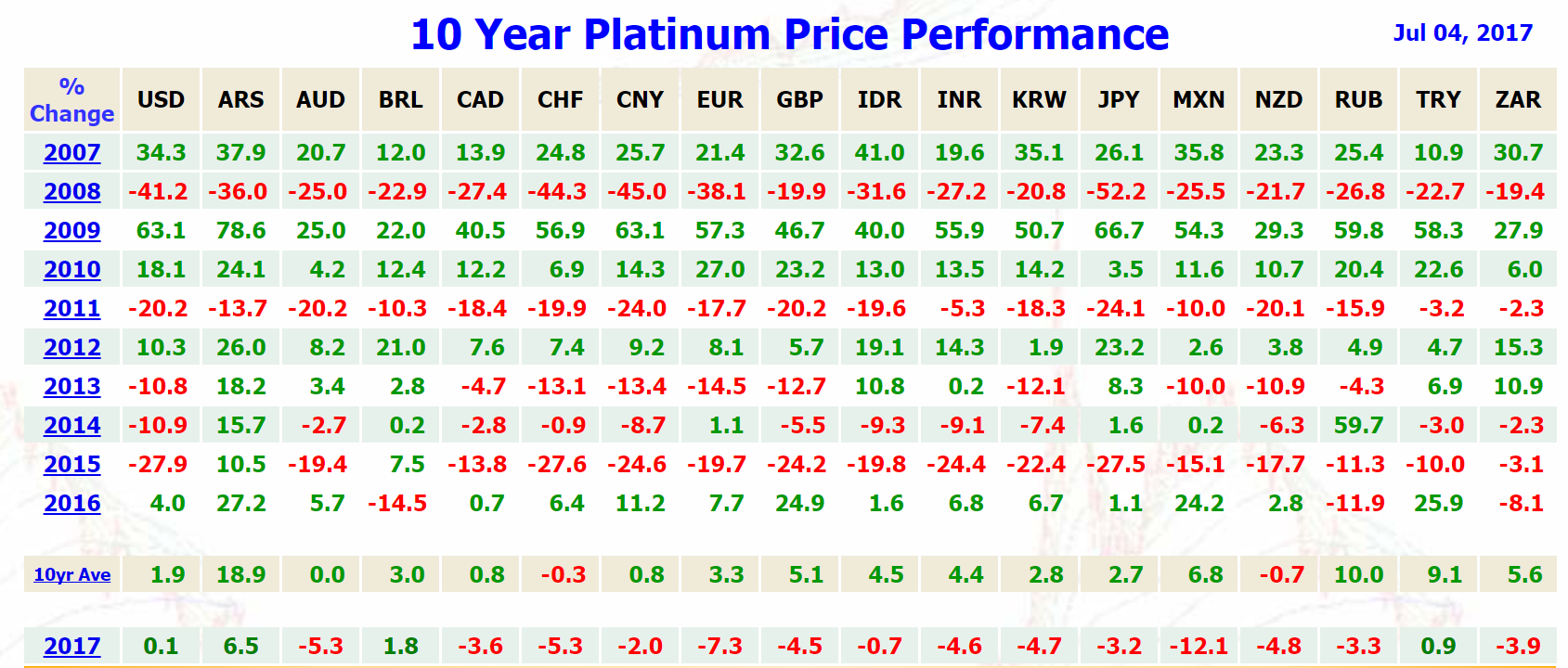

In fact, it's not only this year platinum has been falling. It has been the worst-performing precious metal over the last 10 years. After the drop seen on Monday, it has fallen four out of the last five years -- how is that for beaten down?

Source: GoldchartsRUs

Much of this drop has been attributed to the expectations of "changing consumer interests" as they purchase more gasoline vehicles vs. diesel vehicles. Since gasoline vehicles primarily use palladium in catalytic converters (diesel vehicles use platinum), the result is that industrial demand will fall for platinum -- hence surging palladium, which has almost reached parity with platinum.

While this is a strong argument, we believe that it has its flaws. That is allowing investors an opportunity to pick up platinum at what we feel is a significant discount to its true value.

Industrial Demand Loss Is Over-Exaggerated

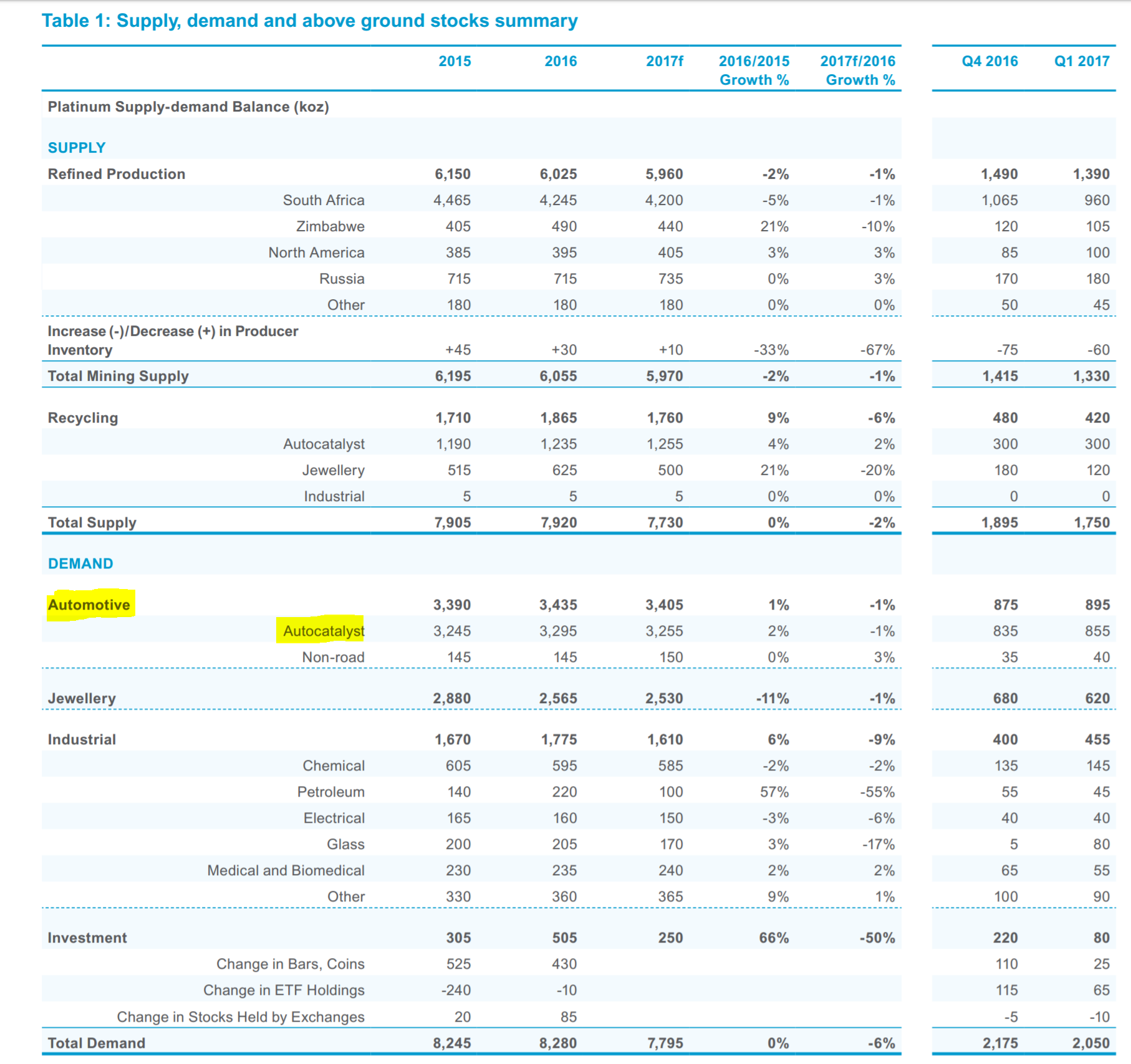

Even if we assume that analysts are correctly predicting consumer tastes, which is far from certain (like this 2013 prediction of diesel cars on U.S. roads doubling by 2018), the actual fall in diesel market share is a very slow process. In fact, according to a 2016 UBS report, this fall in market share is around 4% -- over the next decade -- from 13.5% of worldwide auto demand to 9.5%. Assuming no increase in the growth of the general automotive market, that suggests around a 3% drop a year in platinum automotive catalyst use, or around 100,000 ounces per year.

Looking at the total platinum supply/demand chart, we see that while this 100,000 year drop is sizable, it is certainly not going to kill the platinum industry.

This change in consumer automotive habits of 100,000 ounces per year through 2025 would make up a little over 1% of total platinum demand and would be entirely covered by the average 100,000-ounce drop in production seen over the past few years. Again, this all assumes that diesel's market share drops by 4% over 10 years (or a 30% drop in the total diesel market) and consumers do not increase automotive purchases (flat industry growth).

Of course, even if we do see all of this happen, the production of platinum is one of the most overlooked issues in the industry.

Platinum Mine Supply Is Due to Plummet

Platinum is a rare element and mining it is very expensive. In fact, it costs more on a per-ounce basis to mine platinum than gold. According to a report issued last September by the South Africa-based Minxcon Group, the total worldwide cash cost of platinum is $829 per ounce, with South African production (the largest producer of platinum) pegged at $980 per ounce.

I want to emphasize that we are not talking all-in sustainable costs here -- we are talking the actual cash costs of production. As in, if production falls below the cash cost of a mine, then that mine is losing money on a daily basis for the company. Depending on closure and maintenance costs, it would make more sense for a company to close the mine down than continue producing.

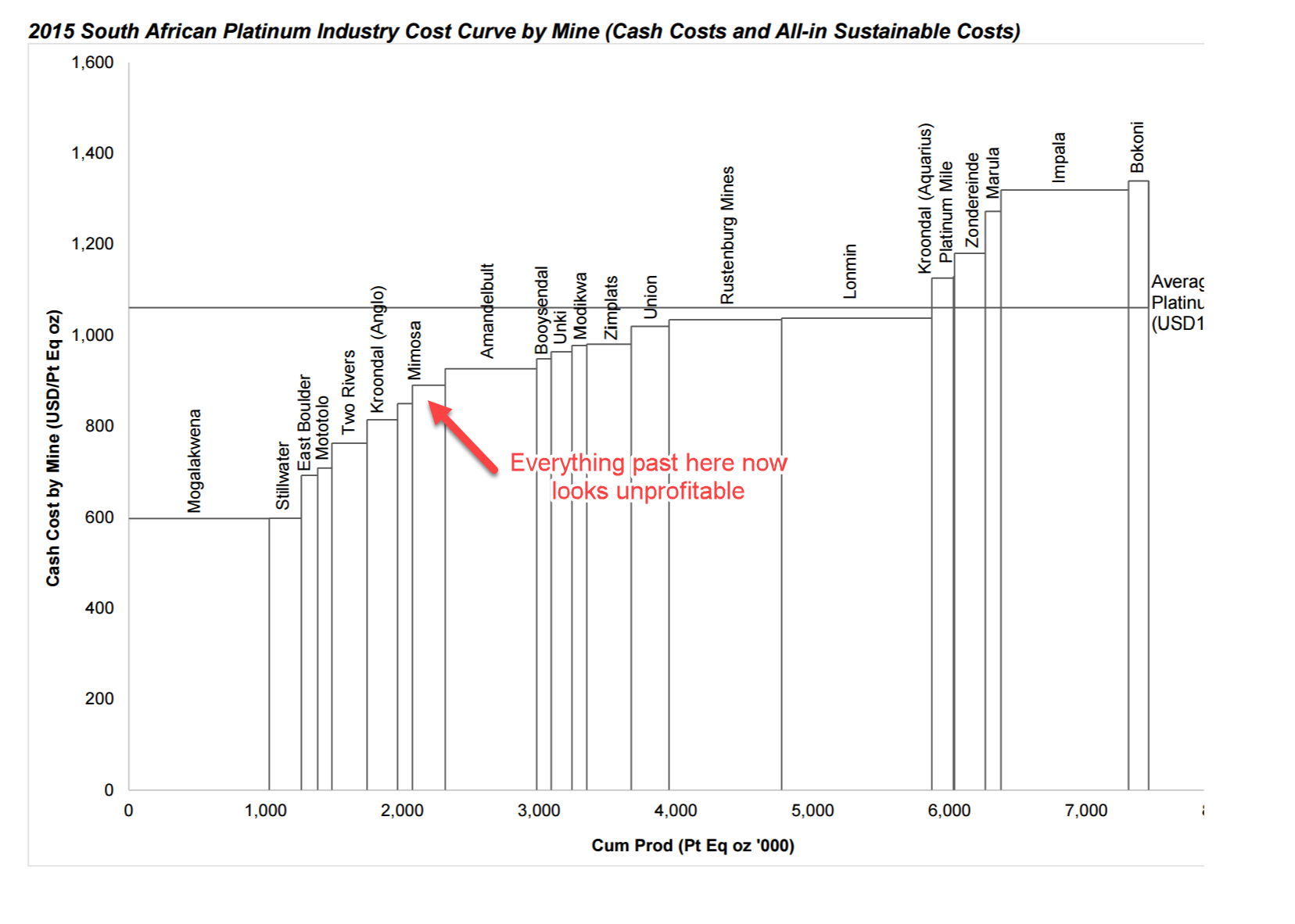

In fact, looking at the cash cost curve for South African platinum miners (where we have data), most of their production is not profitable on a cash basis.

Source: Minxcon Consulting Group (editing text is ours)

The line representing the average platinum price was dated to when platinum was trading at over $1,000; now it looks as if almost 70% of South African ounces are unprofitable. We do note that this shows platinum-equivalent production, and with surging palladium the cost structure is probably a little bit more appealing. Regardless, it shouldn't be that much different.

What this means is that we expect significant mine closures in South Africa unless we see much higher platinum prices. Investors are already shorting major platinum companies, with Lonmin (OTC:LNMIF) having the honor of being the seventh-most shorted issue on the London exchange. When companies are this cash-strapped and unable to raise cash via new equity (due to low share prices), then something has to give when trying to conserve cash. What this means is that mine closures and layoffs are on the horizon, as they simply don't have the balance sheet cash to maintain cash-losing operations.

Whether it be Lonmin or any of the other platinum miners, we expect mine closures to be announced if platinum remains under $1,000 per ounce. Just as the announcements of cuts in uranium production caused a surge in uranium prices earlier this year, we expect that whenever cuts in platinum production are announced there will be a commensurate jump in the platinum price.

Regardless, investors should expect drops in mined platinum supply at current prices, which we believe will more than make up for lost demand due to automotive consumer preferences.

Improving Emission Standards

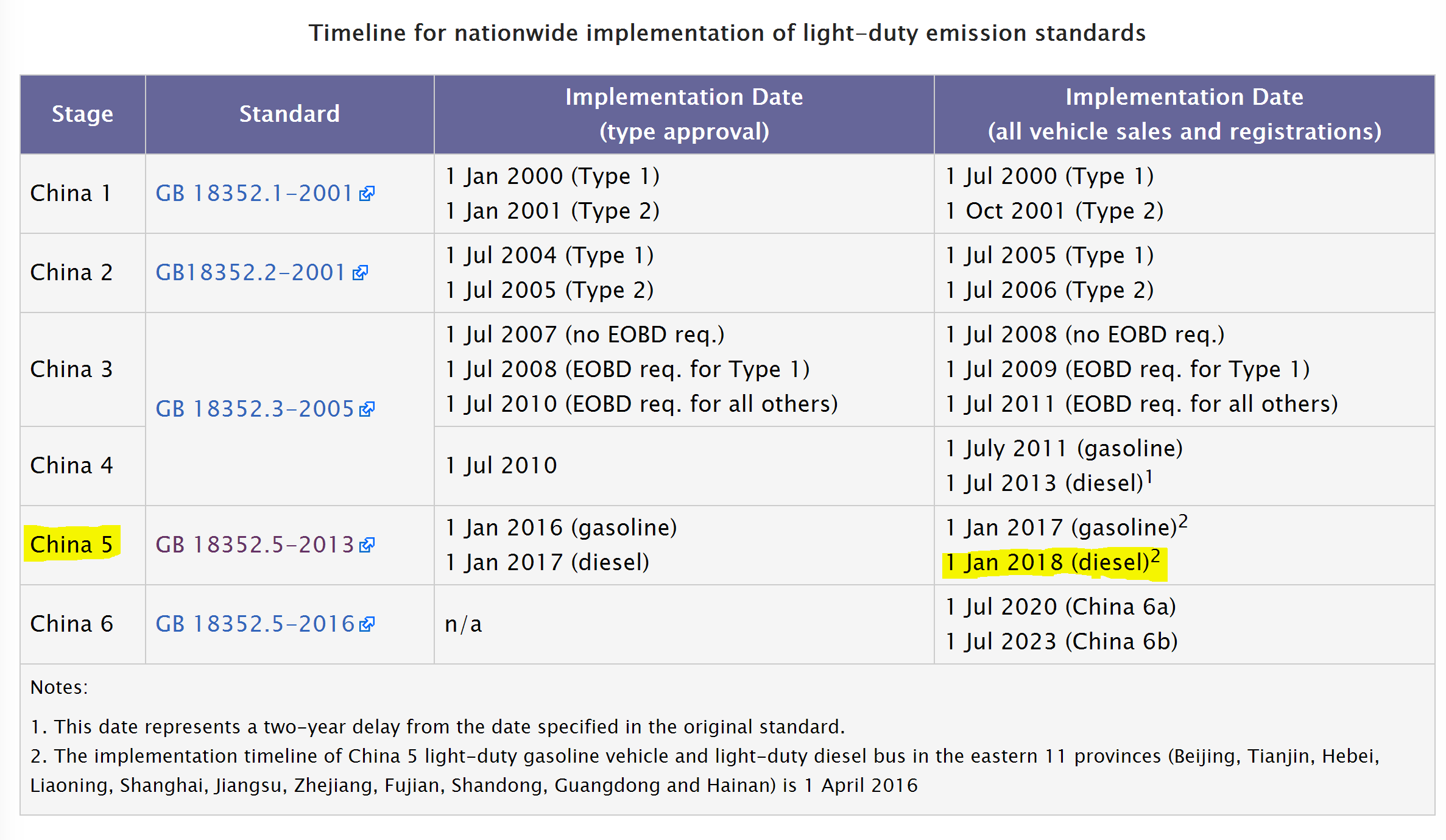

While in the U.S. the new administration is not expected to beef up any sort of emission standards, in Europe and China tougher emission standards are coming for both gasoline and diesel vehicles.

Source: Transport Policy

Similar to the Euro V standards, China's implementation of "China V" is expected in stages through 2017 as the Chinese government gets serious about its battle with pollution and smog.

What is very interesting is that standards for gasoline vehicles went into effect this past January, with the primary pollution control catalyst being palladium. While we doubt this is the main driver behind the 2017 rally in palladium, we think it certainly could have been a contributor to the physical tightness that we seem to be seeing in palladium.

These standards were implemented for gasoline vehicles this past January, but not for diesel vehicles. Starting Jan. 1, 2018, the implementation of "China V" will go into effect for diesel vehicles. Since the primary PGM used in diesel vehicles is platinum, we expect Chinese demand for physical platinum to rise as the new standards take effect in early 2018.

While we can't say it will be a game-changer, we certainly think that it could provide both a physical and psychological boost to the negativity surrounding the platinum market. Pair that with mine closures, and you have a market ripe for a rebound.

Investor Sentiment Is Rarely This Negative

Earlier this year, hedge funds did something they haven't done since records began in 2006 -- they have taken a net short position in platinum. That short position has continued up to now as the latest COT report shows that speculative traders are short by around 500,000 ounces (10,000 platinum contracts).

Source: CFTC

With such negativity among the speculative community, this allows opportunity for short squeezes and contrarian sentiment investors to take positions. This is especially true when we feel the fundamentals don't support such a low price.

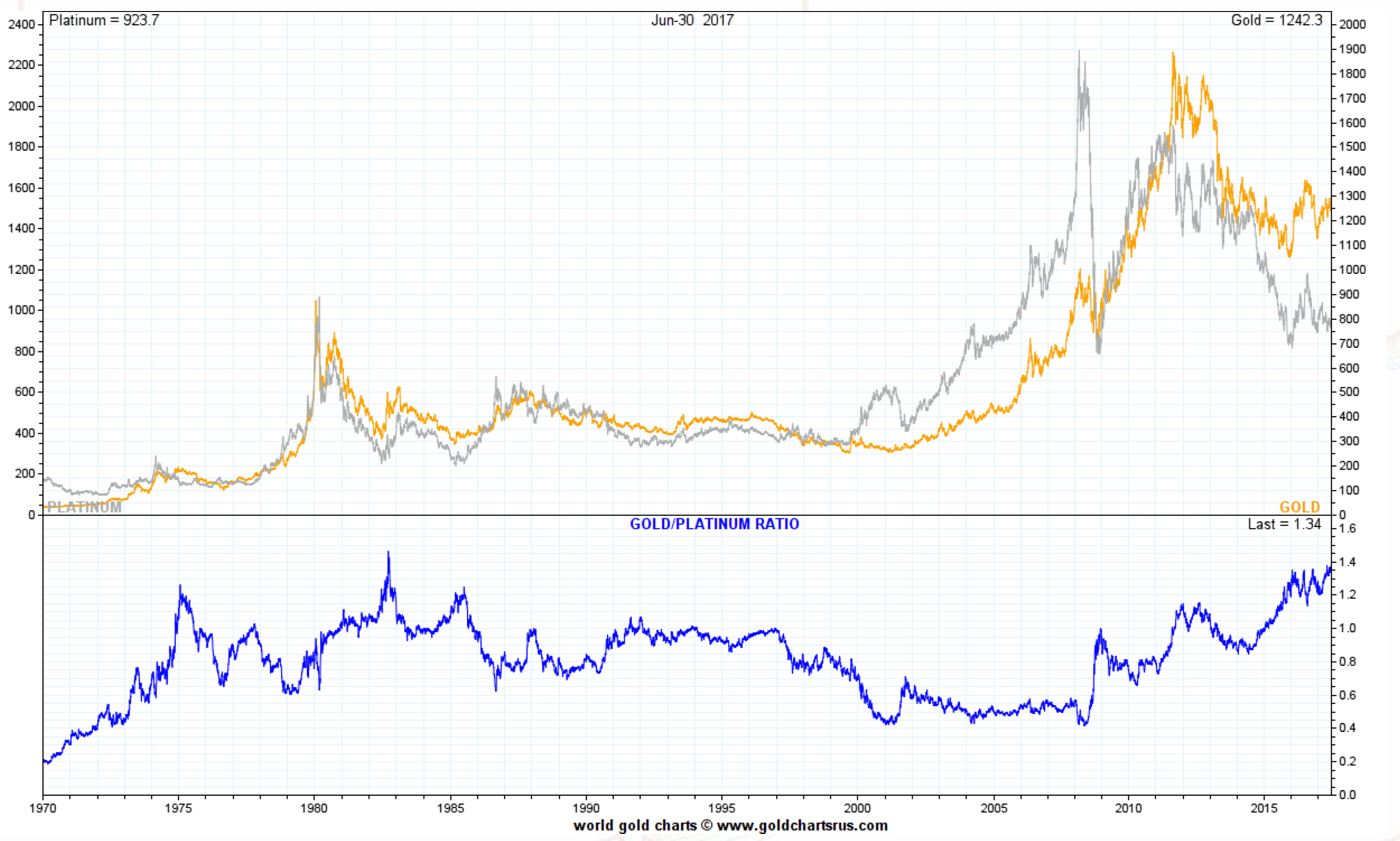

In fact, when looking at the platinum/gold ratio, our current value of 1.34 is close to the spike-highs seen over the last 50 years.

Source: GoldChartsRUS

The chart above says a lot because it shows how rare the current break between gold and platinum is historically. Also, based on this chart, we believe that the contributor of automotive demand might be a bit overemphasized as platinum was able to maintain a premium to gold through much of the last 50 years, despite its low usage as an auto catalyst in the 1970s and the increasing usage of palladium in more recent years.

Conclusion for Investors

While volatility in platinum is almost certain to continue and we cannot rule out a further drop in the metal, we think there are plenty of reasons for investors to like platinum here.

Decreasing supply as platinum drops toward its cash costs of production, mine closures in South Africa, increasing usage in China on improving emissions standards, and a potential reversal in the tremendously bearish sentiment by speculative investors are all things that could be the catalyst for a reversal in the metal.

In fact, we believe the downside in platinum is fairly limited as the cash costs of production of the metal seem to be in the mid-$800 range, which is a 5%-10% downside from current prices.

If the metal reverts to its historical parity or premium to gold, it could easily provide 20% or greater upside as it reaches parity again with gold.

Thus, if investors can be patient, we think they should seriously to consider the Sprott Physical Platinum and Palladium Trust (SPPP) or the ETFS Physical Platinum Shares (PPLT). The reversal could happen quickly as a producer going under, a significant mine closure, or a change in investor sentiment would provide a much more V-shaped recovery then a simple grind higher.

Out of all of the precious metals, we like platinum the best and we are excited about the potential upside.

0 comments:

Publicar un comentario