Alarm grows about over-exuberance in corporate lending

The nervous hear echoes of the build-up to the financial crisis

WHEN the financial crisis was at its height in 2008, being a debtor was a dreadful experience. Banks and companies scrambled desperately to get the financing they needed.

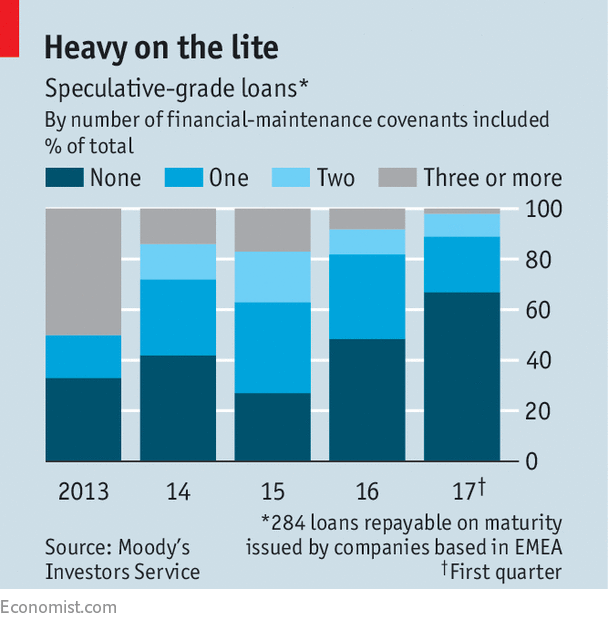

But the balance of power in the financial markets can easily shift. In 2005 and 2006, credit had been easy to get on generous terms. Not only were loans cheap and plentiful; they also suffered from fewer restrictions. Until then, corporate loans had many covenants offering safeguards for lenders if the debtor’s financial position were to deteriorate. But 2005-06 saw the emergence of “covenant-lite” loans in which such restrictions were virtually non-existent. The cycle has turned again. Analysis by Moody’s, a ratings agency, shows that the proportion of the loan market that is “covenant-lite” has risen from 27% in 2015 to more than two-thirds in the first quarter of this year (see chart). Some loans even contain restrictions on the lender, not just the borrower. Private-equity firms demand a veto over secondary-market buyers of loans they owe; the idea is to avoid the debt being bought by activist investors who might make demands on a company’s management. Investors are willing to accept such terms because they are desperate to earn some kind of yield on their assets. In the past eight years, central banks in developed economies have pushed interest rates close to zero. Government-bond yields have also been at historic lows, and some have even been negative. When low-risk assets offer a poor return, investors are willing to take more of a chance. At times like this, Wall Street always has a suitable set of initials to flog. This time, it is the collateralised loan obligation (CLO), which bundles loans together into a diversified portfolio.

As with subprime mortgages a decade ago, these portfolios are then divided into different tranches, to offer higher returns (at higher risk). CLO issuance so far this year is double the amount raised in the same period of 2016, according to Wells Fargo, a bank. Investors’ enthusiasm is not just confined to loans. Argentina recently issued a 100-year bond, despite its history of repeated defaults. With a 7.9% yield, investors clearly gambled they could get a decent return on the bond before Argentina hits economic trouble again.

Advertisement: Replay Ad

Advertisement

3

Another reason why investors are more willing to take on risk is their belief that the global economy, and the health of the corporate sector, are both improving. The global default rate on speculative bonds is down to 3.3% over the past 12 months, according to S&P Global, another ratings agency; at the start of the year, the default rate was 4.2%. Many companies have taken advantage of a long period of low interest rates to refinance their debts. But is the enthusiasm for CLOs and covenant-lite loans a sign of the same speculative excess that frothed in the middle of the previous decade? There are other straws in the wind. The Bank of England warned this week that consumers’ debt in Britain was rising faster than incomes and asked banks to put aside more capital to cover the risk of bad debts. On a scale of one to ten, one banker describes the current level of investor euphoria as “about eight”. The good news is that any shake-out in the market should be more contained than it was in the days of Bear Stearns and Lehman Brothers, whose collapse precipitated the 2008 crisis. The financial system is not as fragile as it was a decade ago; banks have more capital and are probably carrying less of this speculative debt on their own balance-sheets. Nevertheless, it is hard to escape the feeling that the market is being kept aloft by the actions of central banks. The European Central Bank (ECB) and Bank of Japan are still buying tens of billions of dollars’ worth of assets every month. That keeps yields down and prompts investors to seek alternatives. Matt King, a strategist at Citigroup, thinks that global central banks have to keep creating $1.2trn a year just to keep the markets from selling off. That creates the potential for a game of chicken between central banks and the markets. The Federal Reserve is now pushing up interest rates and may reduce the size of its balance-sheet.

China is also tightening policy; and Mario Draghi of the ECB said this week that “deflationary forces have been replaced by reflationary ones.” Central banks will move cautiously because they do not want to trigger a credit crunch. But investors are aware of this concern, and may reckon that policy will be eased again at the first sign of trouble; as a result, they may well keep lending. There is potential for serious miscalculation on both sides.

0 comments:

Publicar un comentario