Why government-bond yields have been falling again

Economic optimism and soaring stockmarkets had been expected to push them higher

EVERY year it seems that analysts and investors play a ritual game. They begin by asserting that government bonds are terrible value and that, accordingly, this must be the year when yields will rise (and prices fall). And then they get mugged by reality.

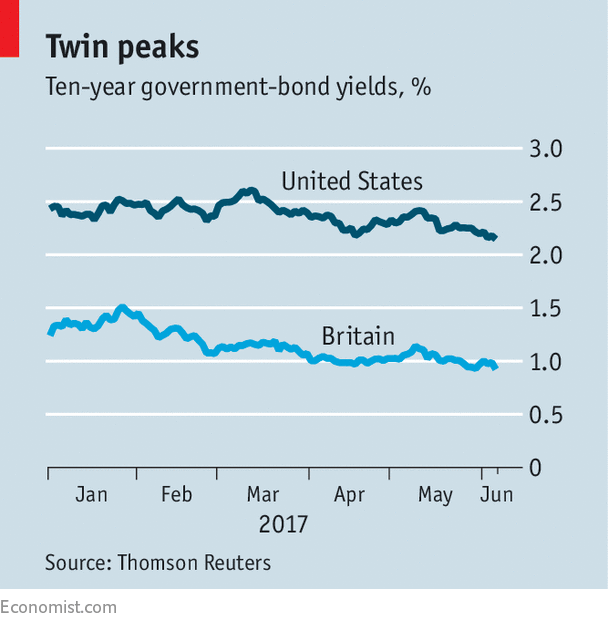

The same pattern seems to be playing out in 2017. Back in December, a poll of fund managers by Bank of America Merrill Lynch (BAML) found that pessimists on global bonds outnumbered optimists by 58 percentage points. Investors believed in a “reflation trade”, with tax cuts from Donald Trump’s administration leading to faster American growth, to which the Federal Reserve would respond with higher interest rates. For a while, such forecasts seemed to be on the money. The yield on the ten-year Treasury bond picked up to 2.63% by March 13th (see chart). But since then the trend has changed. The Treasury-bond yield recorded a low for the year of 2.13% on June 6th. In Britain the yield on the ten-year gilt dipped below 1% on June 6th and 7th; in real terms (ie, after inflation), the yield is negative. Swiss ten-year bonds still offer a negative yield: investors will lose money if they hold them until maturity.

According to BAML, by the end of May more money had flowed into global bond funds ($168bn) this year than into equity funds ($141bn).

All this is slightly at odds with the optimism that has helped push stockmarkets to repeated highs. Closing prices for the S&P 500 and NASDAQ Composite reached new peaks on June 2nd, even as the bond yield was dropping. The MSCI World Index, an equity benchmark, has risen by 10% so far this year. Global stockmarkets have been recovering since February 2016 on hopes of faster economic growth. That would usually be a signal for bond yields to rise, not fall.

Although analysts are revising their global growth forecasts upwards, there is little sign yet of any rebound in inflation. In America the core inflation rate for personal consumption expenditure, a figure watched closely by the Fed, declined to 1.5% in April. Inflation rates in China, Japan and the euro zone are all under 2%. It is inflation that saps the appeal of fixed-interest investments like bonds.

In the absence of inflation, the Fed has less reason to keep increasing interest rates. Kit Juckes of Société Générale (SG), a French bank, says the market is pricing in short-term interest rates of only 1.7% in two years’ time. “Investors are losing faith in the idea that the Fed will push rates up to 2.5% or above,” he says.

Advertisement: Replay Ad

Advertisement

3

Another reason why bond yields have retreated is that the fiscal stimulus promised by Mr Trump seems likely be delayed. The proposed infrastructure programme (actually tax credits for investors) is a long way from fruition. And the administration’s budget proposal includes cuts to popular programmes such as Medicaid that will struggle to get through Congress. Since the stimulus was expected to push up the budget deficit (and require the issuing of more bonds), any delay is good news for bond yields.

More broadly, investors have also started to worry again about a potential slowdown in the Chinese economy, amid signs that the authorities are tightening monetary policy. Commodity prices, seen as an indicator of Chinese demand, are at a 12-month low.

If these worries are real, why is the stockmarket doing so well? One reason is the strength of corporate profits. According to Factset, annual profits growth in the first quarter for companies in the S&P 500 index was around 14%. Part of this is the result of a rebound in energy companies’ earnings, after a slump in the oil price dropped out of the annual comparisons. But global profits forecasts for 2017 are still being revised higher.

Companies are benefiting because there is little sign of wage pressure. Even though the American unemployment rate dropped to 4.3% in May, year-on-year growth in average earnings in America was just 2.5%. “Labour is in demand because it is cheap,” say analysts at Rabobank. In turn, subdued wage growth means there is little upward pressure on inflation—good news for bonds.

This helps to explain why investors keep getting caught out in their expectations for the bond market.

In a normal economic cycle, bond yields would be heading a lot higher by now. But it has been pretty clear since 2008 that these are not normal economic times. Perhaps investors should have reflected on the example of Japan, where bond yields have stayed low for two decades despite the ups and downs of the cycle.

0 comments:

Publicar un comentario