Why Does The Stock Market Continue To Levitate?

by: Lawrence Fuller

- The resiliency of the stock market in the face of geopolitical uncertainty and deteriorating fundamentals is astonishing.

- The only logical explanation is the record pace of liquidity being created by central banks.

- This has created two economies that continue to diverge.

- The question is not whether or not we are in a bubble, but how and when it will end.

- The only logical explanation is the record pace of liquidity being created by central banks.

- This has created two economies that continue to diverge.

- The question is not whether or not we are in a bubble, but how and when it will end.

The resiliency of the US stock market is truly amazing, refusing to give up as little as 2-3% for any more than a few days, or hours, before powering higher. This continued levitation comes regardless of whether the news is good, bad or indifferent. We often hear that the latest "relief" rally was the result of a better-than-expected outcome from a political or economic event or announcement. Yet to rally in relief suggests that the market suffered a meaningful decline in anticipatory angst over such an event or announcement, but that never happens. This is just an attempt to provide a rational explanation for what has become a very irrational market.

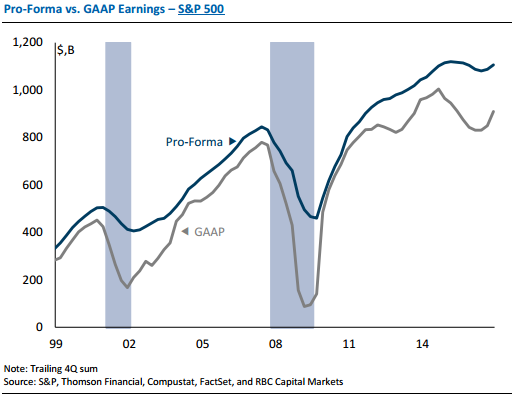

Still, I search every day for fundamental reasons that might justify the stock market's current valuation, much less a higher one, but I can't find any. Wall Street often cites the return to earnings growth for the S&P 500 (NYSEARCA:SPY), but the current situation is more of a recovery than a growth story. If we use the pro-forma, or adjusted, earnings figures, which vary from one company to another depending on how many expenses they exclude as questionable one-time items to inflate their bottom line, earnings are still below the level achieved in 2014. If we use the numbers all companies are required to report, based on generally accepted accounting principles, the results are well below that of 2014. This standard doesn't show much of an earnings recovery.

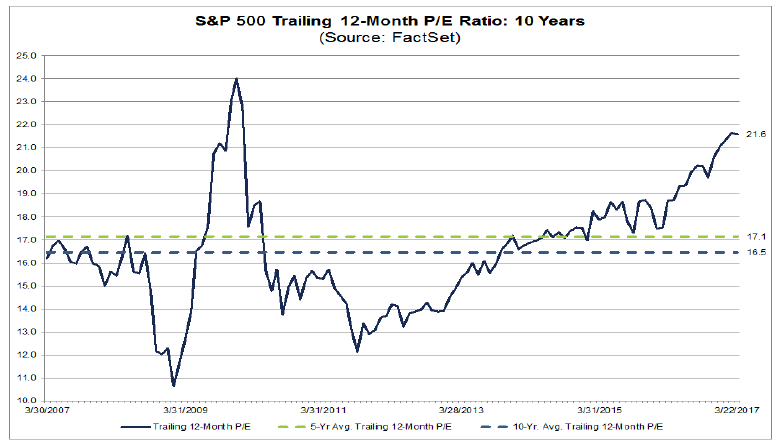

Despite this earnings stagnation, valuations have continued to climb to levels only topped just prior to the bursting of the technology bubble in 2000 and the housing bubble in 2008. This doesn't give me confidence in my long-term investment outlook.

How do we explain what is happening today? I was stunned by a recent interview on CNBC of legendary investor Asher Edelman, who explained that the government's "plunge protection team" has been actively propping up stock prices. This group, otherwise known as the "Working Group on Financial Markets," was created by Ronald Reagan following the crash in 1987. Edelman believes that the PPT is operating through the New York Fed (which serves as the money manager for the Federal Reserve) and politically connected hedge fund goliaths, such as Citadel.

This sure would explain a lot of the peculiar stock market activity we have seen in recent months and years, as well as the incredibly subdued level of volatility despite heightened levels of geopolitical stress. I can find nothing either to support or to discount Edelman's assertion, but I think there is a far more simple and obvious explanation.

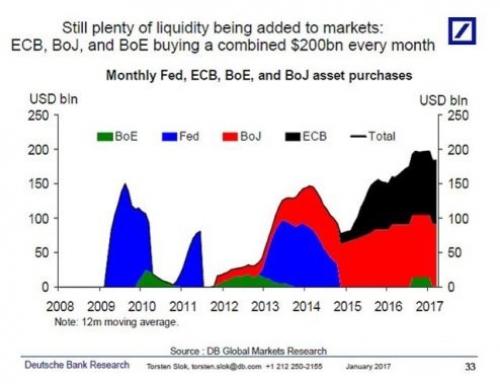

Central banks around the world, led by the European Central Bank, continue to buy financial assets at a rate that is approaching $200 billion a month. This unprecedented liquidity is what is propping up US stock prices either directly, or indirectly through the purchase of lower risk assets.

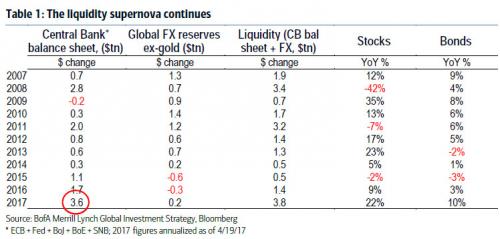

Central banks purchased a record $1 trillion through the first four months of this year, and are on pace to increase liquidity by a record $3.6 trillion in 2017.

I think this explains why the amount of sovereign debt around the world carrying a negative yield is approaching $10 trillion, meaning that an investor is willing to accept a negative rate of return to hold the bond until maturity. It also explains why stocks, bonds and even the safe haven of gold are all rising in price at the same time. There is so much liquidity in search of a home that any reallocation from one asset class to another has a muted impact.

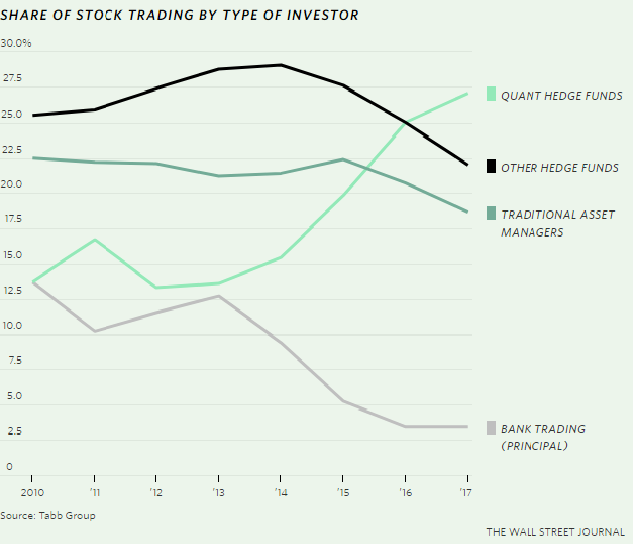

Further exacerbating the divergence between financial markets and economic fundamentals is the growing dominance of mindless computerized trading. I think this explains the nonsensical intraday moves in broad stock-market indices. JPMorgan (NYSE:JPM) asserts that just 10% of trading is done by fundamental discretionary traders today. Hedge funds that manage money using quantitative computer models command nearly $1 trillion in assets and dominate trading activity.

We have a tsunami of liquidity that is fueling financial markets on a global basis, as computerized trading models that could care less about what happened yesterday, or what may happen tomorrow, continue to gain dominance. If this isn't an accident waiting to happen, then I don't know what is. It most definitely explains why markets grow ever more decoupled from economic fundamentals.

What global central banks, led by the Federal Reserve, either refuse to admit or never understood in the first place is that all this excess liquidity has done very little for the real economy. Instead, it has created two economies.

Due to several factors outside the focus of this discussion, consumer demand for goods and services during this recovery has been extraordinarily weak. Regardless, the Federal Reserve continued to increase liquidity and ease financial conditions. Other central banks followed. The benefactors of this monetary policy largesse saw no reason to invest in the real economy, nor do they today, because demand remains so weak. Therefore, they invest in the financial economy where money is made with money rather than with real businesses.

We may be approaching the day when the growing disparity between the real economy and its financial counterpart comes to an end. This week the Federal Reserve announced its intention to shrink its $4.5 trillion bond portfolio, thereby reducing the available liquidity in financial markets and potentially leading to an increase in long-term interest rates. If this occurs in combination with a deceleration in the rate of purchases by the ECB and other central banks, it could have a meaningful impact on market prices.

All that I can conclude for now is that we are either in or rapidly approaching bubble territory in both stock and bond prices. High valuations alone do not necessarily mean that a significant price decline will happen in the near future, but there has always been a reversion to the mean from those high valuations. The question is where does that mean lie, and when will the reversion happen.

0 comments:

Publicar un comentario