Vicious VIX: Jason Miller Made $53,000, But Larry Tabb Got Bilked

by: The Heisenberg

- The VIX debate has found its way onto the front page of the Wall Street Journal.

- By way of a series of amusing anecdotes, WSJ explains why it's dangerous for retail investors and even some "pros" to trade volatility via popular VIX ETPs.

- The piece quotes Deutsche Bank's Rocky Fishman, whose analysis I've been highlighting for months.

- Here's an in-depth look at one of the more important issues facing markets today.

- By way of a series of amusing anecdotes, WSJ explains why it's dangerous for retail investors and even some "pros" to trade volatility via popular VIX ETPs.

- The piece quotes Deutsche Bank's Rocky Fishman, whose analysis I've been highlighting for months.

- Here's an in-depth look at one of the more important issues facing markets today.

"One person's fear is another person's opportunity."

That's from noted market sage, newly-minted futures trader, and 40-year-old Boca Raton day trader Jason Miller, who took some time away from hitting the refresh button on his online brokerage account home page to tell the Wall Street Journal how he's made $53,000 so far this year in short VIX ETPs (NASDAQ:XIV).

As the Journal notes, "that includes a white-knuckle day on May 17, when the VIX spiked 46% following reports that President Donald Trump had pressured former FBI Director James Comey to drop an investigation into former National Security Advisor Michael Flynn."

Miller, undeterred, "rode out the storm, confident the market would revert to its torpid ways - which it did."

The article that features that rather amusing anecdote is called "The Snowballing Power Of The VIX," and you should read it. Because it underscores a point I and many others have been pounding the table on for months: allowing retail investors to short volatility has embedded all kinds of risk in this market.

At issue is the now ubiquitous "doom loop," wherein central bank liquidity artificially suppresses volatility, which in turn allows programmatic/systematic strats like risk parity, CTAs, and volatility control funds to lever up their positions. The concern is that the more suppressed volatility gets, the smaller the nominal spike needed to trigger short covering in VIX ETPs. That short covering could exacerbate said spike, an eventuality which might then force the systematic strats mentioned above to deleverage into a falling market.

Both in these pages, and more extensively over at HR, I've been documenting notes from Deutsche Bank's Rocky Fishman, who writes prolifically about this dynamic. Here's an excerpt from a recent note:

VIX ETPs are a larger-than-usual feedback loop in markets. Inverse and levered VIX ETPs' need to buy VIX futures when vol is rising and sell it when vol is falling creates a feedback loop in vol that can lead to high vol-of-vol. Currently, the combination of low VIX futures levels (making an N-point vol spike look like a huge percentage), large short ETPs, and large levered ETPs leaves over $70mm vega to buy on a hypothetical 5-vol spike in the VIX futures curve.

Unsurprisingly, The Journal piece linked above cites Fishman. Here's the passage:

In a twist, the very funds that are meant to protect against volatility may make any correction worse, says Rocky Fishman, an equity-derivative strategist with Deutsche Bank. So-called "volatility control" funds aim to provide investors with a smoother ride by sidestepping the worst dips. A rising VIX signals the funds to shed stocks in favor of safer assets, accelerating the selloff and spooking other investors into joining the exodus.

Rising volatility triggered $50 billion in stock selling during the market gyrations of August 2015, and $25 billion in the wake of the U.K.'s surprise vote to exit the European Union last year, according to Mr. Fishman.

"It's a feedback loop that can make selloffs unfold faster," says Mr. Fishman.

"There are fund managers whose job it is to sell equities when volatility goes up. And that affects everyone."

I would (strongly) encourage you to read Fishman's analysis in full, as those quotes are just the tip of the proverbial iceberg. As usual, Heisenberg has you covered. Here are two posts where you can read the details:

- Feed Your "VIX-ation" - Rocky's Back To Answer All Your VIX Questions

- Here's The "Not Unthinkable" Nightmare Scenario For Short VIX Strats

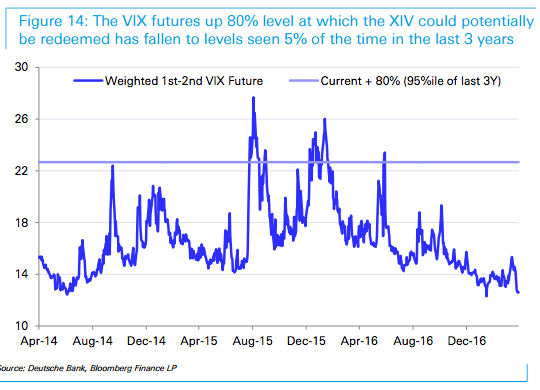

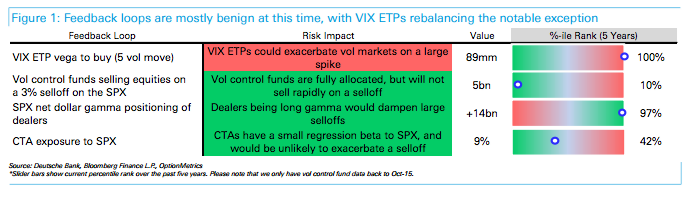

The inherent danger in the feedback loop Fishman describes can't be emphasized enough. It was the subject of a recent post I called "Investigating The Market's 'Nightmare Scenario.'"

There's more analysis from the above-mentioned Fishman in that post which finds Rocky noting that while the risk is high that VIX ETPs (NYSEARCA:VXX) could tip the first domino, he suggests the other dominoes might not fall as the situation stands now.

Here's a handy table that illustrates that point (and again, these things change by the day, but this will give you a good idea of what he's talking about):

(Deutsche Bank)

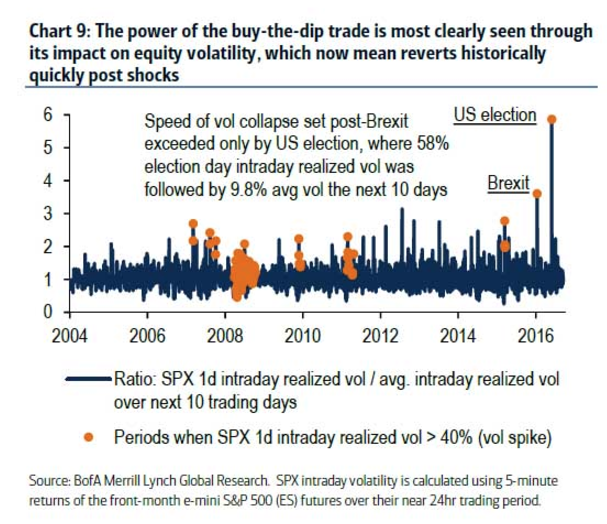

The problem (again) is that by perpetuating the "buy-the-dip" mentality, central banks are creating and fostering an environment where the market can't price risk correctly. Simply put, volatility spikes immediately "mean revert". This is something BofAML has been keen on flagging for a couple of months now.

Here's a chart that illustrates the phenomenon in volatility:

(BofAML)

And here's what it looks like in equities themselves:

(JPMorgan)

That's what's allowed day traders like Jason Miller to clock staggering returns selling volatility via VIX ETPs.

Obviously, the problem here is that the Jason Millers of the world i) would in all likelihood never be doing this if VIX ETPs didn't exist, ii) have no idea the extent to which this trade depends on central banks, and iii) do not know that they are perpetuating an insanely dangerous dynamic by (literally) forcing programmatic strats controlling hundreds of billions of dollars to lever up.

Ultimately, it's not clear that retail investors should be able to employ this strategy. And indeed, it's not even clear that anyone outside of seasoned traders and/or hedge funds has any business doing this. Think I'm exaggerating? Well, consider another excerpt from the Journal's article:

Trading the VIX, however, is a lot different from watching it on TV, and its idiosyncrasies left some investors feeling burned. No trading strategy can exactly replicate the VIX index, and traders rely on proxies like futures and options, which can veer widely from the VIX itself.

VIX exchange-traded products are especially susceptible to this divergence because of the peculiar structure of VIX futures.

Some of the most popular exchange-traded products invest in a combination of this month's VIX futures and next month's. To maintain their exposure, they sell the contracts that are nearing expiration and buy contracts for the following month. Put simply, they buy high and sell low almost every day, steadily bleeding money.

This decay is difficult to comprehend, even for sophisticated investors, and leveraged funds can compound those losses. Market experts say the products are designed for short-term tactical trading, not long-term passive investment.

When the VIX dipped in September, Larry Tabb, president and founder of the Tabb Group, a consulting firm, thought volatility would rise and bought an exchange-traded product that aims to double the daily gain of VIX futures. And even though the VIX rose 28% in October, the VelocityShares Daily 2x VIX Short-Term ETN lost money.

"It just kept going down and down and down," says Mr. Tabb, who blames himself for not reading up on its mechanics before buying. "I got completely screwed."

I don't want to pick on Larry, but read this description from the "About" section of Tabb Group's official website:

TABB Group is the international research and consulting firm focused exclusively on capital markets, founded on the interview-based research methodology developed by Larry Tabb. Since 2003, TABB Group has been helping business leaders gain a truer understanding of financial markets issues to develop actionable roadmaps and approaches to future growth.

Again, not to deride Mr. Tabb, but come on, man. That just further supports my contention that the vast majority of market participants (let alone retail investors) have no business whatsoever pretending to be VIX futures traders.

Remember what you're doing when you sell volatility. Here's Deutsche Bank's Aleksandar Kocic to explain (full note here):

Volatility declines either when the markets are predictable or when there is no consensus. Dissensus has emerged as a new paradigm - an absolute inability to form consensus across variety of contexts, accompanied with an onset of a breakdown of conventional frames of reference. So, what does one do when no decision can be made? Well, one waits.

Selling gamma is an act of abandonment of denial of immediacy. In the same way that issuing debt is equivalent to selling future time (a creditor has an implicit claim on debtor's future), shorting gamma means selling waiting time. Waiting time as an asset is highly undesirable - no one wants to be long waiting time. Short gamma is a way of disposing of it. This means that you can sell something you don't want and get paid for it.

That is a risky trade.

But a combination of central bank liquidity and the mentality (buy-the-dip) that liquidity has instilled in markets has made it seem more like a riskless trade.

Here's what Citi said late last week with regard to the lack of reaction in European credit spreads following the surprising result of the UK elections:

The common theme remains the remarkable ability of the market to shrug off seemingly any amount of political or economic uncertainty - provided the central banks keep promising to work their magic. As such, to us the spread outlook in both € and £ therefore depends much less on the rather intractable complexities of the political and economic outlook than it does on the minutiae of whether and when central banks remove some of their currently extreme accommodation.

For now, with the punch bowl (or is it a magician's hat?) still full of liquidity, the high opportunity cost of not investing is helping to sustain the status quo. But that doesn't mean that asset prices have actually managed to decouple from central bank balance sheet expansión.

For the last time: the problem is that the vast majority of people selling volatility have no idea that this is what they're betting on and they have even less of an idea about the kind of systemic risks they're creating in markets by participating in the incessant "selling of waiting time" (to quote Deutsche's Kocic again).

Ultimately, I would encourage you to try and understand this for precisely what it is. Because when you do, you'll understand why it is that this discussion has now found its way onto the front page of the Wall Street Journal.

0 comments:

Publicar un comentario