The Fed Is Hawkish - Should Gold Investors Be Bearish Too?

by: Hebba Investments

- Despite the sizable drop in gold during the COT week, we saw relatively muted speculators activity.

- In silver speculative longs maintained their positions while shorts increased on the week.

- During the Fed's press conference, Janet Yellen was surprisingly hawkish which caused gold to drop.

- Even though a hawkish Fed is normally not good for gold, we think the probabilities are rising that the Fed is making a policy mistake.

- Any Fed policy mistake would be bad for markets and good for gold.

- In silver speculative longs maintained their positions while shorts increased on the week.

- During the Fed's press conference, Janet Yellen was surprisingly hawkish which caused gold to drop.

- Even though a hawkish Fed is normally not good for gold, we think the probabilities are rising that the Fed is making a policy mistake.

- Any Fed policy mistake would be bad for markets and good for gold.

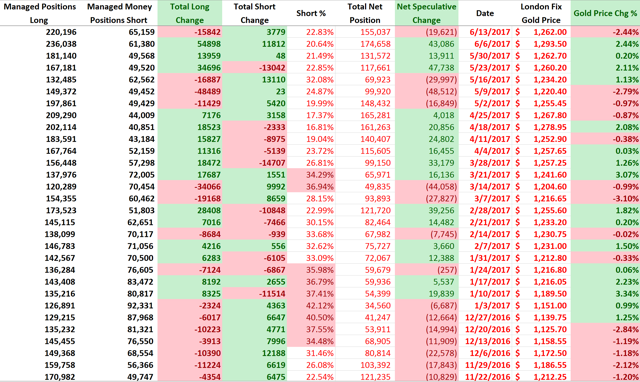

The latest Commitment of Traders ((NYSE:COT)) report predictably showed a week of speculators selling gold positions and initiating speculative shorts. Though despite the large gold drop on the COT week (2.4%), the speculative change on the week was relatively minor - we would have expected more long positions being sold or short positions initiated.

The big event for the week was obviously the Fed statement and conference on Wednesday, but unfortunately those COT positions will not be published until next week - you can complain to the CFTC about still publishing dated reports and not giving us a little more current data.

Having said that, the change in gold since Tuesday's COT positional close and the Friday close is only around 1%, so we don't think positions are too different from what we see today.

We will get more into some of these details but before that let us give investors a quick overview into the COT report for those who are not familiar with it.

About the COT Report

The COT report is issued by the CFTC every Friday, to provide market participants a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. In plain English, this is a report that shows what positions major traders are taking in a number of financial and commodity markets.

Though there is never one report or tool that can give you certainty about where prices are headed in the future, the COT report does allow small investors a way to see what larger traders are doing and to possibly position their positions accordingly. For example, if there is a large managed money short interest in gold, that is often an indicator that a rally may be coming because the market is overly pessimistic and saturated with shorts - so you may want to take a long position.

The big disadvantage to the COT report is that it is issued on Friday but only contains Tuesday's data - so there is a three-day lag between the report and the actual positioning of traders. This is an eternity by short-term investing standards, and by the time the new report is issued it has already missed a large amount of trading activity.

There are many ways to read the COT report, and there are many analysts that focus specifically on this report (we are not one of them) so we won't claim to be the exports on it.

What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

This Week's Gold COT Report

*Gold price data reflects the COT week (Tues-Tues) not a standard week (Mon-Fri)

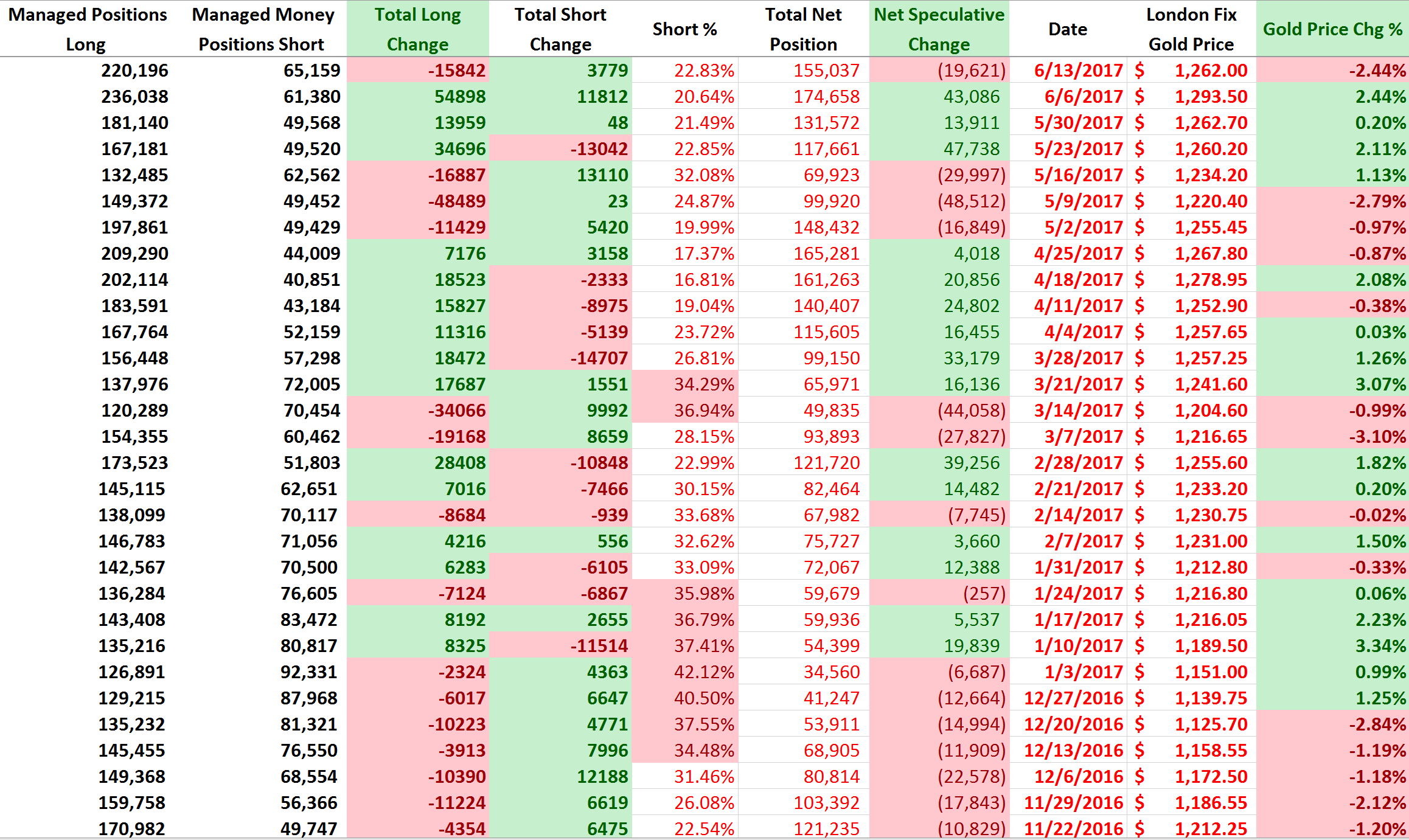

After three consecutive weeks, speculative longs cut back on their long positions by 15,842 contracts, which was actually lower than we would have expected considering the 2.4% drop in the gold price.

Additionally, we saw speculative shorts increasing their own positions by 3,779 contracts - which was also fairly slim for the large drop we saw this week in gold. This is telling us that speculators are still fairly bullish on gold and are reluctant to take the short side of the gold trade.

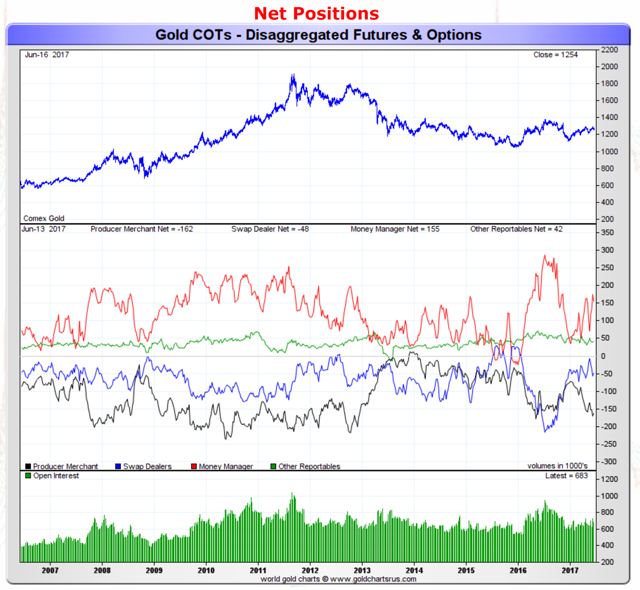

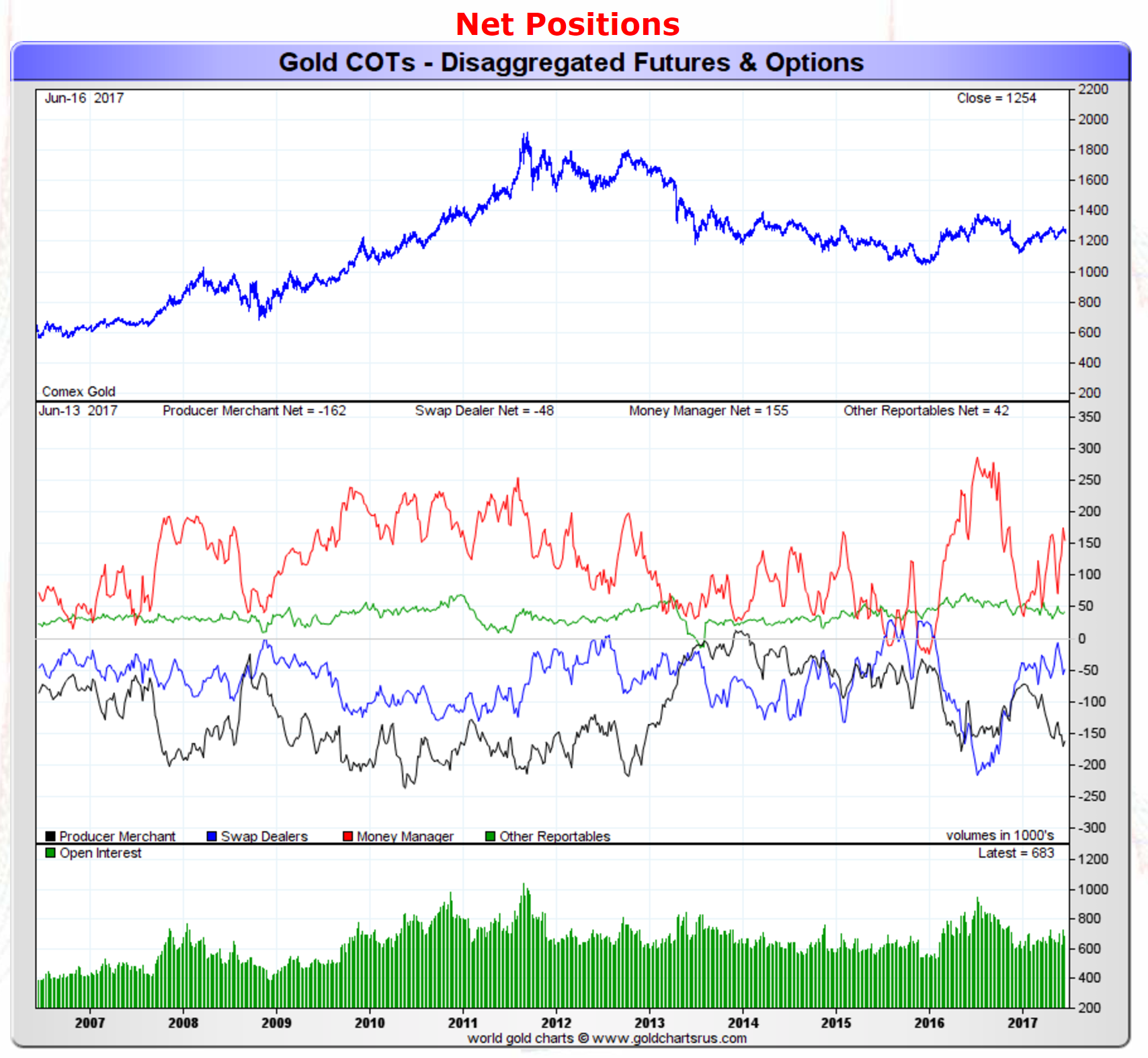

Moving on, the net position of all gold traders can be seen below:

Source: GoldChartsRUS

The red-line represents the net speculative gold positions of money managers (the biggest category of speculative trader), and as investors can see, we saw the net position of speculative traders decreased by around 20,000 contracts to 155,000 net speculative long contracts. We still remain at net speculative long positions that are on the high side of historical averages.

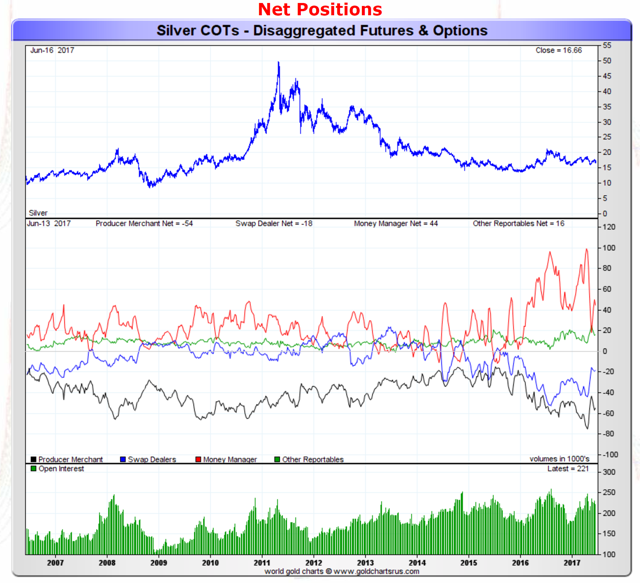

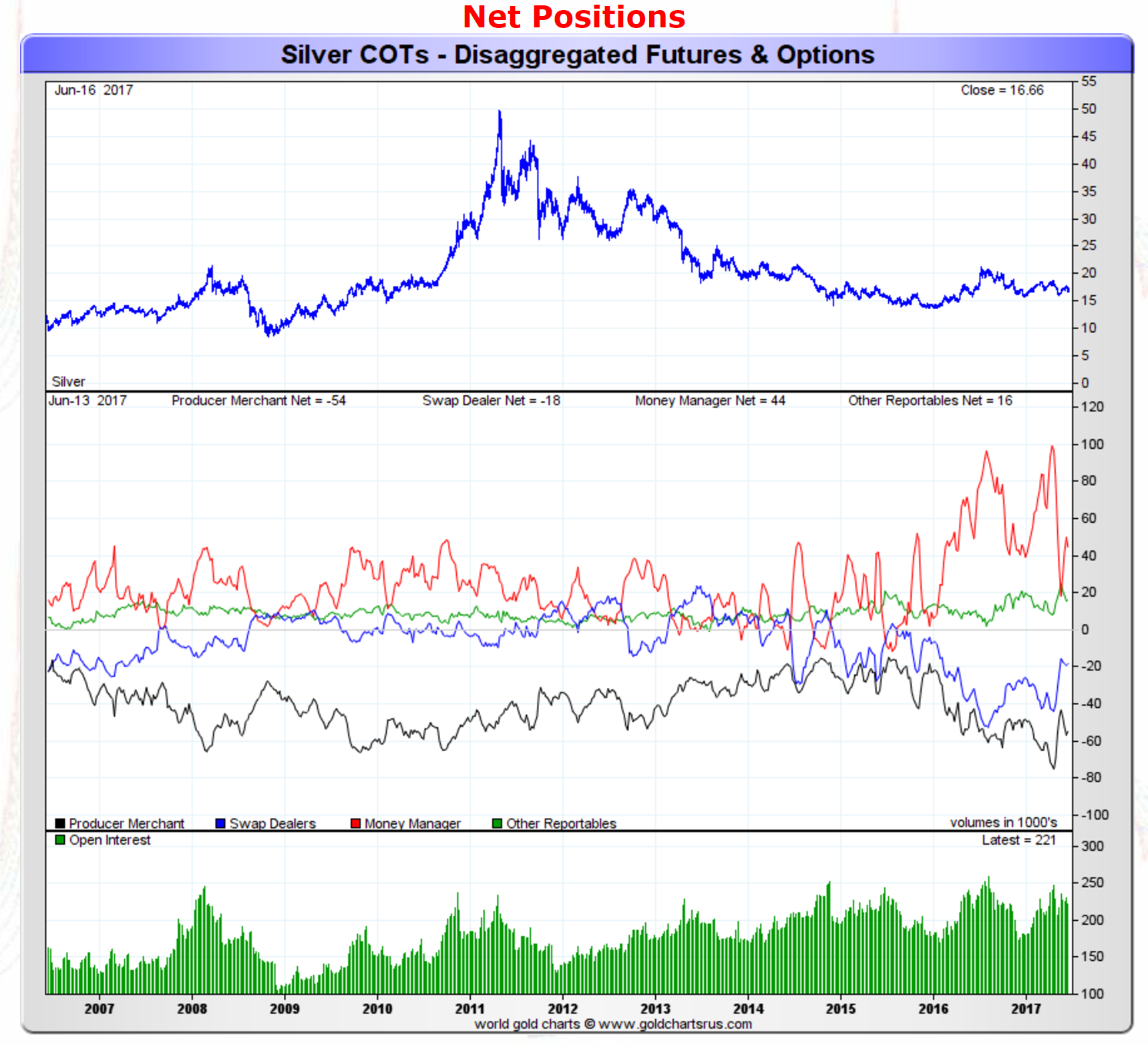

As for silver, the action week's action looked like the following:

Source: GoldChartsRUS

The red line which represents the net speculative positions of money managers, showed a decrease in the net-long silver speculator position as their total net position rose by around 6,000 contracts to a net speculative long position of 44,000 contracts. Most of this was due to an increase of shorts (around 5,000 contracts) with very little net action on the long side.

The Fed Meeting

The big event last week was the Fed meeting, which interestingly enough led to a large drop in gold after it had soared earlier in the day after disappointing retail sales and inflation data. The reason for the drop was attributed to a hawkish Fed that seemed more concerned about inflation than boosting the economy by letting inflation run a little "hot".

It was a bit surprising that the Fed was so focused on inflation rather than the weak economy - and certainly the fact they were considering cutting back on their balance sheet is concerning.

How does the Fed expect to keep rates under control if even they start selling bonds?

But we think Ben Hunt of Salient Partners summarized the shift best (emphasis ours):

There is one BUT…

If the Fed is tightening into a weak economy that is over-leveraged with debt, then the Fed is making a big mistake. This policy error would have huge consequences as what would happen would be that higher interest rates would choke a weak real economy that only looks strong based on the stock market's rise - which would quickly reverse. That in turn would lead to defaults and bankruptcies that would snowball through the economy, like in 2007 EXCEPT that we have way more debt now.

In fact, we believe that gold SHOULD have fallen much more on the Fed statement then it did as it was only down around 1% on the week. We think there is some sizable "Fed policy error" buying in gold that is maintaining its $1250+ Price.

Our Take and What This Means for Investors

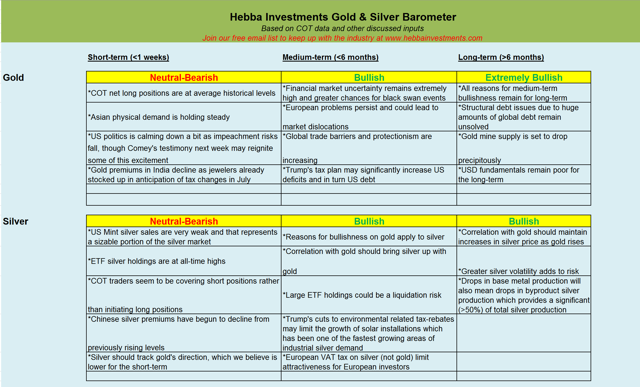

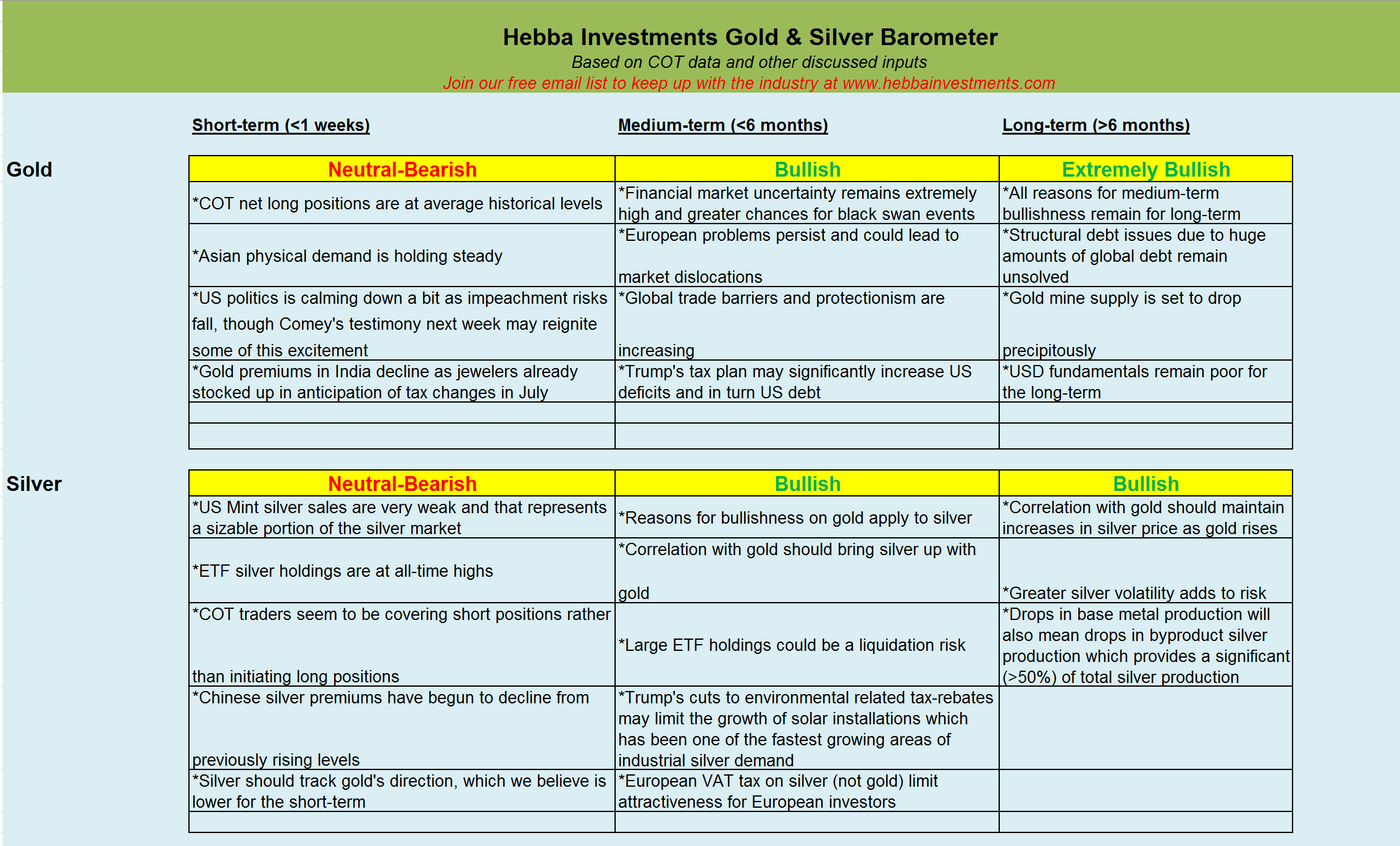

Despite our view that the Fed is making a policy mistake by raising rates and maintaining a hawkish view on inflation, we remain short-term Neutral-Bearish on gold and silver as we believe that hawkish stance is what investors will focus on.

We eventually think that will change as investors start seeing the Fed's position as a big policy mistake, but we think that gold bulls should give it a week or so for the Fed's position to be digested by markets. Thus for us it seems prudent to wait on purchasing additional gold and silver positions (SPDR Gold Trust ETF (NYSEARCA:GLD), iShares Silver Trust (NYSEARCA:SLV), Sprott Physical Silver Trust (NYSEARCA:PSLV), and ETFS Physical Swiss Gold Trust ETF, etc).

The big event for the week was obviously the Fed statement and conference on Wednesday, but unfortunately those COT positions will not be published until next week - you can complain to the CFTC about still publishing dated reports and not giving us a little more current data.

Having said that, the change in gold since Tuesday's COT positional close and the Friday close is only around 1%, so we don't think positions are too different from what we see today.

We will get more into some of these details but before that let us give investors a quick overview into the COT report for those who are not familiar with it.

About the COT Report

The COT report is issued by the CFTC every Friday, to provide market participants a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. In plain English, this is a report that shows what positions major traders are taking in a number of financial and commodity markets.

Though there is never one report or tool that can give you certainty about where prices are headed in the future, the COT report does allow small investors a way to see what larger traders are doing and to possibly position their positions accordingly. For example, if there is a large managed money short interest in gold, that is often an indicator that a rally may be coming because the market is overly pessimistic and saturated with shorts - so you may want to take a long position.

The big disadvantage to the COT report is that it is issued on Friday but only contains Tuesday's data - so there is a three-day lag between the report and the actual positioning of traders. This is an eternity by short-term investing standards, and by the time the new report is issued it has already missed a large amount of trading activity.

There are many ways to read the COT report, and there are many analysts that focus specifically on this report (we are not one of them) so we won't claim to be the exports on it.

What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

This Week's Gold COT Report

*Gold price data reflects the COT week (Tues-Tues) not a standard week (Mon-Fri)

After three consecutive weeks, speculative longs cut back on their long positions by 15,842 contracts, which was actually lower than we would have expected considering the 2.4% drop in the gold price.

Additionally, we saw speculative shorts increasing their own positions by 3,779 contracts - which was also fairly slim for the large drop we saw this week in gold. This is telling us that speculators are still fairly bullish on gold and are reluctant to take the short side of the gold trade.

Moving on, the net position of all gold traders can be seen below:

Source: GoldChartsRUS

The red-line represents the net speculative gold positions of money managers (the biggest category of speculative trader), and as investors can see, we saw the net position of speculative traders decreased by around 20,000 contracts to 155,000 net speculative long contracts. We still remain at net speculative long positions that are on the high side of historical averages.

As for silver, the action week's action looked like the following:

Source: GoldChartsRUS

The red line which represents the net speculative positions of money managers, showed a decrease in the net-long silver speculator position as their total net position rose by around 6,000 contracts to a net speculative long position of 44,000 contracts. Most of this was due to an increase of shorts (around 5,000 contracts) with very little net action on the long side.

The Fed Meeting

The big event last week was the Fed meeting, which interestingly enough led to a large drop in gold after it had soared earlier in the day after disappointing retail sales and inflation data. The reason for the drop was attributed to a hawkish Fed that seemed more concerned about inflation than boosting the economy by letting inflation run a little "hot".

It was a bit surprising that the Fed was so focused on inflation rather than the weak economy - and certainly the fact they were considering cutting back on their balance sheet is concerning.

How does the Fed expect to keep rates under control if even they start selling bonds?

But we think Ben Hunt of Salient Partners summarized the shift best (emphasis ours):

What has happened (and apologies for the ten dollar words) is that the Fed's reaction function has flipped 180 degrees since the Trump election. Today the Fed is looking for excuses to tighten monetary policy, not excuses to weaken. So long as the unemployment rate is on the cusp of "instability", that's the only thing that really matters to the Fed (for reasons discussed below). Every other data point, including a market sell-off or a flat yield curve or a bad CPI number - data points that used to be front and center in Fed thinking - is now in the backseat.

I'm not the only one saying this about the Fed's reaction function. Far more influential Missionaries than me, people like Jeff Gundlach and Mohamed El-Erian, are saying the same thing. If you think that this Fed still has your back, Mr. Investor, the way they had your back in 2009 and 2010 and 2011 and 2012 and 2013 and 2014 and 2015 and 2016 … well, I think you are mistaken. I think Janet Yellen broke up with you this week.The Fed is looking to tighten and, all else being equal, that is not a positive for gold prices when inflation isn't off to the races. Does that mean all is lost for gold investors and it is time to sell?

There is one BUT…

If the Fed is tightening into a weak economy that is over-leveraged with debt, then the Fed is making a big mistake. This policy error would have huge consequences as what would happen would be that higher interest rates would choke a weak real economy that only looks strong based on the stock market's rise - which would quickly reverse. That in turn would lead to defaults and bankruptcies that would snowball through the economy, like in 2007 EXCEPT that we have way more debt now.

In fact, we believe that gold SHOULD have fallen much more on the Fed statement then it did as it was only down around 1% on the week. We think there is some sizable "Fed policy error" buying in gold that is maintaining its $1250+ Price.

Our Take and What This Means for Investors

Despite our view that the Fed is making a policy mistake by raising rates and maintaining a hawkish view on inflation, we remain short-term Neutral-Bearish on gold and silver as we believe that hawkish stance is what investors will focus on.

We eventually think that will change as investors start seeing the Fed's position as a big policy mistake, but we think that gold bulls should give it a week or so for the Fed's position to be digested by markets. Thus for us it seems prudent to wait on purchasing additional gold and silver positions (SPDR Gold Trust ETF (NYSEARCA:GLD), iShares Silver Trust (NYSEARCA:SLV), Sprott Physical Silver Trust (NYSEARCA:PSLV), and ETFS Physical Swiss Gold Trust ETF, etc).

0 comments:

Publicar un comentario