King Dollar Is No More: Gold Is The New King

by: David Luo

- Weak NFP numbers out on Friday, along with revisions downward for previous months.

- The selling pressure on the dollar continues. Further bad economic pressure could turn this orderly decline into a major drop.

- GLD has almost recovered all of its losses, and will look to take out the mid-April highs.

- Fed rate hike looks to be priced in to GLD prices.

- The selling pressure on the dollar continues. Further bad economic pressure could turn this orderly decline into a major drop.

- GLD has almost recovered all of its losses, and will look to take out the mid-April highs.

- Fed rate hike looks to be priced in to GLD prices.

Introduction

First of all, I hope everyone enjoyed a happy Memorial Day Monday long weekend with family and friends.

With the shortened trading week in the US markets, we really didn't get any major news affecting gold prices, except the NFP numbers out on Friday, and the revisions that come with it. Nonetheless, GLD didn't stay flat, but continued to advance orderly through the shortened week, with a one-day gain of 0.78% on Friday to close the week out strong at 121.6.

I normally keep readers updated by posting about GLD every week or so, especially if my outlook changes on the short-term movements. Fortunately, my bullish view hasn't changed since my article two weeks ago about the divergence in the expectations for a Fed Funds rate hike and gold prices.

GLD has already advanced 1.8% since then. Unfortunately, I know some readers in the comments section mention that they look forward to my weekly updates, so I apologize for that.

The real question is, what is ahead for GLD, especially as we get closer to the hyped-up June FOMC meeting, only a week and a half away?

To answer this question, I'll be giving my perspective on macroeconomic trends in the US economy, news regarding the Fed and various Fed presidents, movements in the currency markets and bond market, technical indicators, and how they influence GLD.

The Dollar's Orderly Decline; Gold's Orderly Ascent

Probably the single biggest mover of gold is the dollar, which moves inversely to gold due to the dollar's status as the current reserve currency and safe-haven competitor to gold. They also compete through opportunity cost, with the dollar offering interest and gold offering a hedge against inflation, which weakens the dollar.

This week marks more weakness for the dollar and more strength for GLD. Since the beginning of the year, the dollar index has fallen more than 6% from 103 to less than 97.

Uncertainty about the US direction under Trump continues to linger. The fundamentals for the US don't look very solid. There are the stories of involvements with Russia, geopolitical tensions seem to weigh on the dollar with every news article, and just this week, we got news that Trump pulled out of the Paris climate accord. All of these factors have contributed to the dollar's decline.

The major factor, however, has been Trump's weak dollar policy. From talking with reporters about how he thinks the dollar is too strong, to having his top trade advisor accusing Germany of manipulation of the euro, to threatening to label China a currency manipulator, to accusing the Japanese of devaluing the yen vs. the dollar, Trump has been active in talking down the dollar.

Of course, the idea here is that Trump thinks that our exports will be more competitive if we have a weaker dollar, that foreign buyers will import more US products and we will reduce our trade deficit.

Unfortunately, that probably won't happen and our trade deficits will balloon out of control, instead.

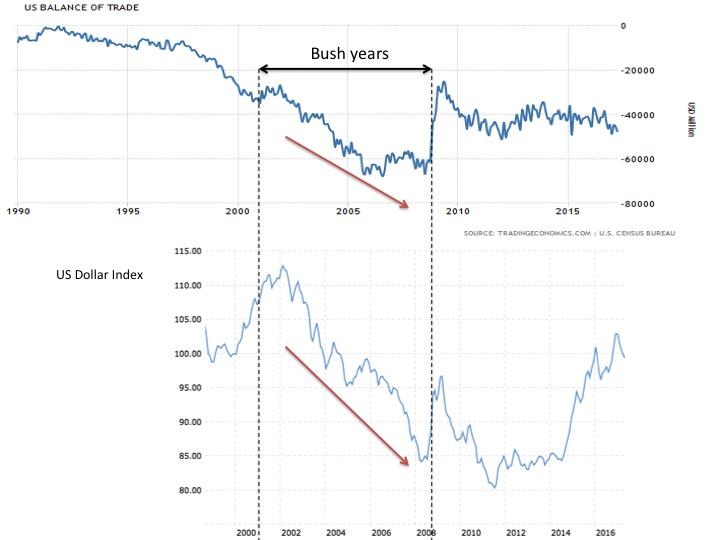

Just look at the events that transpired when George Bush took office from Bill Clinton. The dollar was at record highs around 110, and then for the next eight years while he was in office, it collapsed.

(Source: Trading Economics, Macrotrends)

Meanwhile, our trade deficits exploded. The reason for this is because the US is mostly a service economy, and relies heavily on imports from foreign nations. As the dollar weakens, Americans still depend on these manufactured goods across seas, and they end up paying more for those products because their currency is weaker.

This phenomenon will likely repeat itself under President Trump and doesn't bode well for the US economy or the dollar. Another dollar decline under Trump like we had under George Bush would spell massive gains for GLD.

Under the Bush years, spot gold increased from around $250/oz to $800/oz for a 220% gain, while GLD increased more than 70% from under 55 to 86 from its inception until Bush left office. Since the GLD ETF began in 2006, GLD investors weren't able to capture the huge moves in gold during Bush years, but we will be able to take the full percentage of the moves as the dollar weakens under Trump.

As for this week, GLD continued to strengthen on the back of a weak dollar. The trend looks strong here and I think it will likely continue next week.

Nonfarm Payrolls Disappoint

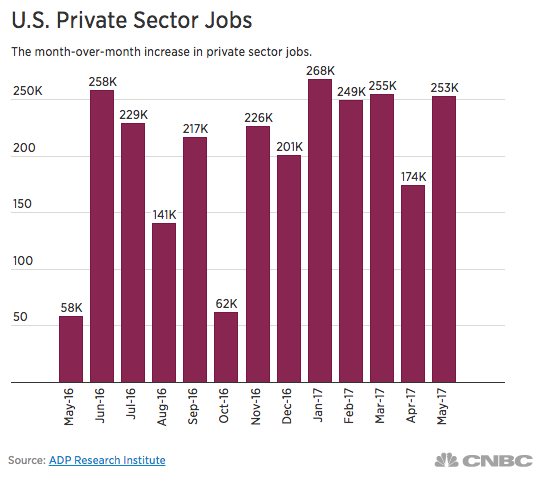

So much for all the hope and optimism for great NFP numbers. As has been the recent trend, the ADP numbers give the markets false hope of a great NFP report, only to have it disappoint.

(Source: CNBC)

The consensus for May NFP was 185k, but we got 138k jobs added instead. Look for this number to come down as we get more revisions in the months ahead. We also got heavy revisions downwards from prior months. The huge April jobs number of 211k was revised down to 174k, and the weak March number, which came out at 98k, was revised to 73k and has been revised even lower now at 50k.

Disappointing NFP tends to propel GLD higher. The narrative here is that weaker NFP means a weaker economy, less rate hikes by the Fed, a weaker dollar from low interest rates and stronger GLD.

The underlying fundamentals for the US labor market don't look good either.

Job creation skewed toward lower-wage professions. Full-time jobs tumbled 367,000 for the month, while part-time positions rose by 133,000.

The unemployment rate decline was due primarily to a fall in the labor force participation rate, which declined two-tenths to 62.7 percent and remained mired around its lowest levels since the late 1970s. The rate, though, is at its lowest level since May 2001.

If we are adding part-time jobs at the expense of full-time jobs, that is not a plus for the economy.

The fall in unemployment, while it looks good on the headline, was due to lack of participation.

As more people become discouraged in finding work and discover that Trump's promise to bring back jobs hasn't materialized, they are once again leaving the labor market.

This explanation also accounts for why we haven't been seeing wage growth. Part-time jobs, low-paying jobs, do not contribute to wage growth. Discouraged workers do not contribute to wage growth. It's no surprise that confidence numbers have also been falling from their highs during the Trump trade.

Federal Reserve & Interest Rates

On the back of the weak jobs number, the Fed Funds futures have lowered their expectations for three rate hikes this year, despite the narrative from Janet Yellen that she thinks that bad Q1 numbers are "transitory."

According to the CME Group's FedWatch Tool, the market thinks there's a 94.6% chance of an interest rate hike in the June meeting, despite all of the poor economic data. I do believe we will be getting a hike in June, and there won't be a surprise because Fed officials are still talking about three interest rate hikes this year. Just a few days ago, the Dallas Fed President Kaplan said that he's sticking to his guns and is calling for two more hikes this year.

I mean, I don't believe him, but what it does say to me is that the Fed is hawkish enough to basically tell the markets that there will be a hike in June. This information has now been baked into the price of GLD. It is just that expectations for future rate hikes, such as one during the September or December meetings have dropped. Higher interest rates may act as a resistance in GLD, but lower interest rates, even in the future, mean a weaker dollar today and stronger GLD.

10-Year Treasury Rate data by YCharts

The 10-year yield also fell as expectations of future interest rate hikes fell. The Fed has been talking about unwinding its balance sheet. If it does go through with this, yields will rise as they taper off their rollovers. However, with the current planned cap, such small rollovers will not have a major effect on interest rates, especially if inflation picks up. I don't see GLD prices being heavily influenced by this "tapering" of the balance sheet.

Technical Analysis

Based on the technicals for GLD, there is more steam in this rally. Since the beginning of the year, we've been seeing higher highs, as indicated by the blue circles, and higher lows, in the black circles.

This is the classic indication of a bull market. I think we're going to be breaking $1300/oz this time around, and take out the last high back in mid-April of around $1290.

The RSI, while climbing past 60, has yet to cross the 70 level, and can sustain there for some time, especially if GLD moves favorably after the June rate hike. The parabolic SAR hasn't turned to show any indication of a time to sell. The technicals seem to show more upside ahead in GLD prices.

Conclusión

This time around, we have not seen a decline in GLD prices as Fed Funds futures have increased.

There is less certainty about how GLD will move post-FOMC meeting as it is no longer a buy the rumor sell the fact trade that I've written about frequently before.

What I am confident in is a dollar that continues to weaken and fundamentals in the US that continue that trend as well. There may be short-term fluctuations before and after the Fed meeting, but I think GLD will be going higher. As we get closer to the FOMC meeting, there may be more clarity on how GLD will perform afterward.

0 comments:

Publicar un comentario