Five markets charts that matter for investors

The euro, S&P 500, mutual fund managers, central banks and frontier markets in focus

by: FT Reporters

Here is a selection of five charts that FT Markets believes are worth watching.

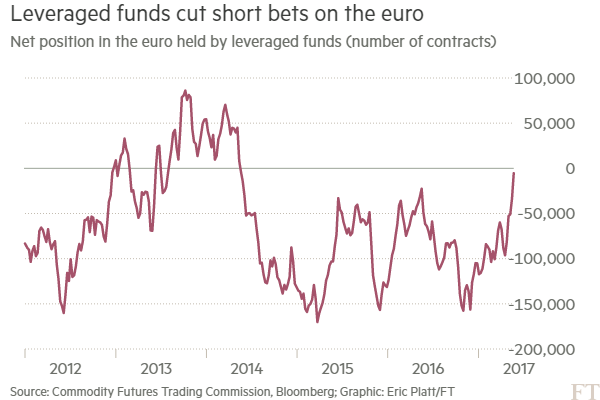

1. A bullish propellant for the euro

Hedge funds have cut their bearish bets on the euro to the lowest level in three years, with the common currency on track for its second straight month of 2 per cent plus returns against the dollar. Investors are now questioning if that will provide additional ballast to the euro.

The shift in sentiment by leveraged funds, a proxy for hedge funds, follows Emmanuel Macron’s sweeping victory in the French presidential election as well as quickening economic activity across the continent. Large net short bets have been reduced, and shorts now outnumber long positions by 5,342 contracts, according to the latest data from the Commodity Futures Trading Commission. That figure eclipsed 155,000 in November.

Despite the swing in futures positioning, investors and strategists are already drumming up a list of potential weights on the euro. That includes the next populist test in the continent, after former Italian prime minister Matteo Renzi signalled he favoured an early election this year.

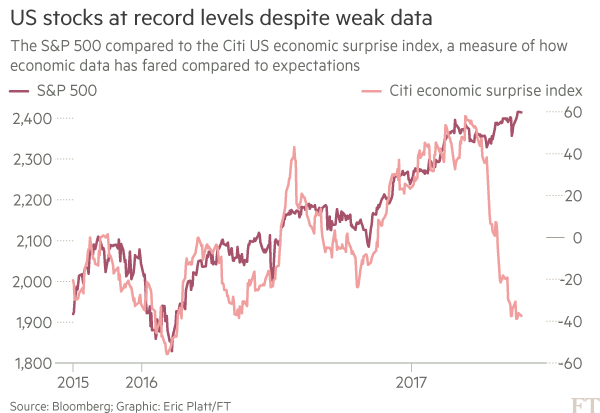

2. S&P 500 v Citi economic surprise index

Confounded by the string of record highs by the S&P 500 despite lacklustre economic data over the past several months in the US? You’re not alone.

Peter Tchir, an analyst at Brean Capital, argues it is a phenomenon that “deserves some attention”. Economic data have broadly fallen short of forecasts over the past month, according to a closely followed barometer produced by Citi. What’s more, investors have dialled back their optimism that economic policies championed by the Trump administration will become law this year.

Nonetheless, the S&P 500 has set 20 closing highs this year. Investors point to faster than expected earnings growth in the first quarter. The advance has been fuelled by the ascent of some of the index’s largest members, many of which are in the technology sector. Portfolio managers have looked to the industry with the expectation that it will be able to deliver growth even if broader economic output decelerates.

More defensive parts of the market have also outperformed the S&P 500 since March 15, with utilities, consumer staples and real estate companies all advancing.

3. Mutual fund managers finally have something to brag about

Mutual fund managers facing mounting competition from passive investment products amid years of underperformance finally have something to brag about.

Goldman Sachs research shows that 52 per cent of funds that focus on large-cap stocks have beaten their benchmarks since the start of 2017. If the trend held steady, it would mark the first time the hit rate has exceeded 50 per cent since 2009.

The brightening performance, which would represent a sharp uptick from the grim 19 per cent hit rate notched up last year, has come as managers have placed bets on the technology, consumer discretionary and healthcare sectors. The trio represent the top-performing S&P 500 sectors this year, with price returns of 20.1 per cent, 11.5 per cent, and 9.7 per cent, respectively.

Growth funds have posted particularly strong gains, with the average fund up 12.5 per cent year-to-date, compared with a 2.4 per cent advance for value funds.

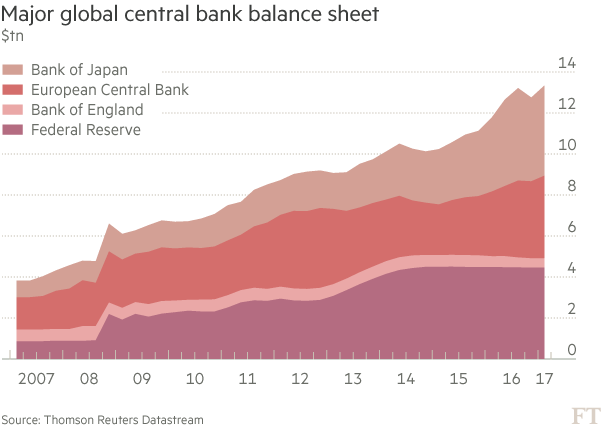

4. Central banks keep expanding their balance sheets

Investors are becoming a lot more focused on the prospects for tighter policy by global central banks.

The Federal Reserve is expected to nudge borrowing costs higher next month and is looking at winding down its $4tn balance sheet this year. The European Central Bank has begun a taper of its purchases with monthly bond buying dropping by one-quarter to €60bn.

Still, as this chart shows, the overall size of central bank support for asset prices remains hefty and helps explain the resilience of equities. Jack Ablin, at BMO Capital Markets notes: ‘’Valuations are stretched but equity markets continue to enjoy a continuous flood of liquidity from the world’s central banks and sidelined investors. Central banks purchased $1.8tn over the past 12 months. The Fed is reinvesting more than $30bn each month even though they stopped growing their balance sheet in 2014.’’

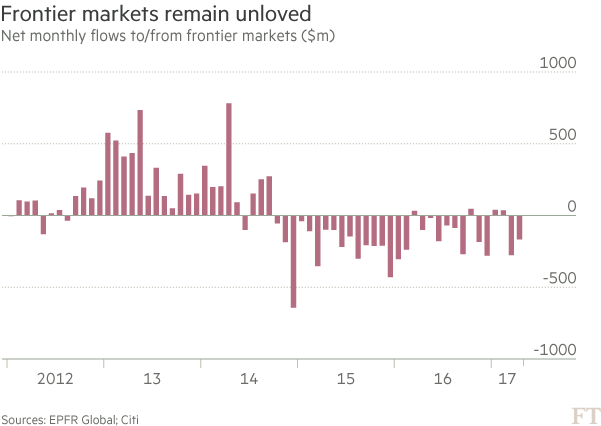

5. Frontier markets are still unloved

Plenty of money has pursued emerging markets this year, not so the outer realm of the investing universe. Flows into frontier markets — countries whose markets are considered too small or illiquid to be included in MSCI’s flagship EM Index, such as Argentina, Kuwait, Pakistan, Vietnam, Morocco and Nigeria — remain negative. Much may depend on perceptions of Africa, a large slice of the frontier world, particularly with Pakistan being promoted to emerging market status by MSCI in June and expectations that Argentina could follow suit in 2018.

0 comments:

Publicar un comentario