Cost of ‘Black Swan’ bet on falling markets hits pre-crisis low

Hedge funds could make 25 times their money if S&P 500 falls 7 per cent in a month

by: Miles Johnson in London

The cost for hedge funds of taking out “Black Swan” insurance against a sharp fall for US equities has fallen to the lowest level since before the financial crisis as stock markets continue to touch all-time highs.

Months of low market volatility has forced down the price of options allowing hedge funds to place bets that would make them 25 times on their money if the S&P 500 index fell by 7 per cent over the next month.

“The price of constructing hedges against a fall in equity markets are at their lowest levels ever, while equity markets are trading at all-time highs,” said Deepak Gulati, chief investment officer of Argentiere Capital and former head of equity proprietary trading at JPMorgan Chase.

“Historically low levels of volatility in options markets are providing the opportunity to construct long volatility positions with completely asymmetric pay-offs.”

At a time when equity markets continue to grind higher and most investors are betting that volatility will remain low, the potential for big payouts worth many multiples of their cost is tempting a small number of hedge funds to take the other side of that trade.

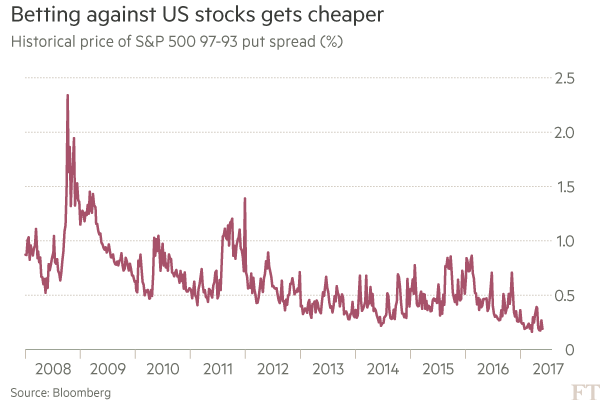

Options using the so-called one month 97-93 per cent put spread on the S&P 500, which requires the index to fall by between 3 and 7 per cent in a month to be profitable, currently allows a maximum profit of $4 for contracts that cost $0.16, or a 25 times return, according to Bloomberg data.

Expectations of market volatility, which make up an important input into how much options bets cost, have been plumbing new lows this year. Earlier this month, the Vix index, which tracks the implied volatility of the S&P 500 over the next 30 days, closed at the lowest level since 1993.

Last month the Financial Times reported that Ruffer, a $20bn London investment company, had been buying up large amounts of contracts linked to the Vix index priced at half a dollar as part of a hedging strategy for its portfolio, earning it the moniker “50 Cent” among bemused traders.

At the same time, low expected volatility also allows traders to make cheap bets using options on the US stock market also rising in value.

The so-called 3 month 105-110 per cent call spread on the S&P 500, which needs the index to rise by 5 to 10 per cent over three months to be profitable, would generate a profit of up to 38.5 times. This compares to an average pay-off ratio for an identical call spread of 5.6 times over the past decade.

Months of low market volatility has forced down the price of options allowing hedge funds to place bets that would make them 25 times on their money if the S&P 500 index fell by 7 per cent over the next month.

“The price of constructing hedges against a fall in equity markets are at their lowest levels ever, while equity markets are trading at all-time highs,” said Deepak Gulati, chief investment officer of Argentiere Capital and former head of equity proprietary trading at JPMorgan Chase.

“Historically low levels of volatility in options markets are providing the opportunity to construct long volatility positions with completely asymmetric pay-offs.”

At a time when equity markets continue to grind higher and most investors are betting that volatility will remain low, the potential for big payouts worth many multiples of their cost is tempting a small number of hedge funds to take the other side of that trade.

Options using the so-called one month 97-93 per cent put spread on the S&P 500, which requires the index to fall by between 3 and 7 per cent in a month to be profitable, currently allows a maximum profit of $4 for contracts that cost $0.16, or a 25 times return, according to Bloomberg data.

Expectations of market volatility, which make up an important input into how much options bets cost, have been plumbing new lows this year. Earlier this month, the Vix index, which tracks the implied volatility of the S&P 500 over the next 30 days, closed at the lowest level since 1993.

Last month the Financial Times reported that Ruffer, a $20bn London investment company, had been buying up large amounts of contracts linked to the Vix index priced at half a dollar as part of a hedging strategy for its portfolio, earning it the moniker “50 Cent” among bemused traders.

At the same time, low expected volatility also allows traders to make cheap bets using options on the US stock market also rising in value.

The so-called 3 month 105-110 per cent call spread on the S&P 500, which needs the index to rise by 5 to 10 per cent over three months to be profitable, would generate a profit of up to 38.5 times. This compares to an average pay-off ratio for an identical call spread of 5.6 times over the past decade.

0 comments:

Publicar un comentario