Why the Federal Reserve should leave interest rates unchanged

The central bank should respond to lower inflation by keeping policy loose

NO STATEMENT from the Federal Reserve is complete without a promise to make decisions based on the data. In each of the past two years, a souring outlook for the world economy prompted the Fed to delay interest-rate rises. And quite right, too. Yet if the Fed raises rates on June 14th in the face of low inflation, as it has strongly hinted, it would bring into question its commitment both to the data and also to its 2% inflation target.

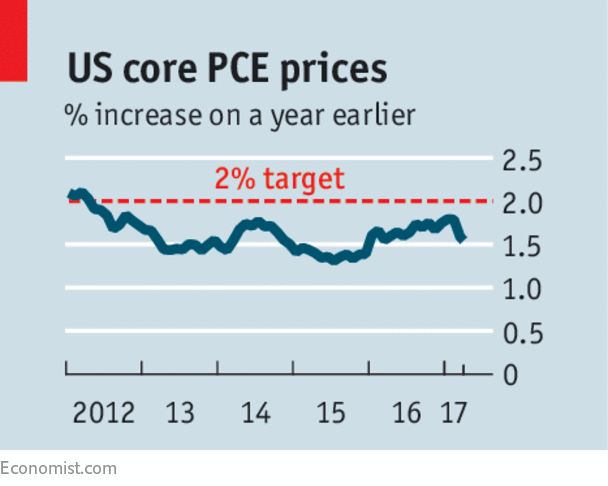

The central bank has raised rates three times since December 2015 (the latest rise came in March). It is good that monetary policy is a little tighter than it was back then. The unemployment rate, at 4.3%, is lower than at any time since early 2001. A broad range of earnings data show a modest pickup in wage growth. The Fed is right to think that it is better to slow the economy gradually than be forced to bring it to a screeching halt later, if wage and price rises get out of hand. The rate increases to date have been reasonable insurance against an inflationary surge. But no such surge has yet struck. Unexpectedly low inflation in both March and April has left consumer prices no higher than they were in January. According to the Fed’s preferred index, core inflation—that is, excluding volatile food and energy prices—has fallen to 1.5%, down from 1.8% earlier this year. It is now well below the 2% target.

Nor does a surge seem imminent. For a while, Donald Trump’s promises to cut taxes and spend freely on infrastructure made higher rates appear all the wiser. But fiscal stimulus looks less likely by the week. Tax cuts are stuck in the legislative queue behind health-care reform, and Mr Trump’s administration has tied itself in knots over whether it will increase the deficit.

Meanwhile, the current “infrastructure week” in Washington may generate more headlines than proper plans.

Even so, the Fed is expected to go ahead and raise rates this month. The markets think there is a 90% probability of an increase of 25 basis points (hundredths of a percentage point).

It is possible that more inflation is coming. An economy that is stimulated will eventually overheat.

The central bank may believe that low unemployment is about to cause inflation. But the truth is that nobody is sure how far unemployment can fall before prices and wages soar. Not many years ago some rate-setters put this “natural” rate of unemployment at over 6%; the median rate-setter’s estimate is now 4.7%.

Advertisement: Replay Ad

Advertisement

3

The only way to find the labour market’s limits is to feel them out. Falling inflation and middling wage growth both suggest that these limits are some way off, for two possible reasons.

First, higher wage growth could yet tempt more of the jobless to seek work (those who are not actively job-hunting do not count as unemployed). The proportion of 25- to 54-year-olds in employment is lower than before the recession, by an amount representing almost 2.4m people.

By this measure, which fell in May, joblessness is worse in America than in France, where the overall unemployment rate stands at 9.5%. Second, even the moderate pickup in wage growth to date might encourage firms to invest more, lifting productivity out of the doldrums and dampening inflationary pressure.

I like hike

Jobs growth in America has already slowed from a monthly average of 187,000 in 2016 to 121,000 in the past three months. That is enough to reduce slack in the economy, but only just.

Slowing it still further is needless so long as inflation remains quiescent. It makes still less sense when you consider the asymmetry of risks before the Fed. If tighter money tips the economy into recession, the central bank has only a little bit of room to cut rates before it hits zero. But if inflation rises, it can raise them as much as it likes.

This asymmetry of risks extends to the Fed’s credibility. Inflation has been below 2% for 59 of the 63 months since the target was announced in January 2012. Continuing to undershoot the goal would cast more doubt on the central bank’s commitment to it than modest overshoots would.

For too long, hawks have made excuses for the persistence of low inflation. The latest is to blame new contracts offering unlimited amounts of mobile data, as if cheaper telecommunications somehow should not count. The Fed should keep its promise to base its decisions on the data, and leave interest rates exactly where they are.

0 comments:

Publicar un comentario