'That's The Most Horrible Thing I've Ever Heard'

by: The Heisenberg

- One day, someone is going to look back at the proliferation of ETFs and wonder how everyone could have been so naive.

- Outside of some geopolitical catastrophe, ETFs almost unquestionably represent the biggest risk to markets - and this risk is at the structural level.

- Think about this: if you own ETFs, you are a derivatives trader. Have you considered that?

- Outside of some geopolitical catastrophe, ETFs almost unquestionably represent the biggest risk to markets - and this risk is at the structural level.

- Think about this: if you own ETFs, you are a derivatives trader. Have you considered that?

So, this is kind of strange.

By far, the most read post over at the Heisenberg Report, in a week dominated by geopolitical headlines, was a piece about ETFs.

Personally, I think that's great. Because it suggests people are at least cognizant of the fact that no matter what you think about the proliferation of passive, low-cost investment vehicles, their rise to prominence (actually "dominance" is better) is important and something that needs careful consideration.

To be sure, the ETF discussion is a rabbit hole. And one thing I've learned writing on this platform over the past year is that readers here don't like to be led down rabbit holes, especially deep ones, because if comment totals are any indication, readers tend to get about halfway down those deep rabbit holes before they simply turn around and climb back out (i.e. they click out of the article and don't bother commenting).

So, in the interest of respecting readers' apparent disdain for lengthy, in-depth diatribes, I'm going to try and keep this concise, simple, and visually pleasing.

As the Heisenberg crowd is well aware, I'm worried about ETFs. That goes for popular equity vehicles (NYSEARCA:SPY) all the way down to high-yield (NYSEARCA:HYG) products.

Here's how I put it earlier this week:

I have very serious reservations about the rampant proliferation of ETFs.

In some instances (HY products) I can put my finger on exactly why (no liquidity for the underlying assets, a quarter of the float being used by institutions for daily liquidity needs, etc.), and in some instances (equity ETFs) I can't quite get there.

But what I do know is that if you step back from the unit creation/destruction process (which generally seems to be functioning well) and just abstract yourself a bit, this just seems like a bad idea.

After all, ETFs are kind of, sort of derivatives. Now there's a vociferous debate about that and I'm really - really - inclined to say it's just semantics. Because at the end of the day, you're buying something that represents something else even if it is, in a way, also a manifestation of that thing it represents.

That last bit is a problem. And no one wants to admit it. But the simple fact of the matter is that ETFs have turned retail investors into derivatives traders. You can call them whatever you want in order to make yourself feel better, but if you've got a portfolio full of ETFs, what you have is a portfolio full of derivatives.

But it's certainly not just retail. Consider this out earlier this week from Deutsche Bank:

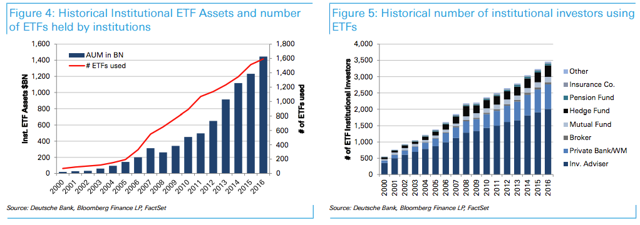

Institutional ETF assets grew by $213 bn and reached $1.44 trillion in 2016 As of the end of 2016, almost 3,500 institutional investors held more than $1.44 trillion in ETF assets accounting for about 59% of all ETF assets. As per historical growth trends, ETF assets held by institutions and the number of products used by them have both grown more than 7 and 8 times in the last 10 years, respectively. Similarly, the number of different institutional investors using ETFs has almost doubled during the same period.

Now again, you can read that as is and take comfort in it (which is pretty clearly what Deutsche intended), or you can translate it and strip it down to what it actually says, which is this:

Now again, you can read that as is and take comfort in it (which is pretty clearly what Deutsche intended), or you can translate it and strip it down to what it actually says, which is this:Institutions use of derivatives that have never really been battle-tested has exploded by a factor 8 since the crisis.

Right. So, that's obviously bad. But it gets worse. Here's another passage from the same Deutsche Bank note:

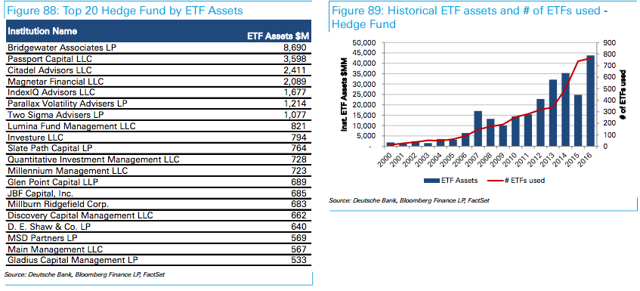

Hedge funds are traders that seek to implement directional or relative value views around market inefficiencies and events (e.g. macroeconomic, geopolitical, or company specific). They usually seek absolute returns, take long and short positions, and may deal in less liquid securities, or in large concentrated sizes. Recent ETF ownership data suggest that more and more hedge funds are finding value in using ETFs. In fact, our data suggest that hedge funds use ETFs for gaining quick and efficient asset class access both on the long and short side, similar to futures contracts.

In the interest of keeping my promise re: conciseness, I'm not going to expound on all of the things that could go wrong there. Rather, I'll ask you again to think about that last bolded passage from a common sense perspective. That is, just read it again and tell me if that sounds like a good idea.

In the interest of keeping my promise re: conciseness, I'm not going to expound on all of the things that could go wrong there. Rather, I'll ask you again to think about that last bolded passage from a common sense perspective. That is, just read it again and tell me if that sounds like a good idea.

Here's what you should think after reading it:

See this always - always - comes back to the same inescapable problem, which is this: I don't care what kind of ETF it is, it cannot be more liquid than the assets it represents.

It can seem to be more liquid, but that's what we might call "phantom liquidity." And it will dry up when things get messy which, you'll recall, is exactly what happened on the morning of August 24, 2015.

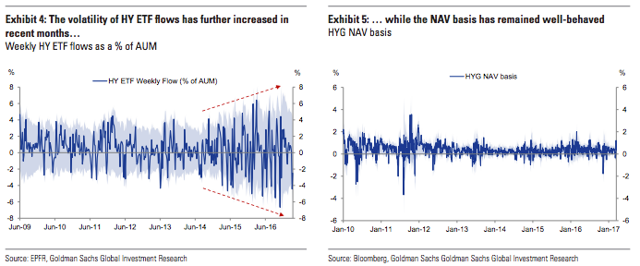

As I've noted before, there are a whole lot of people out there who are hell-bent on pointing to heavy volume as "evidence" of liquidity. Witness Goldman out on Wednesday (this is in reference to high-yield ETFs):

The fear is that the combined effect of the "liquidity mismatch" inherent to ETFs and a potential abrupt reversal of the inflows of the past several years could prove damaging to the secondary market. The past few years have seen HY ETF flows turn increasingly volatile (Exhibit 4). By contrast and taking the HYG ETF as an example, the NAV basis - the difference between the ETF's price and the net asset value of the underlying bond portfolio - has been moving within a tighter range vs. the period from 2010 to 2013 (see Exhibit 5).

We view the relatively low volatility of the NAV basis in the face of increasingly volatile flows as evidence of continued efficiency gains in the mechanics of ETFs.

Higher velocity, a byproduct of more aggressive liquidity provision and improving technology, shortens mispricing periods and thus pushes the volatility of the NAV basis lower.

Read that last bolded bit again.

That is completely and totally absurd. The argument there is that more trading in the ETF (velocity) is leading to a less volatile NAV basis (the difference between the ETF price and the value of the underlying bonds), and, therefore, we have more liquidity.

But that's not true. We just have more trading in the ETF shares. That says absolutely nothing about liquidity for the underlying assets. Indeed, it makes things worse! Because the more you trade the ETF rather than the underlying bonds, the more illiquid those underlying bonds invariably become.

I am 100% sure that the vast majority of market participants (big and small) have no idea how dangerous this is. Which is really, really strange considering what transpired on August 24 two years ago.

If ever there were a "systemic" risk, surely this is it.

Yours truly on a beach weather Friday,

0 comments:

Publicar un comentario