A decade after the crisis, how are the world’s banks doing?

Though the effects of the financial crisis in 2007-08 are still reverberating, banks are learning to live with their new environment, writes Patrick Lane. But are they really safer now?

THE ELECTION OF Donald Trump as America’s 45th president dismayed most of New York; Mr Trump’s home city had voted overwhelmingly for another local candidate, Hillary Clinton.

But Wall Street cheered. Between polling day on November 8th and March 1st, the S&P 500 sub-index of American banks’ share prices soared by 34%; finance was the fastest-rising sector in a fast-rising market. At the time of the election just two of the six biggest banks, JPMorgan Chase and Wells Fargo, could boast market capitalisations that exceeded the net book value of their assets. Now all but Bank of America and Citigroup are in that happy position.

Banks’ shares were already on the up, largely because markets expected the Federal Reserve to raise interest rates after a long pause. It obliged in December and March, with three more rises expected this year. That should enable banks to widen the margin between their borrowing and lending rates from 60-year lows. Mr Trump’s victory added an extra boost by promising to lift America’s economic growth rate. He wants to cut taxes on companies, which would fatten banks’ profits directly as well as benefiting their customers. He has also pledged to loosen bank regulation, the industry’s biggest gripe, declaring on the campaign trail that he would “do a big number” on the Dodd-Frank Wall Street Reform and Consumer Protection Act, which overhauled financial regulation after the crisis.

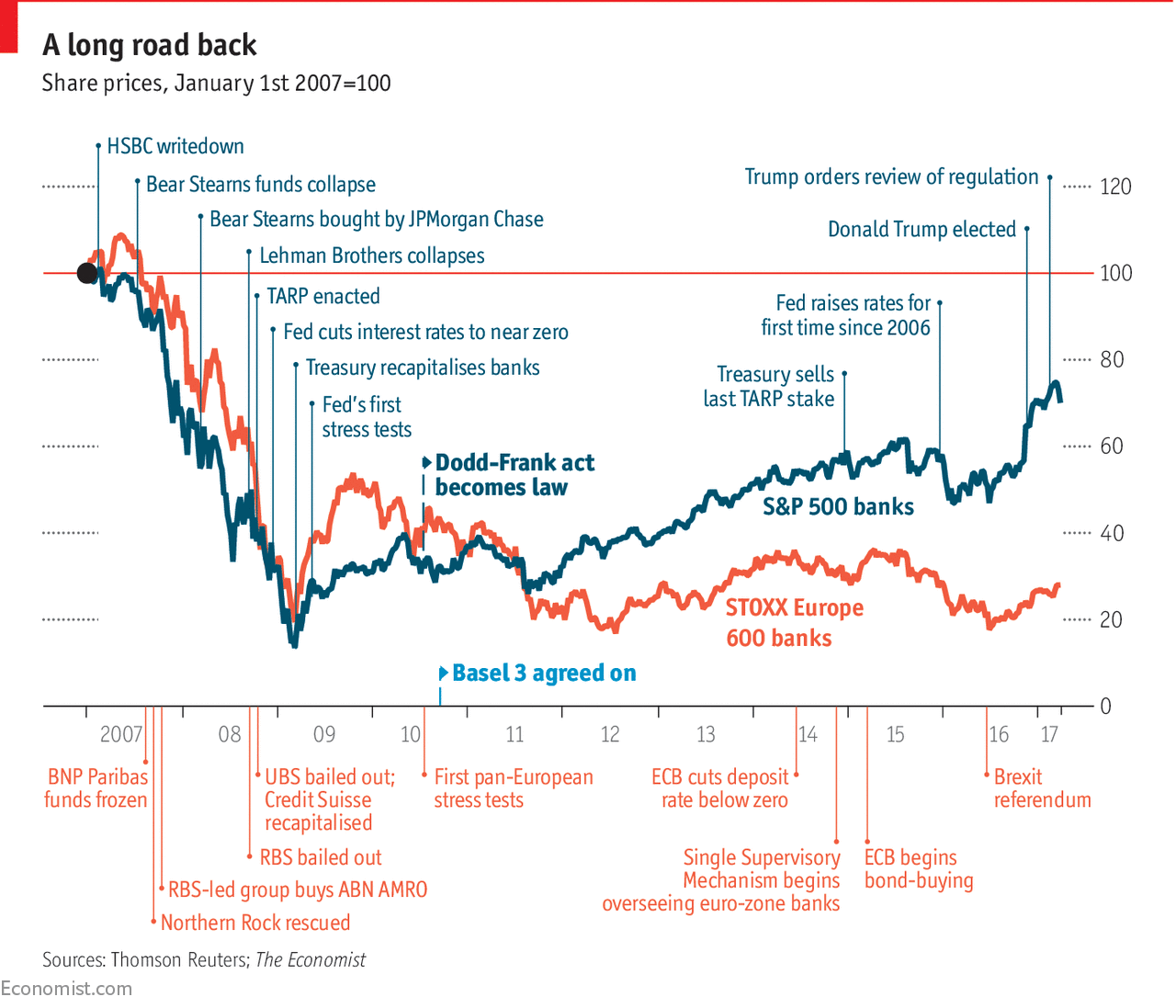

So have the banks at last put the crisis behind them? This special report will argue that many of them are in much better shape than they were a decade ago, but the gains are not evenly spread and have further to go. That is particularly true in Europe, where the banks’ recovery has been distinctly patchy. The STOXX Europe 600 index of bank share prices is still down by two-thirds from the peak it reached ten years ago this month. European lenders’ returns on equity average just 5.8%.

America’s banks are significantly stronger. In investment banking, they are beating European rivals hollow. They are no longer having to fork out billions in legal bills for the sins of the past, and they are at last making a better return for their shareholders. Mike Mayo, an independent bank analyst, expects their return on tangible equity soon to exceed their cost of capital (which he, like most banks, puts at 10%) for the first time since the crisis.

But financial crises cast long shadows, and even in America banks are not back in full sun yet.

Despite the initial Trump rally, the S&P 500 banks index is still about 30% below the peak it reached in February 2007 (see chart). Debates about revising America’s post-crisis regulation are only just beginning. And the biggest question of all has not gone away: are banks—and taxpayers—now safe enough?

Plenty of Americans, including many who voted for Mr Trump, are still suspicious of big banks. The crisis left a good number of them (though few bankers) conspicuously poorer, and resentment easily bubbles up again. Last September Wells Fargo, which had breezed through the crisis, admitted that over the past five years it opened more than 2m ghost deposit and credit-card accounts for customers who had not asked for them. The gain to Wells was tiny, and the fine of $185m was relatively modest. But the scandal cost John Stumpf, the chief executive, and some senior staff their jobs, as well as $180m in forfeited pay and shares. Wells has been fighting a public-relations battle ever since, and mostly losing.

This report will take stock of the banking industry, chiefly in America and Europe, a decade after the precipitous fall from grace of banks on both sides of the Atlantic. The origins of the crisis lay in global macroeconomic imbalances as well as in failures of the financial system’s management and supervision: a surfeit of savings in China and other surplus economies was financing an American borrowing and property binge. American and European banks, economies and taxpayers bore the brunt.

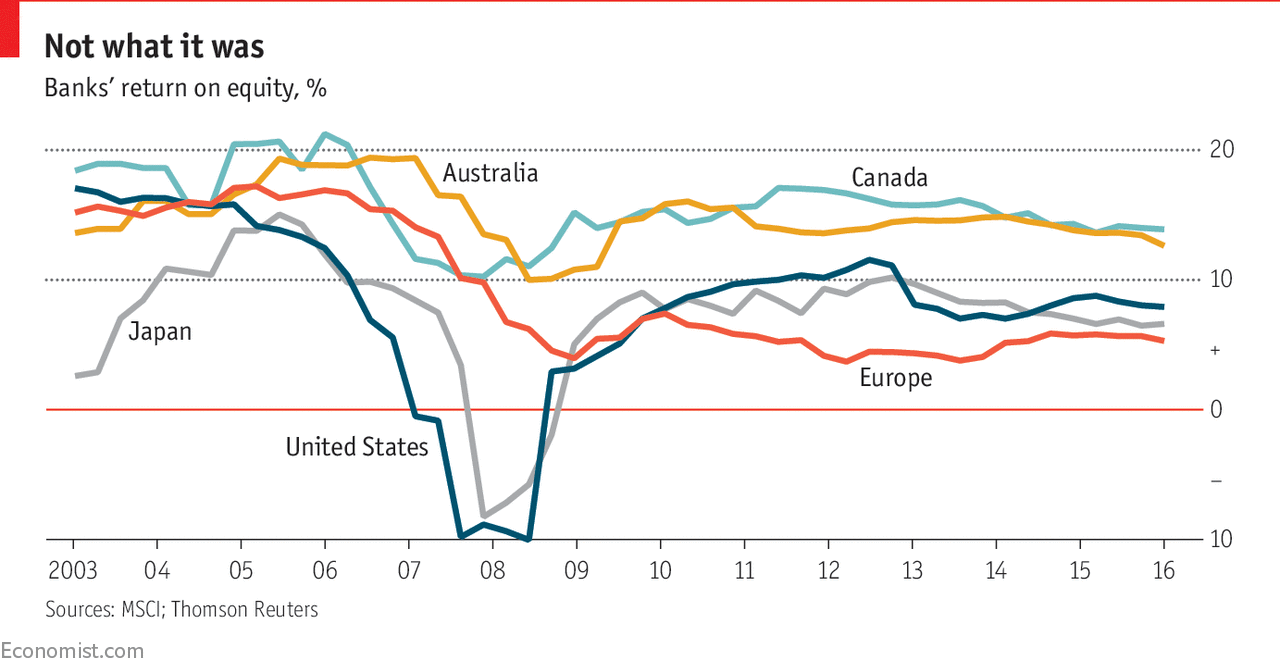

Banks in other parts of the world, by and large, fared far better. In Australia and Canada, returns on equity stayed in double figures throughout. It helped that Australia has just four big banks and Canada five, which all but rules out domestic takeovers and keeps margins high. As commodity prices have sagged recently, so has profitability in both countries, but last year Australia’s lenders returned 13.7% on equity and Canada’s 14.1%, results that banks elsewhere can only envy.

Japan’s biggest banks, which had been reckless adventurers in the heady 1980s and 1990s, did not remain wholly unscathed. Mizuho suffered most, writing down about ¥700bn ($6.8bn). The Japanese were able to pick through Western debris for acquisitions to supplement meagre returns at home. Some chose more wisely than others: MUFG’s stake in Morgan Stanley was a bargain, whereas Nomura’s purchase of Lehman Brothers’ European business proved a burden. Chinese lenders were mostly bystanders at the time, remaining focused on their domestic market.

Advertisement:Replay Ad

Advertisement

3

The seven consequences of apocalypse

Ask bankers what has changed most in their industry in the past decade, and top of their list will be regulation. A light touch has been replaced by close oversight, including “stress tests” of banks’ ability to withstand crises, which some see as the biggest change in the banking landscape. Before the crisis, says the chief financial officer of an international bank, his firm (and others like it) carried out internal stress tests, for which it collected a few thousand data points. When his bank’s main supervisor started conducting tests after the crisis, the number of data points leapt to the hundreds of thousands. It is now in the low millions, and still rising. The number of people working directly on “controls” at JPMorgan Chase, America’s biggest bank, jumped from 24,000 in 2011 (the year after the Dodd-Frank act, the biggest reform to financial regulation since the 1930s) to 43,000 in 2015.

That works out at one employee in six.

The second big change is far more demanding capital requirements, together with new rules for leverage and liquidity. Bankers and supervisors agree that the crisis exposed banks’ equity cushions as dangerously thin. For too many, leverage was the path first to profit and then to ruin. Revised international rules, known as Basel 3 (still a work in progress), have forced banks to bulk up, adding equity and convertible debt to their balance-sheets. The idea is that a big bank should be able to absorb the worst conceivable blow without taking down other institutions or needing to be rescued.

Between 2011 and mid-2016 the world’s 30 “globally systemically important” banks boosted their common equity by around €1trn ($1.3trn), mostly through retained earnings, says the Bank for International Settlements in Basel.

Third, returns on equity have been lower than before the crisis. In part, that is a natural consequence of a bigger equity base. But the fallout from the crisis has also squeezed returns in another way.

Central banks first pushed interest rates to ultra-low levels and then followed up with enormous purchases of government bonds and other assets. This was partly intended to help banks, by making funding cheaper and boosting economies. But low rates and flat yield curves compress interest margins and hence profits.

Balance-sheets have been stuffed with cash, deposited at central banks and earning next to nothing.

According to Oliver Wyman, a consulting firm, the share of cash in American banks’ balance-sheets jumped from 3% before the crisis to a peak of 20% in 2014. As the world economy is at last reviving after several false starts, earnings may pick up in Europe as well as in America.

Sweat your assets

Fourth, sluggish revenues, combined with the competing demands of supervisors and shareholders, have forced banks to screw down their costs and to think much harder about how best to use scarce resources. “If I’m going to get a good return on a high amount of capital, I’d better focus on what I’m good at,” says Jim Cowles, Citigroup’s boss in Europe, the Middle East and Africa. Citi, which under Sandy Weill in the late 1990s had become a sprawling financial supermarket, selling everything from investment-banking services to insurance, has retreated to become chiefly a corporate and investment bank, much as it had been in the 1970s and 1980s. Its bosses emphasise its “network”, a presence in nearly 100 countries that multinationals’ treasurers can count on. It once also had retail banks in 50 countries, many of them second-string. That total is now down to 19.

Such retreat from marginal businesses has also meant fewer jobs and lower bonuses, even if bankers’ pay is still the envy of most. That has brought about a fifth change: banks have become less attractive employers for high-powered graduates. “The brightest people no longer want to go to banks but to Citadel [a hedge-fund firm],” laments a senior banker. Some millennials, he adds, are drawn to technology companies instead. Others “don’t want to deal with business at all”. That is because of a sixth change: the financial sector’s reputation was trashed by the crisis. One scandal followed another as the story of the go-go years unfolded: providing mortgages to people who could not afford them; mis-selling securities built upon such loans; selling expensive and often useless payment-protection insurance; fixing Libor, a key interest rate; rigging the foreign-exchange market; and much more.

Seventh and last, financial technology is becoming ever more important. That may be better news for banks than it sounds, despite the creakiness of some of their computer systems. Plenty of financial startups are trying to muscle in on their business, but in a highly regulated industry heavyweight incumbents are harder to usurp than booksellers or taxi drivers. As a result, there is a good chance of banks and technology companies forming mutually beneficial partnerships to improve services to their customers rather than fighting each other.

0 comments:

Publicar un comentario