Private equity bets big on software

A new wave of funds thinks it can win with aggressive investments in tech businesses

by: Tom Braithwaite

For someone who prefers a low profile, Robert Smith has a knack for attracting attention.

Mr Smith, who rarely gives interviews, held his wedding in 2015 at an inaccessible Italian villa, in theory far from the gazing eye. But given that his bride Hope Dworaczyk was a former Playboy Playmate of the Year and the entertainment was provided by John Legend and Seal, photos of the ceremony made the tabloids anyway.

While many finance executives in Silicon Valley try to blend in by driving Tesla electric cars and wearing jeans to work, the employees at the San Francisco office of Mr Smith’s Vista Equity Partners opt for sports cars and three-piece suits — a reflection of the tastes of their Texas-based boss.

And for the past couple of years, Vista has been making a splash through a series of eye-catching deals in the software industry — an area that private equity firms have long been wary of.

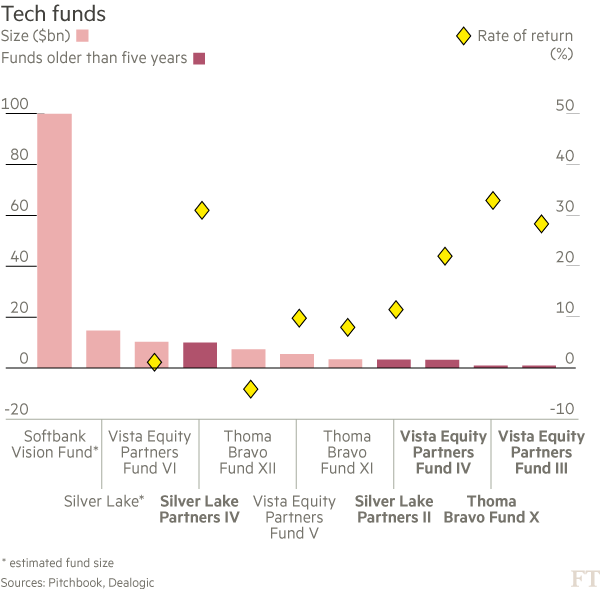

A former Goldman Sachs banker, Mr Smith set up Vista in 2000. Its record of buying, improving and selling software companies recently allowed it to raise $10.6bn for the biggest ever technology-focused private equity fund. The money is going out the door just as fast: in the past 12 months, Vista has bought four companies for more than $1bn each.

“We are very disciplined buyers,” says Mr Smith, who complains that he, a rare black man at the helm of a large financial institution, is often unfairly targeted by the police when he is at the wheel of his McLaren car. “We manage money for teachers and firemen and municipal workers. We have never lost money on any buyout investment. The last thing they want us to do is be irresponsible with capital and we take our fiduciary responsibilities very seriously.”

Glitzy consumer internet companies, such as Snap, Uber and Airbnb, have monopolised attention in the tech industry, stoking a debate over whether Silicon Valley is inflating a new bubble.

Along with groups such as San Francisco-based Thoma Bravo, Vista is at the forefront of a parallel trend of aggressive private equity investments that has the capacity to reshape the software industry. Many of the recent rapidly negotiated deals have been concluded with less due diligence than is typical, and have involved companies with higher growth but lower profits than those normally targeted by private equity firms.

The flurry of private equity investments raises important questions for the tech sector. On the one hand, it could indicate that this new brand of specialist firms has developed a secret sauce that allows it to generate reliable returns from software. Vista’s funds have typically made returns of more than 20 per cent, according to investment data provider PitchBook. However, the investments could simply be contributing to a new bubble that will inevitably lead to a lot of bad debt and failed companies.

Anthony Armstrong, head of technology mergers at Morgan Stanley who has helped sell a number of companies to the young private equity groups, believes they are blazing a new trail.

“It’s like the Golden State Warriors,” he says, comparing them to the highly successful Bay Area basketball team, which has revolutionised the sport with its mixture of pace and aggressive shot-taking. “Smaller players, moving quickly, making three-pointers.”

Vista is by no means alone. Indeed, it will soon relinquish its record as the largest tech-focused fund. Silver Lake, the Silicon Valley-based private equity firm responsible for the biggest ever tech deals such as the buyout of Dell in 2013 and Dell’s $67bn acquisition of EMC in 2015, is raising a $15bn fund. And the Japanese telecoms group SoftBank, primed with money from Saudi Arabia and Apple, is raising the Vision tech fund whose $100bn target size would trump anything that has come before.

A bid backed by Silver Lake is the frontrunner in an $18bn-plus auction for Toshiba’s flash memory business.

Thoma Bravo, which specialises in enterprise software, is also on a buying spree, paying $3bn for Qlik Technologies last year, a company that made just $13m in core earnings and recorded a net loss in the 12 months before the deal.“

There is a lot of capital in the category and more will come,” says Orlando Bravo, 46, the managing partner, who took the reins at the then Chicago-based firm and reoriented it geographically and philosophically to the west coast. Working from the Transamerica Pyramid, San Francisco’s tallest building, he last year raised a $7.6bn fund.

"When we were raising our fund, investors were asking, ‘Are there enough targets for all the money?’, and that’s when [SoftBank’s fund] was announced and my answer to that was, ‘There is way enough’,” Mr Bravo says. “We are, in hindsight, conservative because this is the first time that you have the large-scale tech software assets available to private equity.”

Mixed fortunes

When the private equity industry was in its infancy in the 1980s, the tech sector was barely on its radar. Gradually, this changed. First hardware assets became tolerable for debt providers.

Then came the realisation that software, although lacking hard assets to lend against, could offer reliable recurring revenues. “

The lenders originally were sceptical of the sector because the assets walk out the door every night and there was nothing that they felt they could lend against,” says an asset manager who invests in Thoma Bravo’s funds. “What has been proven is the stickiness of the sales in software. The renewal rates in the best businesses are well above 98 per cent.”

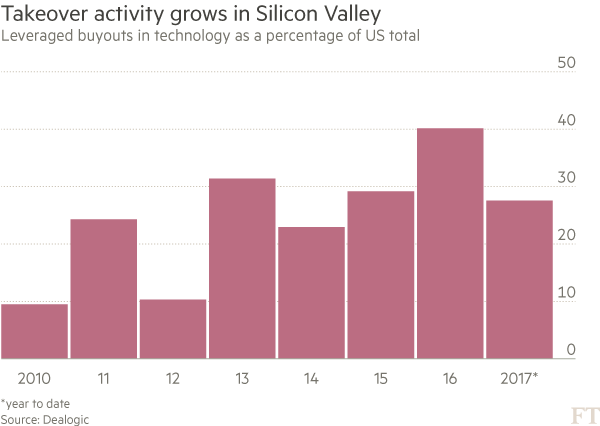

Tech is now attracting all types of private equity firms, with the sector representing almost 40.1 per cent of buyouts last year, according to Dealogic data. That is the highest proportion on record and up from around 10 per cent in 2010. Established generalists such as KKR and Carlyle have been joined by tech-focused firms such as Golden Gate Capital and the newer Siris Capital.

Dealmaking

$3bn Price paid last year for Qlik Technologies by Thoma Bravo — about 200 times its core earnings

$3.6bn Price Vista paid for Canada’s DH Corp to combine it with Misys after the latter’s IPO failed to be launched

The old guard has had a mixed record in the sector. In 2006, Freescale Semiconductor was taken private by a consortium of Blackstone, Carlyle, Permira and Texas Pacific Group for $17.6bn, just before its orders plummeted. Stephen Schwarzman, Blackstone chief executive, described it as a deal “where literally everything goes wrong”. More recently, Carlyle ended up cutting from $8bn to $7.4bn the price paid to Symantec for Veritas, a data storage provider, after banks struggled to finance the deal. Avaya, a networking company, bought for $8.3bn in 2007 by Silver Lake and TPG, filed for bankruptcy in January. In a sign of its changeable approach to the sector, Carlyle has opened, closed and reopened a Silicon Valley operation all within the past 10 years.

Perhaps their experience plays a part, but the larger firms are raising eyebrows at the prices and aggression of the younger pretenders such as Vista and Thoma Bravo. “They are prepared to pay an ebitda multiple that is almost ridiculous,” says a partner at a rival firm, referring to the standard valuation that considers the price paid as a multiple of earnings before interest, tax, depreciation and amortisation.

But Mr Smith is critical of some of the other funds for failing to understand the software market. “The world is awash with capital and ambition which has led more PE tourists to invest in the highly specialised area of software,” he says. “Many have already lost money in the space. I expect to see a few more lose money in their software investments in years to come.”

Ensuring returns

Vista believes that it can make money, even at these high multiples, by exerting an unusual amount of control on its acquired companies. It expects them to follow 100 best practices it has developed. It also requires an unusual amount of sharing between its portfolio. At monthly meetings, the top 300 managers across the companies gather to swap experiences. Everything is done to eke out revenue and margin gain.“

They can produce more code faster with fewer bugs, expand their markets more effectively and frankly enhance the customer experience,” says Mr Smith of companies that have submitted themselves to the programme.

Thoma Bravo does not impose as much control but Mr Bravo says there are always straightforward margin gains to be made because tech companies are reliably inefficient. “Silicon Valley thinks the same way they have since inception — singularly focused on top-line revenue growth,” he says.

This does not mean that the private equity model of slashing costs would work. Margins need to be improved but if that is achieved by cutting too many salespeople or too far into research spending, then growth will lag.

Vista can also be ruthless in the selection of managers. In some cases, it will decide to replace a newly acquired company’s executives. But Mr Smith will also go to extreme lengths to keep executives he values. Vista sold P2 Energy Solutions, which makes software for the oil industry, to its rival Advent International in 2013. Advent, understandably, assumed the management would be part of the deal. But after signing, Vista rehired the chief executive and chief financial officer and installed them at other companies.

Given the target companies often have little in the way of cash flows, the amount of debt used in the deals can seem worryingly large. Yet from another perspective, it can seem too small. Private equity firms like to use as little of their investors’ money as possible, typically borrowing three-quarters of a deal’s price. That allows them to capture more profit when they sell. But lenders will not write a blank cheque to buy companies with such meagre cash flows, forcing the funds to use more equity, which reduces risk but limits the potential returns.

Even Mr Bravo concedes the boom could still blow up — he just does not think his firm would suffer. “The thing I don’t like about the whole asset class is I haven’t seen other groups sell that much,” says Mr Bravo. “Where is the money on the table, guys? I’d like to see how much is stuck.” In the past few months, Thoma Bravo has sold three of its bigger bets, including Deltek, which it bought for $1bn in 2012 and sold on to Roper Technologies for $2.8bn.

Vista did get stuck on one recent deal, abandoning a planned initial public offering of Misys, the UK-based software company, after being unimpressed with what fund managers in London were prepared to pay. Mr Smith’s reaction was, true to form, aggressive. He pulled the listing and doubled down, buying Canada’s DH Corp, a financial technology group, for C$4.8bn ($3.6bn) last month, to combine it with Misys.

The market for selling such companies may evaporate altogether. The Nasdaq Composite surpassed its dotcom bubble peak in 2015 and valuations have kept rising. Another tech sector crash is not inconceivable. On the face of it, that might not seem to matter to the likes of Vista, which has never sold a company through an IPO. But with private equity firms commonly buying and selling the companies between each other, the music could stop at any time.

The McLarens of Silicon Valley would then really start to stand out.

Elliott: Activist investor lays path for tech deals

At 4:30am Lars Björk was disturbed by the ping of a text message. He was more disturbed when he saw the sender. Jesse Cohn of Elliott Management, the activist New York hedge fund, was writing to say he had bought shares in Mr Björk’s company.

For Elliott, which once impounded an Argentine ship during a dispute with the Buenos Aires government, the pre-dawn text sent in March last year counts as a token of affection. “I don’t take it personally,” says Mr Björk, a Swede who runs Qlik Technologies, a maker of data analytics software.

Technology used to be regarded as too complex for activist investors, but Mr Cohn was a trailblazer. He began taking on Silicon Valley companies in 2006 aged just 26, earning a reputation for a thorough understanding of the industry and a bracingly foul mouth. “He’s hard work but he’s not trying to be an asshole,” says one banker who advises the companies that Mr Cohn targets.

Less than three months after his rude awakening, Mr Björk and Qlik were in private equity hands. Thoma Bravo had agreed to pay $3bn. That was 73 per cent higher than Qlik’s value during a sudden dip in February, though only in line with where it was trading at the start of the year. It was a rich price for such an acquisition. A normal buyout might be done at 10 times a target’s core earnings. Qlik was done at 200 times.

Thoma Bravo has spent billions of dollars scooping up software companies. Three of the biggest — Qlik, Compuware at $2.4bn and Riverbed Technology for $3.6bn — were first smoked out by Elliott. Boards do not like to give in too easily to a potential bidder — and private equity firms tend to avoid hostile bids — but when an activist turns up, threatening to oust the board, deals can get done. Orlando Bravo (left), managing partner of Thoma Bravo, says that wooing companies will get easier: “Many are choosing to partner with private equity before the activists even show up.”

If public company boards do start waving the white flag without activists having to fire a shot, that might be bad news for Elliott. But the firm has a hedge: it has set up its own Silicon Valley private equity firm. And whether he is phoning to rattle a cage or launch a takeover bid, Mr Cohn has everyone’s number.

0 comments:

Publicar un comentario